If you follow the headlines on investment in emerging markets, things have been rocky for a while now. Macroeconomic weakness has plagued developing economies for several years, and factors ranging from currency challenges to continued softness in commodity prices only add to the feeling that these markets won’t rebound any time soon.

None of this has dampened private equity’s enthusiasm for certain emerging-markets countries. PE firms have some $4 billion in dry powder earmarked for investment in sub-Saharan Africa, looking to capitalize on the “rising Africa” theme of strong growth and the rise of a middle class, reports the Overseas Development Institute, a London-based think tank. For example, buyout giant KKR & Co.is planning a $100 million pan-African investment program over the next year, according to an October statement by the New York–based firm. In April 2014 Washington-headquartered Carlyle Group closed a $700 million buyout and minority investment fund focused on sub-Saharan Africa.

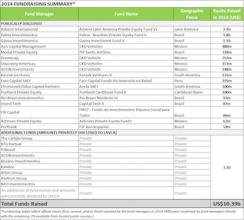

Last year fundraising reached new heights in Latin America, according to the New York–based Latin American Private Equity & Venture Capital Association (LAVCA). Capital committed to Latin American–dedicated private equity and venture capital funds totaled some $10.39 billion, beating the previous record of $10.27 billion, set in 2011, with money coming from firms such as Advent International, Axis Capital Management and Carlyle.

Click image to enlarge.

But choosing a region with powerful demographics and good growth potential only solves for half the equation. According to a new paper by Harvard Business School investment banking professor Josh Lerner and researchers Andrew Speen, Chris Allen and Ann Leamon, private equity firms must change how they invest in emerging countries if they want to succeed. The paper argues that classic control-oriented private equity often doesn’t work in these markets — and that sellers who are willing to make such deals could have less than honest motivations.

“By offering majority interest in the company, the entrepreneur may be signaling poor future growth prospects or that the business is already in such a state that current shareholders are eager to exit,” Lerner writes.

Emerging economies offer a demographic advantage: They have a budding consumer class, and with that comes an increased demand for health care, transportation and other services common to more developed economies. Many of the companies best positioned to capture these growth drivers are family-owned and hesitant to give away a majority stake when they know that the wind is at their backs, Lerner says. If such companies seek investment at all, they want a real growth partner. “There’s an appetite within many of these businesses to get someone who isn’t in the family at the table and can bring expertise that isn’t there,” Lerner tells Institutional Investor.

Tom Speechley, a New York–based senior partner and CEO of Abraaj North America, the U.S. arm of Abraaj Group, a $9 billion emerging-markets-focused private equity firm, says that how a transaction is structured makes a real difference. “You can actually get effective control even in a minority situation,” explains Speechley, whose firm contributed transaction data to Lerner’s paper. “We are active investors, and we definitely want control of the strategic direction and growth of the company. We form a partnership with management, and that partnership is how we get effective control of the growth agenda of the business.”

Abraaj recently led a $60 million Series C funding round with Dubai-based Careem, an app-based car service that works much like Uber. This minority stake, one of the largest investments in the Middle East’s emerging technology sector, will be used to expand Careem into new markets throughout the region.

Leaving the management team in place can also solve another problem unique to growth markets: a lack of local managerial talent. In contrast to U.S. buyout scenarios, it’s tough to hold a casting call for a new CEO in sub-Saharan Africa, where there’s no flock of MBAs waiting in the wings.

Going in as a partner in these economies presents its own challenges, though. General partners and investors have to be prepared to build not only a company but also often much of the supply chain and business vertical that a company needs to succeed.

Johnny El Hachem, CEO of Paris-based Edmond de Rothschild Private Equity, says that bringing relationships and other expertise to the table is a competitive advantage. His €3 billion ($3.2 billion) firm makes only minority investments. “Being a minority investor isn’t an issue anymore, because you can achieve alignment on the major strategic issues, especially if you predefine the exit route,” El Hachem explains, adding that general partners can also intervene if necessary.

When minority investors want to exit, who’s buying? In many cases, it’s a strategic buyer, or it can be the original sponsor. LAVCA president Cate Ambrose says that as Latin American companies have started to mature and institutionalize through early-stage investments, more big-name strategic buyers are looking at the region. “We have already seen a few acquisitions of VC-backed start-ups by international companies like Priceline, Eventbrite, Sage Group,” she says.

Later-stage investors trade away a bit of multiple expansion for a more mature company, but Harvard’s Lerner says that specialization among private equity firms also drives secondary sales. “There are some GPs who specialize in the early stage, and then there are others who are better suited to take a company from $500 million in revenues to over $1 billion,” he explains.

The research suggests that for general partners willing to make minority investments and do the heavy lifting, returns are often comparable to those from majority investments. Exit data from Abraaj in the Lerner paper show little difference between majority and minority exit returns. Abraaj reported an average return of 2.3 times the amount invested for majority stakes, compared with 2.1 times for minority investments. Those figures cover nine majority investments and 55 minority investments made by the firm since 2002.

Data from the World Bank Group’s International Finance Corp. included in the paper, which covers 312 emerging-markets deals fully exited by the end of 2009, shake out similarly. Although the IFC doesn’t display its data by individual deal, the average returns of minority and majority investments are similar, as shown in the following chart.

The holding period on minority investments also tends to be shorter. The paper looks at exit data year by year to take into account the cyclical nature of the exit environment. For majority and minority investments that exited in the same year, the holding period on minority investments is often at least 12 months shorter.

“People assume that the big risks are geopolitical, macro country risks, when in fact what makes or breaks returns is the specific circumstances of the individual companies you invest in,” Abraaj’s Speechley says. “That’s what the best private equity firms do in markets: They take the risk out of markets.”

Get more on alternatives.