As the global recession and financial crisis recede in the rearview mirror, companies have been acting more proactively in using their balance sheets in ways that enhance shareholder value. But we think they can do a lot more.

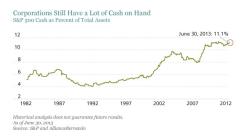

As the market tumbled and liquidity dried up after 2008, companies became very conservative, hunkering down and building massive cash reserves on their balance sheets. By mid-2013, U.S. companies were sitting on cash that was equivalent to about 11 percent of their total assets (see chart below), a three-decade high and earning almost nothing. What’s more, a long decline in interest rates made borrowing much cheaper.

When corporations don’t put their healthy balance sheets to work in productive ways, shareholders get restless.

Thankfully, that trend has changed. With borrowing costs still very low and business conditions stable to improved, management teams have become more receptive to using debt to buy back shares, increase dividends and make acquisitions.

Each of these actions can boost shareholder value. Share buybacks shrink the total number of shares outstanding and give a shot in the arm to earnings per share by helping them grow more rapidly in the years ahead, all things being equal. Dividend payments provide attractive income to investors, and acquisitions — if executed thoughtfully — can create new avenues for business growth.

It is getting more difficult to find companies that appear content to ignore low interest rates and high cash balances. But we still see some companies doing exactly that, even good businesses that represent attractive investments. They can do better for their shareholders.

Take Qualcomm. The telecommunications giant is a well-run business, but management’s strategy for returning capital to shareholders has been underwhelming. The firm sits quietly in San Diego and has a net cash balance equivalent to about $18 per share, with $6 per share of that held domestically — making it more accessible. Without borrowing a cent or repatriating any offshore cash, Qualcomm could buy back 9 percent of its shares outstanding. By issuing relatively cheap debt, it could have more cash on hand and accomplish the same goal.

We believe that buying back shares would benefit both the stock price and shareholder value. The company reported $1.5 billion in share repurchases for the second quarter. But since these purchases were used to offset the exercise of company stock options, the average number of shares outstanding actually rose compared with the same quarter in 2012 and, for that matter, the first quarter of 2013.

So, from the perspective of outside shareholders, no shares were repurchased. Even as Qualcomm’s corporate earnings exploded in recent years, its stock price languished. In fact, it’s trading at a discount to the S&P 500 measured by price-to-earnings — despite strong growth forecasts.

Apple took a different route, but only after a lot of convincing. It was a longtime holdout from buybacks, offering similar justifications to those we’ve heard from Qualcomm and other companies. These include the need for sufficient cash reserves to make operational investments and acquisitions in a rapidly evolving industry. We acknowledge the need for some liquidity, but it’s telling to us that Apple eventually relented and borrowed against its cash reserves to buy back a substantial number of shares.

Other companies still resist share repurchases, even when their stocks are undervalued and they have more than enough cash to shrink bloated share bases. Qualcomm’s management has raised its dividend in recent years, a modestly positive step. But it hasn’t reduced the share base — and that certainly doesn’t help the company take advantage of its stock’s low P/E ratio.

In our view, truly shrinking a share base by buying back shares is likely to lead to higher earnings per share. And since corporate cash is earning less than the dividend yield on the stock, repurchasing shares could actually save money. Whether a company uses cash, relatively cheap debt issuance or a combination of both to increase shareholder value, we think investors would welcome the news.

Kurt Feuerman is chief investment officer of Select U.S. Equity Portfolios at AllianceBernstein.

Read more about equities.