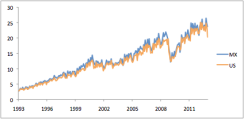

Against a generally soft backdrop for emerging-markets currencies, the Mexican peso stands out thus far in 2013. Overall indexes suggest that emerging-markets currencies have moved sideways or, at best, edged slightly higher since the end of last year. The peso, by contrast, has strengthened more than 5 percent against the U.S. dollar. The currency is again approaching the $12 mark, which it broke through for a time in early 2011, before that year’s mid-year risk asset selloff (see Chart 1).

This appreciation has not reflected near-term growth enthusiasm. Although the Mexican economy has been growing at a satisfactory pace, it is not booming. Real gross domestic product expanded at a seasonally adjusted rate of 3.1 percent quarter on quarter in the fourth quarter of 2012 and does not seem to have picked up in early 2013 despite the upside growth surprise in the U.S. Indeed, Mexican industrial production growth has turned negative in the past few months, in contrast with the acceleration across the border. Nor is the strength of the peso due to improved carry (the overnight interest rate that accrues to investors long a particular currency), as Banco de Mexico actually cut the overnight interest rate 50 basis points on March 8 — an event that appears to have helped touch off the most recent part of the peso’s rally.

Chart 1: Mexican peso vs. U.S. dollar

Chart 1

Source: Bloomberg; data through April 15, 2013 |

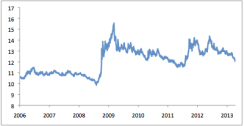

Chart 2: Mexico real effective exchange rate (2010 = 100)

Chart 2

Source: BIS, JPMAM; data through February 2013 with estimate for March 2013 |

Can the peso strengthen further? Its move this year takes it, in real effective terms, to within shouting distance of the average rate observed in the period from 2003 to 2008. In turn, that plateau followed a slide at the start of the 2000s that coincided with China’s entry into the World Trade Organization, a competitiveness blow to Mexico, which persistently lost market share in the U.S. for years afterward. Given considerable restructuring within Mexico (along with an extended period of wage restraint), as well as the steady rise of wages within China and other Asian economies, the economy can probably sustain a stronger real exchange rate today than was the case five to ten years ago. That view, however, probably requires validation in the form of stronger trend growth, which might result from the current reform wave. Any such improvement will likely become apparent only over the course of a few years. In the short term, then, room for additional appreciation seems somewhat limited, as the currency has broadly returned to its precrisis level. Significant gains look more like a long-run phenomenon.

On an entirely separate topic, doubts about the reported strength of Chinese exports in recent months have focused on the mismatch between shipments to Hong Kong, as reported by the Chinese authorities, and imports from China as shown in the Hong Kong version of the data. Given the somewhat sluggish international backdrop as well as the historical pattern, in which the data have generally lined up nicely, valid ground for concern may exist. The Mexican experience, however, shows that bilateral trade figures need not match entirely. Chart 3 shows Mexican exports to the U.S. from the perspective of the official Mexican and U.S. data, while Chart 4 shows Mexican imports from the U.S. on these two bases. In theory, the numbers should match nicely, as they are measuring the exact same thing, just on two sides of a shared physical border (with no timing issues associated with, for example, long shipping routes).

Moreover, the two statistical agencies — Mexico’s INEGI and the U.S. Census Bureau — cooperate closely in producing the numbers and attempting to iron out differences, and no obvious reason exists for the numbers to vary. Indeed, most of the time, the figures match. But there are extended periods during which the two series will diverge, painting a stronger or weaker picture depending on which set of numbers is “correct.” As an illustration, since mid-2010, Mexico has persistently shown weaker imports from the U.S. than the Census Bureau has reported for U.S. exports to that country. The bottom line is that contrasts in bilateral trade data do not suffice, in themselves, to assume data manipulation.

Chart 3: Mexico exports to the U.S. in Mexican and U.S. data (USD bn, sa)

Chart 2

Source: JPMSI; data through January 2013 |

Chart 4: Mexico imports from the U.S. in Mexican and U.S. data (USD bn, sa)

Chart 4

Source: JPMSI; data through January 2013 |