Tech giant Apple has been swatted by the U.S. government lately over e-book price-fixing, while the company has watched its dominance in mobile phones and tablet computing erode as more competitors enter those markets. But for exchange-traded funds that track growth stocks, none of this matters, according to data prepared for Institutional Investor by New York–based financial data firm Axioma. Of the 11 growth ETFs examined by Axioma, eight had Apple as their largest holding.

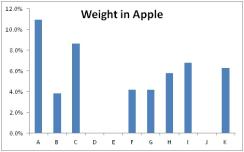

The iShares Morningstar Large Growth Index Fund (fund A in the chart below), had the largest holding, with 10.94 percent of its assets in the iPhone maker. The Vanguard Mega Cap 300 Growth Index Fund has the second-largest holding, with 8.65 percent. The Vanguard Growth Index Fund, the SPDR S&P 500 Growth ETF and the Schwab U.S. Large-Cap Growth ETF have 6.77 percent, 6.27 percent and 5.77 percent, respectively (see chart 1 below).

To Melissa Brown, senior director of applied research at Axioma, the heavy concentration in Apple shares among some growth ETFs is cause for concern. “Apple is a very big stock in the market, so maybe it’s not that surprising, but it really is betting big on Apple,” she says. “If you’re buying that iShares Morningstar Large Growth Index Fund, for example, that’s probably something you should know.”

Chart 1

Chart 1

A iShares Morningstar Large Growth Index Fund; B iShares Russell 3000 Growth; C Vanguard Mega Cap 300 Growth Index Fund; D First Trust Large Cap Growth Alphadex Fund; E Guggenheim S&P 500 Pure Growth ETF; F Vanguard Russell 1000 Growth; G iShares Russell 1000 Growth; H Schwab U.S. Large-cap Growth ETF; I Vanguard Growth Index Fund; J Powershares Dynamic Largecap Growth Portfolio; K SPDR S&P 500 Growth ETF |

Chart 2

Chart 2

|

Growth ETFs largely fall into one of two broad strategies, according to Brown. “Basically, you’ve got two different definitions of growth,” she explains. “One is more stable growth, which would be steady and not extremely volatile. Then there’s the cyclical growth, where growth may be higher now but probably contains more volatility.”

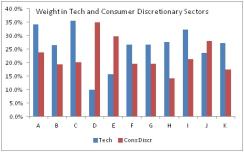

On the more volatile end of the spectrum, Brown points to iShares Morningstar Large Growth Fund. Although its name wouldn’t suggest any particular view on growth, the fund is “very tech heavy and very concentrated,” Brown says. Apple makes up 11 percent of its portfolio; tech is 35 percent of assets; and the fund is very concentrated, with 80 percent of the portfolio in the biggest 50 stocks.

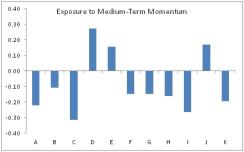

The Guggenheim S&P 500 Pure Growth ETF falls on the other end of the spectrum, says Brown. The fund doesn’t hold Apple shares at all, and it’s much more heavily weighted in consumer discretionary stocks than technology companies. The Guggenheim ETF has a much higher exposure to momentum than most of the growth ETFs Axioma studied, “meaning that the stocks in its portfolio are ones that in general have done well recently, which is not true for all of these portfolios,” adds Brown.

Indeed, the growth ETFs’ exposure to momentum — that is, swings in performance by various stocks — is another area in which there is some diversity (see chart 3 below). “The common wisdom about growth managers is that they tend to be more momentum based, [but] what we’re seeing here is that this is not the case,” says Brown. “It’s true for some of the funds, but not true for all of them. Some of them seem to have a reasonably high exposure to low-momentum stocks, which is really kind of interesting. You tend to see that more in a value-oriented portfolio.”

Chart 3

Chart 3

|