There is a popular theory currently making the rounds in academic circles: that the once feasible notion that emerging markets can catch up with developed markets in economic growth is little more than a pipe dream. That theory is nonsense.

True, emerging markets face major cyclical headwinds. But their long-term potential to outgrow developed markets, and therefore close the GDP-per-capita gap — in other words, to achieve convergence — remains very much alive and well.

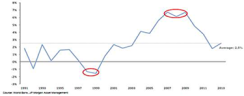

A comparison of emerging-markets GDP per capita relative to that of the U.S. since 1991 shows the inherent murkiness at pinpointing convergence. In real terms, growth in emerging-markets GDP per capita has outpaced the U.S. by an average of 2.5 percentage points over this period — but not without fairly massive speed bumps. Consider the late 1990s, when the U.S. economy was growing by leaps and bounds, while the Asian financial crisis was wreaking havoc across emerging markets. If you had taken a snapshot in, say, late 1998 and used that to extrapolate a long-term growth rate, you would have expected developed markets to have outgrown emerging markets by 1.4 percent per year in the foreseeable future.

Emerging markets vs. the U.S.: GDP per capita

We know the reality has been dramatically different. Emerging-markets GDP per capita expanded by a 6.5 percentage point faster annual rate compared with the U.S. from 2007 to 2009. As the U.S. economy was staggering through its biggest downturn since the Great Depression, emerging markets escaped relatively unscathed, supported by strong Chinese demand and the accompanying supercycle in commodities. Once again, had you chosen that moment to extrapolate the long-term trend based on the growth gap in this period, emerging-markets GDP per capita would have been expected to catch up with the U.S., in real terms, in just 32 years.

History is full of other examples of the nonlinear nature of economic convergence: such as the U.S. with the U.K. in the late 19th century, or South Korea with the U.S. in the second half of the 20th century. From a long-term perspective, both instances look fairly smooth. But a closer look reveals that the narrowing of the growth gap was much more volatile in both cases. History proves, and common sense dictates, that you simply cannot use a short period of GDP outperformance or underperformance to forecast a long-term trend.

Of course, the elephant in the room for the erroneous hypothesis that emerging markets will remain forever subjugated to their developed-markets counterparts is China. It would be misguided to attempt to formulate any credible theory without incorporating the Asian juggernaut. China accounts for more than 19 percent of the world’s population and has the second-largest economy. At the moment, the Chinese economy is suffering significant cyclical headwinds, and the recent period of below-trend growth in emerging markets could well continue.

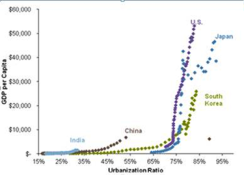

Investors should not forget the ability of major emerging markets to influence their own economic development and boost growth, however. Ways to achieve this include the rule of law, mobilizing and educating their workforces and investing in new infrastructure. China’s GDP per capita is still only 22 percent that of the U.S. and, despite the country’s rapid development, has an urbanization ratio of only 53 percent compared with the U.S.’s 83 percent. We therefore believe that China’s economic development, driven by a self-reinforcing cycle of urbanization and industrialization, still has much further to run.

Urbanization and GDP-per-capita growth

As a result, although it may be tempting to endorse this notion of dismissing the potential for emerging markets to ever close the gap with their developed-markets counterparts, the truth is that it’s just not that simple. The International Monetary Fund’s long-term GDP-per-capita growth projections show that emerging markets will outgrow developed markets by 2.4 percentage points in 2019 — a rate not far from the average of the past few decades. The outlook for emerging-markets convergence, it turns out, does not look quite so bleak after all.

Richard Titherington is chief investment officer and head of the emerging-markets equity team at J.P. Morgan Asset Management in London. For additional insights, please see Richard Titherington’s bio page.

Get more on emerging markets.