A guy walks into a bar. There, at the table next to the fireplace, he sees a lovely young woman reading. He’s overwhelmed with her beauty, and, almost without realizing it he’s walking up to her. And after a few pleasantries and compliments, he’s doing well. She’s laughing. But he knows he only has a few moments to deliver a single question that can kick-start a conversation that will keep her engaged and talking throughout the evening. So he turns to her and he says, “So... tell me the truth... what do you think the correct discount rate assumption is for public pension fund liabilities?” There’s silence. She sighs, looks at her watch and flags the bartender. Our hero is crestfallen, assuming the waiter is being summoned to deliver the bill. “Can I help you?” “Yeah”, she says, “I’m going need a double... and get one for my friend here too. We’ll be here for a while. Actually, you know what, just bring the bottle.” Yadda yadda yadda.

Okay, okay, I admit that pension fund discount rates should almost certainly never be part of any pickup line that’s being delivered seriously. Notwithstanding, the discount rate of public pension funds is one of the most pressing topics of our generation... and so I do think it should be a more frequent topic of conversation... even among friends at bars and cocktail parties. Why? The discount rate assumption will ultimately determine how much the sponsoring governments will have to contribute to their funds today in order to ensure they are solvent tomorrow. And that means that the choice of discount rate will directly affect government budgets and, thus, it will affect all of us.

For example, my old colleagues at Boston College suggested that a drop in the discount rate for public pension funds was warranted. And, in addition, they argued that the appropriate discount rate would increase the size of the unfunded liability from $0.7 trillion to $2.2 trillion. In other words, in order to meet its “real liability”, sponsors would have to come up with an extra $1.5 trillion... that they don’t have. So this is a very big deal with huge implications for present day government spending and taxation. And the reason I bring this up today is because my II colleague Frances Denmark has quite a nice piece entitled, “Debate Heats Up over Public Pension Fund Discount Rates”. Go read it.

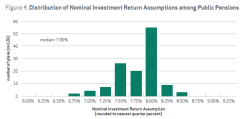

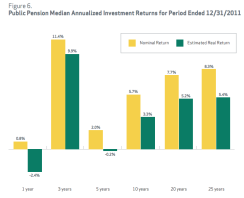

Anyway, I actually have to head out, so I can’t dig too deep into this topic just now. (‘How very convenient’, you must be thinking.) But before I dash off, I will leave you with some nice charts out of a recent report by the National Institute of Retirement Security, as I think they may help frame the debate for you. The first chart shows the nominal expected returns used by public pension funds as their discount rate for liabilities – I think all would agree that these seem fairly aggressive. The second chart then shows how these same pension funds have performed over varying time scales. As this shows, the 25-year return for these investors remains above the expected returns.

And this is precisely why there’s so much tension surrounding this debate. On the one hand, there’s plenty of truth in the argument that these pension funds are being unrealistic. But, on the other hand, there’s also plenty of rationale for not raising taxes today to pay for pensions if, over the long run, these funds are actually going to meet these return assumptions (as they have for the past 25 years). It’s enough to turn your hair grey...