The outperformance of emerging-markets equities has represented one of our main investment views since late last year and one we have expected to see playing out strongly through the course of 2013.

This projection has rested primarily on our forecast of a cyclical upswing in emerging-markets economic growth following several quarters of below-trend expansion, along with the corresponding underperformance of emerging-markets equities versus the S&P 500 since mid-2011.

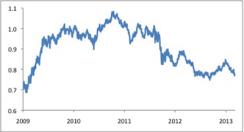

In response to significant improvement in the data flow from China, along with similar improvement elsewhere in emerging Asia, emerging-markets equities began outperforming strongly in September 2012, a trend that continued through the end of the year. Since then, though, emerging-markets equities have stumbled badly in relative terms. While the S&P 500 has gained more than 8 percent, year to date, emerging-markets equities have become stuck in neutral, posting only a very marginal increase during 2013. Emerging-markets equities have thus unwound most of their late-2012 outperformance against U.S. stocks (Chart 1).

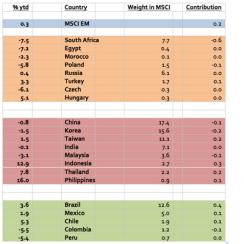

Sometimes, exceptionally strong or weak performance by an overall emerging-markets index reflects big swings in a small number of constituents, as has been the case this year to some extent in emerging-markets debt, where high-yielding Argentina has hurt the emerging-markets bond index significantly. For equities, though, just about everything has gone wrong recently. Chart 2 shows year-to-date performance (in dollar terms) by each of the constituents of MSCI’s emerging-markets index, along with its weight in the index and its contribution to overall performance. Among the 21 members, only two — Indonesia and the Philippines — have risen more than the S&P 500 this year, with their Asean neighbor Thailand not far behind. Meanwhile, more than half of the countries represented in the index have seen their equity markets fall this year.

Chart 1: MSCI EM vs. S&P500

(price terms), 1 Jan 2010 = 100

Chart 1

Source: Bloomberg; data through March 8, 2013 |

• The yen. Despite the convincing, if somewhat uneven, growth rebound in emerging-markets Asia, the three highly cyclical economies represented in the index — Korea, Taiwan, and Malaysia — have posted a negative aggregate equity performance this year. This weakness likely reflects the large yen depreciation. That produces a one-time competitiveness shock for these economies, which export broadly similar products as Japan (and which also sell heavily into the Japanese market). Damage from the yen’s slide likely falls disproportionately on companies represented in the equity indexes, especially in Korea’s case.

• The incomplete cyclical rebound. While Asia has turned upward, the inflection point in economic activity has not yet occurred definitively elsewhere. Weakness in the euro area continues to weigh on emerging-markets Europe. Meanwhile Brazil — another economy with strong links to the global cycle — remains sluggish. Five of the eight EMEA (European, Middle East and Africa) markets in the index have suffered year-to-date losses, including two of the three with the closest euro area links (Poland and the Czech Republic, with Hungary having recorded a moderate gain). Brazil has also lagged the S&P 500 significantly.

• Fears of policy tightening. Weakness in emerging-markets growth during late 2011 and 2012 primarily reflected earlier policy tightening, which itself came in response to overheating concerns. The sluggish growth pace of recent quarters has alleviated that pressure but does not appear to have created significant across-the-board slack. Emerging-markets economies, then, have less room to run than their developed-markets counterparts, where unemployment rates remain high. The growth upturn thus has already stirred fears of an eventual monetary policy response. The Chinese market, in particular, has suffered from this concern, with the authorities ratcheting up housing market restrictions in the past few weeks and investors beginning to think about possible credit tightening or even interest rate increases. In Brazil, too, the central bank has sent a strong signal that a tightening cycle is on the way, even before the economy’s vigor improves noticeably. Just as easy money continues to support developed-market equities, emerging-markets equities may already be suffering this year from policy changes in the other direction.

• Stagnant commodity prices. Overall commodity prices have done nothing thus far in 2013, and major indexes like the CRB remain well below their 2011 peaks. Lack of support for commodity prices probably reflects a combination of global slack, a reduction in the commodity intensity of Asian (especially Chinese) growth, and some loosening of supply constraints (especially in energy). Commodity-sensitive markets have generally struggled this year, including Russia, Colombia and Peru.

• Country-specific concerns. Just as growth tends to soothe many ills, weakness or sluggishness can expose many problems. Ongoing difficulties in South Africa and Egypt (especially the latter) may not owe to cyclical considerations, but the market has a tougher time shrugging off such developments in a weak-growth atmosphere. Mining disturbances in South Africa and political turmoil in Egypt have left these two markets as the weakest among the MSCI constituents in 2013. South Africa’s weight — nearly 8 percent of the index means it alone has accounted for -0.6 percentage points of overall performance on the MSCI’s emerging-markets index this year.

Chart 2: MSCI EM performance by country

Chart 1

|

While emerging-markets equities can still rise more strongly than the S&P 500 with these forces at work, emerging-markets outperformance this year may fall short of what the business-cycle swing would typically generate.

Michael Hood is a market strategist for J.P. Morgan Asset Management.