Emerging markets have been conspicuously absent from the global recovery that started roughly two years ago. Whereas U.S. growth forecasts have been ratcheting up steadily — and Europe and Japan looking marginally healthier than feared — emerging-markets growth forecasts have gone the other way, facing downgrades almost continually since 2011 (see chart 1). As one might expect, markets have responded. In the two years ending June 2014, the MSCI World index (developed markets) outperformed the MSCI EM index by roughly 43 percentage points in total-return terms. The S&P 500 outperformed EM by nearly 60 percentage points. Effectively, emerging markets have decoupled from developed markets in a significant — and, for EM investors, uncomfortable — way.

Recent data, however, suggests that this economic decoupling may be nearing an end. The market has begun to take notice, and the relative performance of emerging markets has improved noticeably in recent months.

What should we make of these developments? Allow us to suggest three takeaways:

1) The current decoupling is a cyclical phenomenon and the logical extension of orthodox policy measures adopted following the crisis.

2) A decoupling of emerging-markets growth from developed-markets growth is both rare and, more important, unsustainable.

3) There are early signs that a selective recoupling is under way, whereby manufacturing exporters are helping emerging markets rejoin the global recovery, supporting a return to emerging-markets equities.

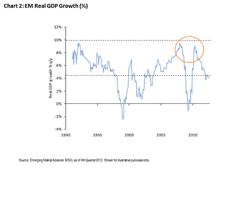

The cyclical pressures that emerging markets have faced during the past few years have their origins in the global financial crisis of 2008–’09. Heading into the crisis, emerging economies were booming, operating near full employment and not feeling the drag of excess leverage that plagued so much of the Group of Seven. As a result, the financial crisis that precipitated major recessions and protracted economic weakness in the G-7 created only a temporary pause in growth in emerging markets (see chart 2).

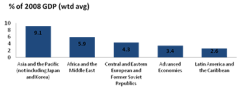

To prevent another Great Depression, policymakers worldwide embarked on record fiscal and monetary stimulus. Emerging countries did their part for the cause, despite their healthier position, and soon their economies returned to the significant growth they had enjoyed going into the crisis. It could be argued that EM countries did more than their part (see chart 3), with China, South Korea and Turkey providing more stimulus as a share of gross domestic product than the U.S. — the epicenter of the crisis — and the rest of the G-7.

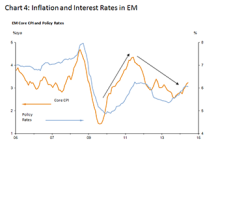

This outsize contribution to the global stimulus effort came at a cost: Given the health of the emerging economies going into the crisis, the aggressive stimulus measures soon led to overheating, and inflation pressures appeared on cue in 2010 (see chart 4). Emerging-markets central bankers and governments responded with orthodox policies intended to cool their economies and rein in inflation. These policies had their desired effect and set in motion the growth decoupling we have observed since early 2012.

In the World Trade Organization era of globalization, a decoupling of EM growth from a global recovery is both rare and unsustainable (see chart 5). In the past 20 years, such disconnects have only occurred on two other occasions. The first, in 1998, involved a major EM-centric crisis; the second was the commodity-led boom of the mid-to-late 2000s, when emerging markets’ growth continued to accelerate, despite the beginnings of the deleveraging-led slowdown in the G-7. In both cases, EM growth rejoined the global trend within two years — even in the case of a major crisis. Given that the current decoupling has persisted for more than a year, investors may be looking ahead to normalization, with EM joining the recovery firmly in place in developed markets.

We are seeing evidence to suggest that the economic and market decoupling that has plagued emerging markets since the peak in 2011 may be coming to an end. Though not yet showing consistent recovery, EM growth figures appear to have bottomed for this cycle, whereas developed markets may have seen their strongest gains. As evidence of this, we observe an upswing in the local purchasing managers’ indexes in EM relative to those in developed markets (see chart 6). Moreover, although we are encouraged by the improvement in the aggregate figures, the recovery is not yet broad-based. Manufacturing exporters are leading the charge, while commodity-linked exporters are still lagging, given the ongoing shift in China’s growth model away from commodity-intensive investment.

This upswing has corresponded to a turn in the relative performance of EM equities. Through mid-August, the MSCI EM index has outperformed the MSCI World (developed markets) by more than 400 basis points in U.S. dollars year to date, after having lagged by as much as 600 basis points as recently as March.

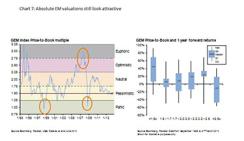

That rebound has not materially dented the valuation case for EM equities, given the evidence that EM economies appear to have stabilized and may be rejoining the present global recovery (see chart 7). At roughly 1.6 times book value, the MSCI emerging-markets index still trades at levels suggesting investor caution, a view confirmed by investor positioning. Should the data continue to support our view that a selective recoupling is already under way, we expect flows into EM equities to gain strength, lifting valuations to levels more in keeping with an improving outlook. Until we see a decisive and sustained turn in the economies and earnings in EM, however, we believe that being patient, waiting to add exposure when valuations pull back to 1.5 times book value or below, will be rewarded, as the case has been not only recently but also over the past 20 years.

George Iwanicki is an emerging-markets macro strategist, and Curtis Butler is a client portfolio manager, with the global emerging-markets team for J.P. Morgan Asset Management in New York. For additional global Market Insights, please see George Iwanicki’s bio.

Get more on emerging markets and equities.