To view a PDF of this story click here.

As investors continue to seek yield and respond to evolving dynamics around the globe, a number of specifi c equity investment strategies have come to the fore. Sustainability is drawing greater investor interest. Closed-end funds, often overlooked, provide advantageous structural benefi ts for income and exposures. And many investors are looking closely at the small-cap value space as economic activity accelerates.

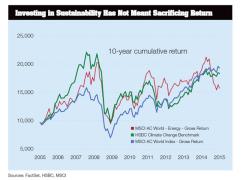

Amid increasing global demand for sustainable investments — companies that address environmental, social responsibility and corporate governance (ESG) issues to generate profits — the opportunity set is expanding rapidly. The market share and market capitalizations of companies that are addressing sustainability issues are expected to be significantly larger a decade from now than they are today. Still, many investment professionals seem to underestimate the scope of opportunities in this area. “Our approach is to invest in companies that are directly solving for environmental stewardship and providing a solid return for our clients,” says Alan Hsu, portfolio manager at Wellington Management Company. “We refer to it as the ‘double bottom line.’”

Investor adoption has been slow, largely because of concerns that investing in ESG means sacrificing return. However, the long-term case is compelling. Comparing the diversified global index and energy subsector indexes with companies that provide sustainable solutions (represented by the HSBC Global Climate Change Benchmark Index), the returns are competitive going back ten years or more. “As demand grows, the value of sustainability-related assets will rise,” says Hsu.

The opportunity set spans a range of companies that are solving sustainability challenges: low-carbon electricity, low-carbon transportation, energy efficiency, and water and other resource management. “We invest in those companies for which ESG is a revenue source, not a cost,” Hsu explains. This includes capital formation and financing for sustainable infrastructure; manufacturers of enabling technology, such as wind turbines, solar power equipment and micro grids; asset-creation companies involved in construction efficiency or wastewater management; and asset owners like solar and wind farm operators.

ESG is increasingly a global discipline. The demands around sustainability from investors — as well as consumers — affect policies around the world, and global analytical coverage is critical for identifying market leaders and evaluating risks.

China is a good case study. “China is just catching up with environmental issues, but it’s doing so very quickly,” says Juanjuan Shen, global industry analyst at Wellington Management Company. “We’re definitely seeing much heightened environmental awareness and demand for improvement in response to heavy pollution from burning fossil fuels.” During the past three years, the Chinese government has issued numerous policies, directives and executive orders to steer the country’s energy consumption toward cleaner sources. Tighter emissions and efficiency standards have increased the cost of using fossil fuels. Executive orders to local governments and incentives for developers to produce solar and wind power have stimulated investment in cleaner energy. “China now has the largest pipeline for new sustainable energy projects in the world,” Shen says, “and we want to be on the right side of this movement and the government’s efforts.”

Hsu and his team emphasize the value of Wellington Management’s ESG specialists. “Our dedicated, experienced research team identifies ESG opportunities, as well as risks,” he says. The team performs reviews of many client portfolios and helps Hsu, Shen and others engage with management teams to drive improvements that mitigate risk. “Th is often falls outside of fundamental research of ESG issues,” says Hsu, “but it’s a key component of our approach.”

Closed-End Funds: Structural Advantages

In an environment in which investors are looking for high yield and low risk, closed-end funds are underappreciated and underutilized when compared with traditional mutual funds and other investment choices. This is particularly true when investors are considering asset-appreciation and income strategies, as well as the access to less liquid investment categories that they can provide. “Most investors simply don’t realize that the very structure of a closed-end fund offers a number of advantages,” says Rennie McConnochie, business development manager at Aberdeen Asset Management Company.

Although closed-end funds are similar to conventionally managed mutual funds, there is one significant difference: They are represented by a fixed number of shares, which are sold on an exchange, originally through an initial public offering. In that sense, they resemble corporate equities and trade just like stocks. Contrary to a popular misconception, closed-end funds are not “closed” to new investors. They simply have a fixed number of shares available for daily buying and selling. “This gives them a stable asset base, which allows fund managers to follow their investment strategies without having to worry about investing new inflows or meeting redemption requests,” McConnochie says. This structure also allows the fund to be fully invested at all times. “There is no cash drag,” he notes. Traditional funds must maintain cash reserves in case of redemptions, which represents performance inefficiencies. There is no risk of selling low in a down market to meet outflows or buying high to invest new inflows. “We don’t end up with the typical barbell portfolio, with liquid investments on one side and high return assets on the other, to handle liquidity concerns,” McConnochie says. Furthermore, closed-end funds tend to have lower expense ratios. “There are no costs for distributing, issuing or redeeming shares, which leads to much lower fees,” says Renee Baker, marketing manager at Aberdeen Asset Management Company.

Because closed-end funds trade on an exchange, the price fluctuates with supply and demand in the market. Therefore they can be bought and sold above or below their net asset value. Investors can use any of the usual stock-trading methods, including market and limit orders, stops, short sales and margin trading. And because investors can buy or sell closed-end fund shares in real time during the trading day, they have the ability to make investment decisions using current information.

“Most closed-end funds are now trading at a discount, so there’s a compelling opportunity,” says McConnochie. “It’s possible now to pay only 90 cents for a dollar’s worth of performance.” Indeed, yields have been an impressive 5 to 7 percent. Although it’s true that exchange-traded funds have turned in similar performance over the past several years and that many active managers have underperformed market benchmarks, it’s important to look at the total return on a closed-end fund. “While the net asset value might have been $24 last year and it might be $24 this year, there will likely be significant distributions and dividends from the fund, which aren’t always obvious from performance reports,” he explains. Investors can always opt to reinvest dividends, compounding the rate of earning distributions. “The return elements are net asset value accretion plus distributions of dividends and capital gains,” he says. The discount of share price to NAV provides a measure of value. “It’s this perceived complication that can turn financial advisers off closed-end funds,” McConnochie says.

The closed-end structure is well suited to investing in less liquid parts of the market, and Aberdeen’s U.S. closed-end funds provide access to the world’s emerging markets — both specific regions and particular countries. “You don’t have to take a haircut to get out, which mitigates having to worry about redemptions,” says McConnochie.

The active management of closed end funds tends to be an advantage for less liquid and more complicated asset classes. “Active management means you can boost returns, plus there is easy access to research and expertise,” Baker says. Each fund benefits from a diligent research process and disciplined portfolio construction.“We have a ‘boots on the ground’ approach, and we understand the risks,” she notes. With teams of analysts and portfolio managers in 26 countries, Aberdeen meets with and researches companies three to five years in advance of making an investment. “It’s important for us to understand each specific market and how they work together regionally and globally,” Baker says. This means diminished risks for exposure to China, India, Japan and other markets.

“We are low-turnover investors, portfolio turning over each year,” says McConnochie. Th is mostly consists of taking advantage of price dips for quality stocks or trimming back on those that have outperformed. “We’re very much buy-and-hold, which keeps costs lower,” he says. Holding times can be ten, 15 or 20 years — rare among investment managers. In all markets and in each of its funds, Aberdeen looks for high-quality names that maintain strong balance sheets, high return on equity and sustainable business models. “We also make sure we buy at a good price,” McConnochie says.

Commitment to the secondary market is also critical, as it supports liquidity. This means actively keeping in touch with investors and advisers through education, outreach, surveys and marketing programs to increase new investment. Without support in the secondary market, financial advisers and investors tend to generally lose confidence in closedend funds. “We’re committed to this market, and it’s fundamentally, incredibly important to provide this type of support to our investors,” says Baker.

Small-Cap Value: Opportunities in a Growing Economy

“We like where value is positioned today,” says Lance James, senior portfolio manager at RBC Global Asset Management. With small-cap equities in general having performed well over the past several years, and as investors look at equity markets and consider active versus passive strategies, there is more appetite for active management within the small-cap and midcap segments. “Our focus is to take advantage of market inefficiencies where there is mispricing versus the fundamentals in the small-cap space,” he says. “There is generally more consistent outperformance by small-cap value managers versus their index than in other equity categories.”

A dedicated small-cap value allocation within a balanced portfolio may lead to both higher returns and lower volatility. “We usually invest in companies that grind it out over time,” James says. By sector, there is a concentration in financials, mainly regional banks, specialty finance companies, insurers and real estate investment trusts that are trading at attractive valuations. Utilities, industrials and consumer goods are also favored categories. “We look for those companies with a competitive advantage, with a proven product or service,” James explains. Through the slow economic recovery, the strongest of these companies have survived the downturn, cut costs and increased sales as the recovery has accelerated. The buying signal is oft en a change in a company’s near-term profitability improvement potential, which could be triggered by improving macroeconomic conditions, industry consolidation, a change in management, a new product launch or the end of a capital spending cycle. “As long as we produce long-term returns above the index benchmark, there will always be an institutional demand for active management,” James says.

By Howard Moore