Perennial soccer power Brazil is hosting the 2014 FIFA World Cup. The Brazilian men’s national team has won the competition five times — more than any other country — and holds the record for most goals scored. The favorite to win the next World Cup also stands to benefit economically from the estimated 3.3 million tickets available for sale and the additional tourism income, much of it foreign, that will flow into the country. When it comes to Brazil’s economy as a whole, however, during the past year the market has not been seeing the World Cup host as fully in the game.

An investment favorite following the 2008 financial crisis, Brazil has watched its image slip among global investors to the bottom of the league standings. It was recently included as part of the so-called Fragile Five, the five emerging markets whose currencies were deemed by Morgan Stanley strategists the most vulnerable. Global emerging-markets equity fund portfolios have reduced their exposure to Brazil, from 13.4 percent in the second quarter of 2012 to 10.3 percent as of August, according to fund data from research firm Lipper.

But perhaps markets have judged Brazil too harshly. The country got off to a sound start with its series of reforms during the 1990s, instituting key changes and relatively sound macroeconomic policies, which are still in play. As conditions change, however, Brazil needs to adapt its game plan. Its main goals should include another round of reforms, as well as continued infrastructure improvement and measures to attract investment. (Read more: “Emerging Markets Face Mounting Challenges as Global Liquidity Dries Up”)

Brazil laid most of the groundwork for its structural reforms in the late 1990s. Compared with other emerging-markets countries, Brazil falls in the middle of the pack in terms of corruption perception, ease of doing business, human development, economic freedom and global competitiveness. After initial strong improvements on the sociopolitical side, Brazil has largely moved sideways since the global financial crisis; it has failed to use the past few years to improve its position further and missed a good opportunity to raise its growth level. Standard & Poor’s put Brazil on negative watch a few months ago, and Moody’s has recently downgraded the country’s rating outlook to stable, citing a requirement of GDP growth above 3 percent to turn the outlook positive again.

President Dilma Rousseff and her administration have recognized the challenges to long-term growth since she took office on January 1, 2011. So has the electorate, if the widespread street protests this June were any indication. Policymakers have started to respond, albeit not as coherently as we at Investec would have liked. There has been some progress, including important structural changes to the savings rate and required real pension return, and tax reductions in fuel and vehicles designed to control inflation and support economic activity.

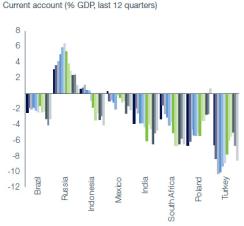

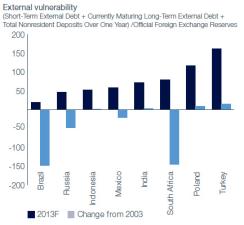

Another point in Brazil’s favor: Its current accounts and external vulnerability are not only substantially better than the rest of the Fragile Five (see charts), but they are also performing at levels at or above many other emerging markets. Brazil has a strong defense by way of its $376 billion in reserves and a central bank that is not afraid of preventing currency shocks. On the other hand, much has been made of Brazil’s current-account deficit, but we would argue that these concerns are a bit unwarranted. First, the negative forecast stemming from a sluggish start to the year fails to take into account the causes behind the poor numbers. Second, although undoubtedly there will be a modest increase in the deficit this year, closer analysis is warranted. Third, we should examine the factors behind the gradual improvement we see happening this quarter and into 2014.

Much of the downturn in the current-account deficit during the first half of 2013 was on the back of a sharp drop in the country’s trade surplus. Brazil’s oil and distillate trade posted two quarters of sizable deficits, driven by lower crude oil production. This decline is expected to normalize by year-end. Investment, which contracted by some 4 percent in 2012, has also put modest pressure on the trade account, as capital goods imports increased. Exports are likely to bounce back, helped by stable iron ore prices and stronger crop yields after weather-related problems in 2012. Stabilizing growth in China and the pickup in activity in neighbor and major trading partner Argentina also stand to favor Brazil with regard to its balance of trade.

Brazil should continue to attract plenty of foreign direct investment, which is expected to total about $65 billion in 2013 and would cover most, but not all, of its current-account financing. Portfolio flows are also expected to increase. Fixed-income inflows have already received a boost from the June repeal of the financial transactions tax, a move that has bolstered investors’ confidence.

Two factors that could hamper Brazil’s rebound are low savings and investment levels. Its savings rate staggers behind that of other Latin American and global emerging-markets peers. The country needs to boost investment to above 20 percent of its GDP. Private sector investment has been largely stagnant during the past three years. The system is too heavily dependent on the public sector, but government efforts thus far to boost infrastructure investment and encourage private sector participation have not met with much success.

Brazil remains a relatively closed economy, and growth in recent years has been driven by domestic consumption. The recent moderation in real wage growth, combined with modest interest rate tightening and stronger investment, is starting to aid production and soften consumption within the economy. However, there is a lot more work to be done. The challenge is to add capacity to bolster long-term trend growth and lower inflation structurally, rather than only cyclically.

Investment and building infrastructure will weigh on the budget, with government having to balance longer-term objectives and sustaining a sound macroeconomic framework. Brazil’s complicated tax laws have also had a stifling effect on production. But at the same time, the steps that Brazil has taken to simplify its tax code — with the hopes of spurring domestic and foreign private investment — have decreased revenues. This drying-up of public coffers has been compounded by the effects of an interest rate hike and a challenging global environment. Debt-to-GDP levels have steadily improved in recent years and are likely to trend sideways. This is disappointing relative to Brazil’s own performance, but much less so when compared with global peers.

The central bank’s inflation targeting has been one of Brazil’s macroeconomic successes in recent years. In turn, this policy ?has helped force real interest rates lower. Inflation has hovered near inflation targets during the past decade. Real yield compression has fizzled out, however, and remains very high by global standards. High levels of inflation on services, reflecting the past decade’s policy emphasis on minimum-wage hikes and social spending at the expense of capacity creation, are largely to blame and will need to be addressed before the inflation range can move structurally lower.

More recently, inflation expectations have been pushing toward the higher end of the central bank’s target range, eliciting a strong policy response, with hikes in short-term interest rates and aggressive currency intervention to prevent spillover effects that would result from a sharply weaker real. In the coming months, headline inflation should creep lower despite the stronger seasonal pattern through the end of this year. Much of this trend is likely to stem from the high base from 2012 and falling food inflation, containing rising expectations and allowing the interest rate hiking cycle to stop. With a steep curve and very high real yields, the market offers relative value over the short term when five-year real rates are compared with the inflation rates of emerging-markets peers like South Africa, Indonesia and Russia. But without further progress by Brazil in addressing the longer-term challenges, it is difficult to forecast further sustainable falls in real yields.

Vivienne Taberer is a portfolio manager with Investec Asset Management’s emerging-markets fixed-income team.

Read more about fixed-income asset management.