Brazil’s worsening fiscal accounts have attracted attention all year, and that has intensified in the past few weeks since the release of very poor September figures. Concern about public finances has helped fuel a sell-off in Brazilian credit relative to other BBB-rated Latin American borrowers such as Colombia and Peru. Analyst rhetoric about the situation has thus turned sharply negative. To some extent, this worry appears justified. Brazil’s fiscal accounts have genuinely worsened in the past two years, and the government will need to carry out an adjustment at some point. Still, near-term debt dynamics do not look particularly unfavorable. The structural growth slowdown — which has contributed at least marginally to fiscal deterioration — seems to be the more urgent problem.

The public sector primary budget surplus accounted for 1.6 percent of gross domestic product in the 12 months ended September 2013. Although state and local government finances have worsened somewhat, most of the deterioration has occurred at the federal level and more specifically in the treasury accounts, although the social security deficit has widened modestly as well. Of course, this worsening trend has occurred against the backdrop of sluggish growth. Indeed, since 2009 Brazilian public finances have become significantly more cyclical. Previously, the primary fiscal balance essentially stayed constant, regardless of growth. In the past several years, though, the balance has fluctuated in tune with economic trends (see chart 1).

Chart 1: Brazil real GDP (% y/y) and change in primary fiscal balance (% of GDP)

Source: JPMSI, Bacen, JPMAM; data and forecasts through 2013

Fiscal slippage, however, appears to go beyond purely cyclical developments. Assuming that the primary surplus winds up 2013 at roughly 1.3 percent of GDP, it will have swung 1.8 percentage points in two years during a period of weak but positive growth. One estimate of the output gap, generated by the Hodrick-Prescott filter, shows the economy weakening relative to potential during the past two years by about 2.1 percentage points (see chart 2). The well-known shortcomings of the H-P filter notwithstanding, other efforts at measuring the output gap produce broadly similar estimates. Public finances, then, have moved almost as much as the output gap since 2011. In OECD economies, where automatic stabilizers are prevalent, the cyclical elasticity of the fiscal accounts generally runs around 0.4. Public finances in developing countries like Brazil typically display much less sensitivity. Even assuming a multiplier of 0.25, which is probably a bit high, the cyclically adjusted primary fiscal balance appears to have slipped by roughly 1.2 percentage points of GDP in the past two years.

Chart 2: Brazil real GDP and H-P filter trend (1995 = 100, sa)

Source: JPMSI, JPMAM; data and forecasts through Q4 2013

As a corollary to the above point, the present level of the primary surplus, adjusted for the business cycle, probably stands only marginally above the actual reported figure, because the output gap itself is fairly small. The economy enjoyed a strong recovery in 2010 and appears to have begun overheating by the end of that year. Weaker growth since then has eliminated that problem but has probably opened up only a small gap in the other direction. Recent trends in the labor market, in which tightness has eased somewhat but the unemployment rate remains very low, support that contention. Again using a 0.25 fiscal multiplier, this year’s cyclically adjusted primary fiscal surplus would stand at 1.6 percent of GDP, compared with 1.3 percent for the actual figure and 2.8 percent for the cyclically adjusted balance in 2011 (see chart 3). Recent surpluses represent a level change compared with the early 2000s, when the cyclically adjusted surplus ran between 3 percent and 4 percent of GDP.

Chart 3: Brazil actual and cyclically adjusted primary fiscal surplus (% of GDP)

Source: JPMSI, Bacen, JPMAM; data and forecasts through 2013

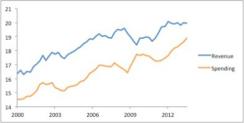

Trends in revenue and spending this year corroborate the notion that some structural slippage has occurred. Revenue growth has weakened recently, compared with its norm before the 2008 global financial crisis, but has remained reasonably strong. Indeed, in the six months to September, the central government’s intake rose 10.6 percent year-over-year, a pace slightly stronger than nominal GDP. More broadly, revenues as a share of GDP have essentially tracked sideways since the beginning of 2012 (see chart 4). Spending, on the other hand, has continued to climb rapidly. It increased 14.4 percent year-over-year during the middle two quarters of 2013, similar to its post-2000 clip. Spending has moved steadily higher relative to GDP: by 1.6 percentage points in the past 24 months. It appears that the government has not adapted its spending habits to a new, structurally lower pace of economic (and revenue) growth. As a result, the government’s footprint, already fairly large by the mid-2000s for a country at Brazil’s income level, has continued to expand.

Chart 4: Brazil federal government revenue and spending (% of GDP)

Source: Fazenda, JPMSI, JPMAM; data through Q3 2013

Does fiscal slippage threaten Brazil’s debt sustainability? The country has made progress on various fronts in recent years, with the net debt ratio falling and interest rates declining secularly. Some relaxation in public finances might thus be warranted. Two caveats, however, apply in this area. First, Brazil’s gross public debt has dropped less than its net debt, as some debt creation has funded asset accumulation, such as international reserves and claims on state-owned banks (see chart 5). Second, implied interest rates calculated from the behavior of actual interest payments suggest that gross debt is a relevant consideration. The implied interest rate using gross debt more closely matches trends in market Brazilian interest rates than if the net debt figures are used (see chart 6). This result most likely derives from the low income generated by the asset side of the public sector balance sheets. For example, the country’s international reserves are primarily invested in U.S. Treasuries and comparable securities. The debt sustainability exercise thus should focus on stabilizing gross debt or, alternatively, should apply an above-market interest rate to the level of net debt. Moreover, it seems likely that at some point fairly soon, the government will need to recapitalize BNDES, the Brazilian development bank, implying a net debt ratio several percentage points of GDP higher than the present reported figure.

Chart 5: Brazil public debt, net and gross (% of GDP)

Source: JPMSI; data through September 2013

Chart 6: Brazil public sector interest rate, using net and gross debt denominators (%)

Source: Bacen, JPMAM; data through September 2013

Assuming an eventual net debt ratio around 45 percent of GDP (compared with 35 percent, as shown in present figures) and applying a real interest rate of 7 percent (between the implied rates using net and gross debt figures) and a conservative potential GDP growth rate of 2.5 percent, the primary surplus required to stabilize debt would be roughly 2 percent of GDP. With considerable uncertainty about all three variables, the actual figure could lie on either side of that figure, although it seems unlikely to stand either below 1 percent of GDP or above 3 percent of GDP. Most likely, then, debt sustainability requires a somewhat higher primary fiscal surplus than the government is running, and at some point an adjustment will prove necessary. Still, an upward spiral of the debt ratio appears unlikely under the present circumstances, given that the actual primary surplus is not far below the stabilizing level. More likely: The debt ratio will drift gradually higher, as indeed it began to do in September.

From a creditworthiness and financial market standpoint, the apparent drop in the economy’s potential growth rate during the past few years looks like a more pressing concern than does fiscal slippage. The less favorable growth-inflation trade-off apparent since 2010 suggests that potential growth, previously thought to be in the range of 3.5 percent to 4.5 percent, has fallen to a rate closer to 2.5 percent. That pace seems insufficient to attract large-scale capital inflows in coming years. At the same time, meaningful fiscal deterioration has taken place, and the decline in the primary fiscal surplus goes beyond cyclical effects. The government’s somewhat cavalier attitude toward this worsening suggests an ongoing cause for concern for investors while at the same time not necessarily justifying an alarmist tone from market analysts. The more the fiscal balance slips in the short run, the greater — and more politically difficult hurdle — will be the eventually required correction. This combination of weaker growth and a less impressive fiscal effort appears to justify the widening in Brazil’s credit spreads this year relative to comparably rated Latin American borrowers such as Colombia, Peru and Panama. In the case of Brazil, this credit spread is 107 basis points, compared with 72, 68 and 87 for the other three countries, respectively. Reversing that market trend will likely require genuine policy change.

Read more about emerging markets.