Leveraged credit investments were strong in 2013, with bank loans returning 6.2 percent and high-yield bonds yielding 7.4 percent, according to the Credit Suisse leveraged loan index and the Bank of America Merrill Lynch U.S. high yield index, respectively. These yields occurred even as many other fixed-income asset classes were negatively affected by interest rate volatility.

The significant rise in Treasury yields from their lows in mid-2012 substantiated leveraged credit’s ability to deliver positive annualized returns in a rising rate environment. In fact, both loans and high-yield bonds have done so consistently for almost 20 years (see chart 1). High-yield bonds did have a correction in mid-2013, when spreads broke the typical negative correlation with Treasury yields, but recovered to provide positive returns in the fourth quarter as correlations reverted to normal patterns. Loans continue to deliver stable returns, with only a brief pause in June.

We have observed that the two components of the broader leveraged finance sector, bank loans and high-yield, share a close relationship, with the majority of companies that issue one also issuing the other. From a portfolio standpoint, however, investors may look to bank loans versus high-yield with nuanced objectives in mind. For example, investors with low tolerance for volatility and more interest rate sensitivity may emphasize loans, given the attractive relative value potential and downside hedging from their position in the capital structure. Investors with greater risk tolerance and a more benign outlook for rates may emphasize high-yield or, in the present environment, “medium yield,” as described in Pimco’s earlier viewpoint, “High Yield in 2014: Where Can You Look for Upside in a ‘Medium Yield’ Market?”

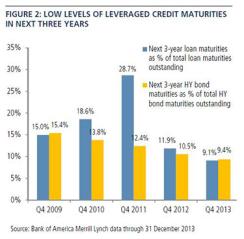

Consistent with our views, industry forecasts call for a low rate of defaults — in the 1 percent to 3 percent range — in leveraged finance markets, based on low levels of principal maturities in the next year, according to data from Bank of America Merrill Lynch. Issuance may ease back from record highs in 2013 but should remain healthy. We also expect continued slow but steady growth in the U.S. economy to offer further stability to these companies.

Less than 10 percent of the combined high-yield and loan market is maturing between 2014 and 2016. This figure represents a five-year low for the three-year principal maturity schedules (see chart 2) and lends support to our outlook for low defaults through 2014 and into 2015. We expect there will be a few notable exceptions, including some leveraged buyouts from 2006 that will likely default in 2014. These are largely anticipated and priced into the market, however. In general, we expect calm credit conditions for leveraged finance in 2014.

Given these strong underlying credit fundamentals, look for the technical side to be the primary driver of shifts in the loan and high-yield bond markets in 2014. In 2013 high demand not only supported refinancing and maturity extensions but also prompted the return of more issuer-friendly structures, with covenant lite becoming the norm in the loan market, payment-in-kind toggles returning to the high-yield market and more instances of loans and bonds funding dividends or share repurchases. In 2014 we expect these issuer-friendly features to continue, unless there is an unexpected drop in demand for high-yield credit. That said, our fundamental outlook is for continued strength in demand.

After record retail flows of $62.4 billion into loan mutual funds, according to figures from J.P. Morgan, and robust collateralized loan obligation issuance in 2013, we expect the pace of flows into the loan market to slow in 2014 but remain positive. On the CLO front, many managers are trying to print deals ahead of new federal risk-retention rules that are in the works, particularly smaller managers who may be less able to meet the new requirements. Steady retail demand and increasing institutional appetite for loans should drive demand into 2014.

High-yield lost $3.9 billion in outflows in 2013. High-yield exchange-traded funds rose $900 million, whereas actively managed funds lost $4.8 billion through December 25, according to data from EPFR Global. In 2014 overall demand for high-yield is expected to be influenced by rate volatility as credit fundamentals remain supportive.

Responding to investor interest, leveraged credit issuance accelerated in 2013 to a combined $1.07 trillion in loans and high-yield, with record-high levels in both markets.

Corporations have been focusing on strengthening their balance sheets, as evidenced by data from J.P. Morgan that shows 75 percent of new loan issuance and 54 percent of high-yield issuance related to refinancing or repricing of existing debt.

We expect to see a reduction in overall issuance in 2014, but activity should remain healthy. Industry forecasts range from approximately $285 billion to $335 billion in high-yield bonds and from $350 billion to $420 billion in loans, based on sell-side research from Morgan Stanley, Barclays, Credit Suisse and J.P. Morgan. After addressing near-term maturities, we believe issuers will set their sights on maturities from 2017 to 2019, pushing maturities farther out as long as the markets remain receptive.

Bellwether deals for H.J. Heinz Co. and Dell gave rise to expectations of more M&A activity in 2013, but that never materialized. With the economy improving, we could begin to see corporate issuers more willing to spend their cash in 2014. We may see more organic new issuance to finance mergers or capital-spending programs, also known as capital expenditure programs, which have been lagging as companies focused more on extending their debt maturities (see chart 3). We thus expect investment-grade issuers to continue to offer a higher share of new supply in the market. In 2013 through November, $128.5 billion in new high-yield supply came from “fallen angels,” companies whose ratings have been downgraded from investment grade to high yield, representing a higher proportion of new issuance than in previous years, according to Bank of America Merrill Lynch.

While we could see more organic new issuance, we also expect transactions to fund dividends to continue, as the exit strategy for many private equity-funded deals remains unclear. This year we are moving farther into what has become a prolonged credit cycle. The fundamentals are in place to create a low-default environment that is “supportive of stability in the speculative-grade credit markets,” as a recent Moody’s report phrased it. We at Pimco continue to see erosion in structural protections, however, and are closely monitoring an overall increase in leverage as more aggressive transactions test the depth of the market. With careful attention to individual credit and market liquidity risks, we believe leveraged credit offers many opportunities for attractive returns in 2014.

Andrew Jessop is a high-yield portfolio manager and Elizabeth MacLean is a bank portfolio manager at Pacific Investment Management Co.’s headquarters in Newport Beach, California.

See Pimco’s disclaimer.

Get more on fixed income.