Global creditworthiness looks a lot like the global economy these days: modestly weaker overall but with some pockets of strength.

The average rating of 179 countries declines by 0.6 point, to 43.9 on a scale of zero to 100, according to Institutional Investor’s semiannual Country Credit survey. The retreat reflects widespread drops in most regions of the world, only partly offset by modest gains in Western Europe. The latest decrease reverses an upturn registered six months ago and leaves the global average sitting well below the all-time high of 48.0, which was recorded in September 2008.

The findings echo January’s revised forecast from the International Monetary Fund, which sees the global recovery remaining intact but proceeding at a slower, subpar rate of 3.5 percent this year.

The countries that manage to eke out rating increases are generally regarded as doing better than previously thought but not doing particularly well. Exhibit A is Western Europe, where ratings rise for 16 of the region’s 19 countries, with the biggest gains coming in peripheral countries such as Greece (up 2.6 points), Portugal (2.2) and Ireland (1.6).

The situation “appears more favorable today than it was a year ago,” says Joseph Doumar, a risk analyst at New York Life Investment Management. “I think we’ve seen some real improvement, documented improvement, in sovereign credit quality.” But, he adds, European leaders still haven’t fixed the euro’s structural weaknesses, and each passing day is as likely to bring bad news as good.

Elsewhere, the U.S. leads a broad-based decline in creditworthiness. The country’s rating falls 1.1 points, to 88.8, its lowest level in the 33-year history of the survey. The U.S.’s ranking drops two notches, from tenth to 12th. It now sits below Australia and the Netherlands and just above Austria and Hong Kong.

Analysts attribute the drop to continuing worries about political gridlock in Washington. Congress and the Obama administration may have managed to avoid the so-called fiscal cliff at the turn of the year, but there is still plenty of opportunity for clashes over sequestration — a package of budget cuts scheduled to take effect in March — and the debt ceiling, which needs to be increased in May.

The U.S. rating decline “is due to political instability and political problems,” says Dae Kyun Mok, a senior portfolio manager at Mirae Asset Global Investments Co. in Seoul, South Korea. “It’s not due to economic problems. The macro indicators have shown improvement in the past two or three years.” John Sharma, an economist at National Australia Bank, agrees. “There are a number of positive indicators for the U.S. economy, so even though it contracted in the last quarter of 2012, there are still a lot of positive signs.”

Survey respondents also see positive signs in China, which posts a 1.1-point rise. The gain reflects a growing confidence that the country has achieved an economic soft landing. “People are beginning to cope with China growing at 7.5 or 8 percent, as opposed to double digits,” says Christian DiClementi, an economic analyst at AllianceBernstein in New York. “They’re saying, ‘I’m okay with 8 percent.’ ” And if China is okay, that’s good enough to pull up Hong Kong, which sees its rating jump 2.4 points.

Japan also posts a significant gain, rising 2.2 points; its ranking moves up two places, to 18th. The reflationary policies that Shinzo Abe has adopted since taking over as prime minister in late December elicit optimism among some analysts. Abe has ramped up government spending, pressured the Bank of Japan to adopt quantitative easing and encouraged a depreciation of the yen to end Japan’s prolonged deflation and jump-start growth. Abe’s determination to stimulate growth “has contributed a lot of positive sentiment,” says Marc Bautista, head of research at Metropolitan Bank and Trust in Manila.

In contrast to the scattered gains in advanced nations, much of the developing world suffers a ratings decline. Developing Asian nations fall by 0.5 point, on average; Eastern Europe and Central Asia sheds 1.2 points; Latin America and the Caribbean drop by 1.9 points; the Middle East and North Africa declines by 0.8 point; and African states slip by 0.3 point, on average. The lack of a strong economic locomotive in either the U.S. or China has clearly taken a toll on much of the world, analysts say.

Although the Chinese economic slowdown is turning out to be modest, most Asian developing nations see slight ratings declines because they’ve suffered a cut in their China growth dividend. The most notable exception to the trend is Myanmar, which gains 3.1 points because of optimism that the country is now lifting its self-imposed isolation from the global economy.

In Latin America, 23 out of 29 countries decline, while only six win ratings increases. Two of those gainers — Cuba (up 2.3 points) and Venezuela (1.5) — benefit from anticipation that their longtime leaders, Fidel Castro and Hugo Chávez, respectively, are nearing the end of their power. As for the rest of the region, there’s a heightened sense that nothing can substitute for a strong U.S. economic impulse. “Europe is struggling,” notes National Australia Bank’s Sharma, and slower growth in China is being felt in Latin America.

Africa presents a bit of a mixed picture. Despite the modest average decline, 18 of 49 states in the region see their ratings rise. “We think Africa is one of the bright spots of the world going forward,” says AllianceBernstein’s DiClementi. “When you comb the surface of the earth, you say, ‘Where else are you going to see growth?’ ”

Countries in Eastern Europe and Central Asia are facing a double whammy, says Ulrich Rathfelder, a country-risk analyst at Landesbank Hessen-Thüringen in Frankfurt. Stagnation in the euro area means that Eastern European countries are exporting less to their prime customers in Western Europe, he says. At the same time, he adds, “financing for Eastern Europe is more difficult” because troubled Western European banks are retreating to their home markets.

Ukraine’s rating falls by 10.1 points, the biggest decline in the survey. The drop reflects concerns about the country’s economy, its testy relationship with the IMF and its increasingly repressive political system, Sharma says. Slovenia falls 5.2 points, the second-biggest decline in the region. “It’s got problems with growth and their banking system,” Sharma says. “And they’ve been downgraded.” In August, Fitch Ratings, Moody’s Investors Service and Standard & Poor’s all downgraded Slovenia by one notch, citing concerns about a rising debt burden and the cost of recapitalizing its banks. S&P made another one-notch downgrade in February.

In the Middle East and North Africa, domestic political unrest pushed down a number of countries, including Algeria, which falls 2.4 points; Tunisia, down 2.9 points; and Syria, which falls 3.0 points. It also limited gains among Gulf oil producers. “Those who give good marks to the Gulf countries may be neglecting the political risks,” says Rathfelder.

Overall, the picture that emerges from the survey is one of resignation. A slowly growing, politically divided U.S. is providing only minimal horsepower for global reflation; Western Europe remains deeply troubled; and China is growing fast, but not fast enough to do much for the rest of the world.

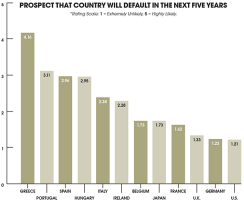

Despite Western Europe’s higher ratings this time, its future clearly remains the global financial system’s principal concern. Six of the seven nations voted most likely to see their ratings decline in six months’ time are in Europe: Cyprus, France, Greece, Italy, Portugal and Spain. Argentina is the only non-European country to make that list. By contrast, the six nations voted most likely to rise are all over the planet: Brazil, Indonesia, Ireland, Paraguay, Peru and the Philippines. The percentage of respondents who said they regarded a default as likely or very likely in the next two years fell to 23.6 percent for Spain and 18.9 percent for Portugal, down from 27.8 percent and 33.3 percent, respectively, six months ago. Greece still stands in a class of its own: Fully 74.5 percent of respondents saw the country as likely or very likely to default within two years, up from 65.2 percent previously.

In the near term analysts say the world appears to have settled into a new normal in which Europe limps along at the edge of the precipice, while most other regions tread water. “A lot will depend on the U.S.,” says National Australia Bank’s Sharma. “If things go smoothly, I will be cautiously optimistic.” And if not, the world will struggle to find a new locomotive to pull it out of its torpor. • •