Investors bracing for higher interest rates have been shunning U.S. Treasuries and snapping up alternatives such as bank loans and high-yield corporates, which tend to be more responsive to improving economic conditions than to rate changes. But this strategy may also expose such investors to market sensitivities that they did not think were part of the deal. There’s another way to go.

We’ve written before about how a strategy targeting stable, high-quality business models handles a variety of investor needs. It can smooth performance while capturing the long-term returns from equities more efficiently, or it can act as a third dimension of investing style uncorrelated with other active approaches, such as value and growth. But there is another use you may not have thought of: harvesting just the potential for return associated with high-quality, less volatile stocks by eliminating exposure to stock market fluctuations.

To understand the appeal of such an approach, recall that a portfolio of stocks screened based solely on their sensitivity to the market produced very attractive long-term returns. Sorting that same group for traits of strong fundamental quality — such as robust free cash flow generation, sustainable competitive advantages and good capital stewardship — generated even better results, as we’ve noted.

To extract this alpha potential, we hedge out the portion of the strategy’s returns that is associated with equity market participation. By shorting the market index in proportion to the portfolio’s below-market beta, its beta goes to zero, effectively untethering it from equity market movements.

The results are encouraging. In simulations going back to 1990, a hypothetical high-quality, low-volatility portfolio with no exposure to the market performed better than government bonds with similar risk and was far less volatile than high-yield credit. The end result was a risk-adjusted return superior to both (see chart 1).

Chart 1

But the true beauty of this absolute-return equity strategy lies in its diversification benefits within a total portfolio. These pluses stem from the fact that the sources of long-term returns of a high-quality, low-volatility equity portfolio — in particular, stable and sustainable profitability — tend to be very different from those of most bond strategies, whose returns are driven by interest rate levels and more economically sensitive credit fundamentals.

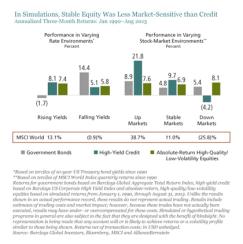

To illustrate, we have compared the three-month performances of government bonds; high-yield credit; and a hypothetical high-quality, low-volatility equity portfolio in different interest rate and stock market environments since 1990. The equity portfolio outperformed government bonds in rising and stable interest rate environments, with similar insensitivity to rates as high-yield credit. Unlike high-yield credit, however, this portfolio was also relatively insensitive to equity market fluctuations, resulting in better downside protection when equity markets slumped (see chart 2).

Chart 2

Whether you are worried about rising rates or merely looking for an alternative solution that offers bondlike characteristics with strong diversification benefits, we think a strategy that isolates the alpha from high-quality, lower-risk stocks may be the right fit.

Kent Hargis and Chris Marx are portfolio managers of the low-volatility equity services at AllianceBernstein.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AllianceBernstein portfolio-management teams.

MSCI makes no express or implied warranties or representations, and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indexes or any securities or financial products. This report is not approved, reviewed or produced by MSCI.