After a long postcrisis rally, investors have faced much more challenging conditions in the past year.

The U.S. stock market has essentially gone sideways, while volatility, long subdued by the calming power of quantitative easing, staged a dramatic comeback. After staying below 20 for all of 2013 and most of 2014, the CBOE Volatility Index (VIX) broke above that level in October 2014 and has sustained several periods above 20 since then.

For traders and investors looking to establish or liquidate a position carefully to avoid moving the market, the choppy conditions pose a challenge. “The greater the volatility, the more likely prices are to move in my favor or against me while I’m looking to trade without impacting the market,” says Alex Clode, business manager for trade analytics at Bloomberg. “You would expect slightly larger costs on aggregate in those periods.”

Trading costs actually fell over the past year, according to Institutional Investor’s latest Transaction Cost Analysis survey, yet although market impact costs also declined on average, the savings weren’t shared across the board. “The lower market impact trend has been accompanied by a widening of the distribution, with fatter tails,” says David Griffin, New York–based product manager for TCA analytics at Elkins/McSherry, a division of State Street Corp., which conducted the survey. “This is probably a result of greater volatility in the market.”

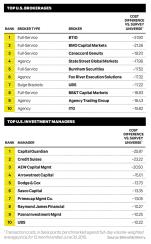

San Francisco–based BTIG ranks first among U.S. brokers in this year’s survey with an average cost per transaction of 31.90 basis points below the volume-weighted average price for the universe covered in the year ended June 30. Capital Guardian, headquartered in Charlotte, North Carolina, takes the No. 1 spot among investment managers with an average cost of 25.97 basis points below VWAP. On a global basis Russell Implementation Services in Seattle tops the ranking of brokers with a cost of 35.06 basis points below VWAP, while New York’s MetLife leads among investment managers with a cost of 49.55 basis points below VWAP.

Volatility spiked dramatically in late August, when China’s bear market and surprise devaluation shook markets around the world. The VIX hit a six-and-a-half-year high of 53 on August 24. “That shined a bright light on the structure of capital markets,” says Bill Lenich, head of program trading at Weeden & Co. The Greenwich, Connecticut, firm ranks 13th among U.S. brokers and fourth globally in the survey.

In particular, the halting and reopening of trading for individual stocks didn’t run smoothly on August 24, distorting prices of the stocks themselves and of derivatives and exchange-traded funds tied to those stocks, he says. “Both the buy and sell side are concerned about fairness,” he says. “There is reason to question whether the prices that day were good and fair.” As a result, Lenich expects regulators and possibly exchanges to implement changes to make markets “more transparent and fluid and to guarantee more efficient price discovery.”

The stock market’s structural weaknesses become more apparent in times of severe volatility, Lenich notes: “Any time there’s extreme market volatility, the question is how do I protect my order flow and participate fairly and efficiently?”

The wider distribution of market impact will likely continue if volatility remains elevated, says Griffin, who adds, “Based on world events, I can’t see volatility going away anytime soon.”

Volatility can take many forms. U.S. regulators have shown an interest in the volatility that short-term traders can create in mutual funds and exchange-traded funds. In September the Securities and Exchange Commission put out for comment a proposal that would require mutual funds and ETFs to establish and disclose liquidity risk management policies to ensure that investors can redeem their shares in a timely manner. The SEC also proposed allowing mutual funds to adopt so-called swing pricing, whereby funds adjust their net asset values when purchases or redemptions of fund units exceed a certain percentage of the fund’s net asset value — its “swing threshold.” By raising a fund’s NAV when there is heavy buying and lowering it at times of heavy selling, such pricing aims to protect long-term shareholders from dilution caused by short-term traders and help funds manage their liquidity risk. An SEC spokeswoman declined to comment on the proposal.

Griffin thinks swing pricing is a great idea, noting that it has already been implemented in the U.K. and elsewhere in Europe. “The basic concept makes a lot of sense,” he says. “Long-term investors shouldn’t have to endure the comings and goings of a subset.”

Meanwhile, investors and brokers continue to struggle with the consequences of market fragmentation. Traders can choose from a host of public exchanges and private dark pools to execute orders. “The challenge is how to find the highest-quality fair and liquid market when we have a choice of 30-plus places to go?” says Andrew Upward, head of market structure at Weeden. “When do we use them, and how do we judge our quality of execution?”

TCA practitioners face quantitative and qualitative issues, he says. The quantitative part involves measuring the execution quality of the trade against different benchmarks. The qualitative part includes understanding how the venue operates, says Upward: “How are the orders ranked; what types of counterparties will be at the top of the queue? Who will I be interacting with, and what kind of liquidity do they offer?”

Charlie Susi, co-head of institutional trading at KCG, which ranks 11th among brokers in the survey, says that with more than 50 electronic trading platforms available across U.S. markets, there’s a trade-off between having a comprehensive selection of places to trade and the complexity of dealing through so many entities. “There’s often only meaningful liquidity in a small subset of those,” he says. “You’re forced, however, to understand every venue because one might be the only place to get the right liquidity at that moment.”

Brokers can face a conflict of interest on exchanges that offer rebates to players providing liquidity and charge fees to those who consume it, known as maker-taker pricing. “Brokers are tempted to route to venues that give them better economics but don’t necessarily give clients the best price,” says Upward.

Weeden is agnostic about exchange fees and rebates, focusing solely on getting its customers the best price, he says. Trading on taker-maker markets, which charge brokers a fee for providing liquidity, can improve customer outcomes in some cases, he adds. “Trading on these venues gives us a better chance of capturing the spread, even though it costs us money,” Upward says.

Not everyone is enamored with transaction cost analysis. “I don’t embrace it as much as others,” says Thomas Garcia, head of equity trading for Thornburg Investment Management. “I like it, but it’s not the end-all or be-all.” The real objective for Garcia is maximizing returns for the shareholders of Thornburg funds. Traders often lose sight of that goal, he says: “You don’t want TCA to be the god; you want the god to be your shareholders.”

Garcia offers an example where the cost of a single transaction was misleading from a broader perspective. Several years ago Thornburg portfolio managers owned a stock that was in a sustained downtrend: “We decided to sell on a Monday, and when I started selling, the stock kept going down, down, down,” he recalls. “We had so much that I couldn’t complete the selling early in the day. Finally, at the end of the day, with the stock at its low, someone said, ‘I have a block to buy.’?” Garcia sold to the counterparty and closed out the firm’s position.

The next day the company preannounced an earnings decline of 20 to 30 percent, and shares plunged further, Garcia says. In terms of TCA, “my trade was the worst of the quarter when measured against arrival and VWAP,” he explains. “I looked bad versus the benchmark, but do you think my shareholders cared? I saved them a lot of money.”

The ease and cost of conducting transactions isn’t a matter of interest only for equities, of course. Investors are increasingly applying transaction cost analysis to the bond market, but it’s not easy. “There’s a massive universe of bonds, a vast amount of which don’t trade frequently, sometimes for weeks or months,” explains Griffin. A typical bond will trade actively for only a few weeks after issuance. “Every month there is a whole new set of assets,” he adds.

Most bonds also don’t trade on an exchange. “It’s difficult to get a meaningful price for benchmarks, so measuring trades can be very difficult,” says Bloomberg’s Clode. The first step for TCA practitioners is to gather pretrade prices to measure execution, he says. That’s easier to do now that electronic brokers are asking dealers for price quotes and selecting the best ones, he says. Still, it can be arduous to get executable prices as opposed to indicative ones. “TCA is still in its infancy for fixed income,” Clode says.