What counts as a slowdown in China would make most other nations envious. After dominating equity listings from 2009 to 2011, the country slipped to No. 2 behind the U.S. last year as its stock markets struggled and regulators put the brakes on approvals. But thanks to policy reforms and growing economic bullishness, domestic and offshore fundraising could send Chinese initial public offerings skyward again.

The IPO pipeline contains a record 800-plus Chinese companies, says Hong Hao, head of research at Bank of Communications International in Hong Kong. In late 2011, by comparison, that number was less than 300. “Yes, 2013 will be a better year for sure,” Hong predicts. Hu Yifan, Hong Kong–based chief economist at Haitong International Securities Group, agrees. “I see a pickup in the economy, a pickup in investor sentiment and a large increase in liquidity,” Hu says. “There will be a pickup in both volume and values in 2013.”

Still, there’s a disconnection between China’s economic fundamentals and its capital markets, explains Jing Ulrich, Hong Kong–based chairwoman of global markets at JPMorgan Chase & Co. The biggest problem is Beijing’s stubborn preference for listings by state-controlled companies, which enjoy not only monopolies but preferential access to bank financing. “China’s equity markets have long been treated as a funding channel for state-owned enterprises, with excessive IPOs, lack of transparency and a poor track record of dividend payments favoring equity issuers instead of secondary market investors,” Ulrich says. “Many Chinese retail investors lack confidence in the market and have never made a profit in their limited stock investing experience.”

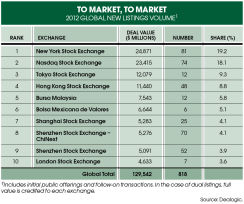

By any standard, China saw plenty of IPO activity last year. Its three stock exchanges had 195 listings that raised a total of $27.1 billion, according to Dealogic; the U.S. had 155 offerings on the New York Stock Exchange and the Nasdaq Stock Market for a combined $48.3 billion. But for China the latest figures represent a dramatic fall from 2011, when it had 341 listings that raised $69 billion.

As the global economy flagged in 2012, Chinese regulators clamped down on IPOs at the Hong Kong, Shanghai and Shenzhen exchanges to avoid flooding the market with stock. They were especially cautious about the Shanghai Stock Exchange, whose A shares are mostly off-limits to foreign investors, but they also held back on approving listings on the Hong Kong Stock Exchange, China’s primary offshore marketplace.

Authorities feared that a surfeit of IPOs would further weigh on the benchmark Shanghai Stock Exchange Composite Index, which gained just 3.2 percent in 2012, its first annual advance in three years. State-owned enterprises account for more than 80 percent of the Shanghai exchange’s 932 names, and Beijing is sitting on 2 trillion yuan ($321.5 billion) worth of stock in such companies. During bear markets Chinese investors tend to avoid SOEs because most of them offer relatively low dividends; Hong Kong–listed H shares pay more in a bid to attract global institutional investors. About 50 Chinese companies — the majority of them large SOEs — have dual A- and H-share listings on the Shanghai and Hong Kong exchanges, respectively.

Reforms may help improve the IPO picture. For one thing, it’s now easier for smaller companies to sell stock abroad. On January 1, the China Securities Regulatory Commission began allowing Chinese corporations to list on international exchanges if they meet those markets’ standards. Previously, besides raising $50 million through an IPO, applicants needed annual net income of 60 million yuan and net assets of 400 million yuan. Over the past year the CSRC has pushed all publicly traded companies to hike their dividends. To boost the quality of businesses, it’s tightening audit measures for IPO hopefuls. And regulators keep increasing the proportion of private enterprises on the Shanghai exchange; just five years ago it was nonexistent.

Meanwhile, the Chinese economy appears to be regaining momentum, says JPMorgan’s Ulrich. Between the second and third quarters of 2012, the annualized rate of growth rose to about 9 percent. After hitting an almost four-year low in early December, the Shanghai Composite had rebounded by 16 percent as of January 11 amid optimism about new Communist Party general secretary Xi Jinping, who has signaled that his market reforms will include more private sector lending.

“As policy reforms take shape, market conditions should become more favorable for the average investor,” Ulrich says.