The Chinese craze for pricey Japanese-made diapers may change the way you think about investing in developing economies. It’s just one of the many trends we see incubating the next generation of winners in emerging markets.

We’re keeping a close eye on the changing shopping habits of the growing emerging-markets middle class, which is showing a voracious appetite for premium-priced goods. This trend not only reveals valuable clues about future consumer-spending patterns, but it also shows that the best plays in emerging equities are not necessarily homegrown.

For the past few years, affluent Chinese parents have insisted on swaddling their babies in Merries disposable diapers, a brand made by Japan’s Kao Corp. Not only that, they have also been paying a lot more for Japanese-made diapers than for a similar product made by Kao’s Chinese factory (see chart 1).

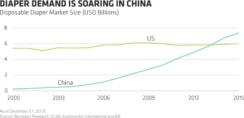

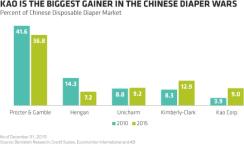

As a result, as demand for disposable diapers has soared (see chart 2), relative newcomer Kao has seen its market share in China surge, even while leading player Procter & Gamble Co. and local rival Hengan International Group Co. have lost ground (see chart 3). And the Chinese appetite for Merries helped drive a nearly threefold increase in profits at Kao’s Human Health Care Business from 2012 to 2015.

What does this mean for investors who are trying to understand the new emerging-markets landscape? We spot three key themes:

Premiumization. The desire for upmarket products is abundantly evident among China’s middle class, and it is breathing new life into the sales of many Western brands — from U.S.-made Steinway & Sons pianos and Mattel Barbie dolls to lingerie from Italy’s La Perla. Although P&G pioneered the disposable diaper market in China, it has continued to target the mass consumer, relying on local production to manufacture low-priced diapers. By contrast, Kao has focused on the premium niche. With its touted superabsorbent polymer technology — not to mention its “Made in Japan” label, which seems to guarantee premium quality — the Merries diaper has become a coveted brand among high-end consumers. In fact, an estimated 90 percent of Kao’s sales come from premium products, versus 25 percent for P&G and 40 percent for Japanese company Unicharm Corp.

The best China plays aren’t necessarily Chinese. As consumer demand shifts toward more premium products — and as questions continue to arise about product authenticity — there may be an increasing number of attractive opportunities for non-Chinese companies with manufacturing located outside of the country. We expect to see similar cases pop up across emerging-markets economies, providing investors with what may be better way to tap into local growth.

E-commerce on the rise. Kao began focusing on the online channel at the very moment when e-commerce was growing rapidly, at the expense of traditional channels. The Chinese are avid online shoppers, increasingly via their mobile phones. According to a proprietary AllianceBernstein research survey, e-commerce penetration of the Chinese household and personal care category rose from just 3 percent in 2013 to 21 percent in 2015. And the online channel is particularly appealing to high-end consumers, because of its convenience, high likelihood of product authenticity — a major concern in China — and broad product assortment.

New eras call for new game plans. Emerging economies look a lot different from how they did not that long ago. What worked for investors over the past decade isn’t likely to succeed in the years ahead. So, don’t assume the mass market is where the action is. Pay attention to trends in e-commerce. And — maybe most important — look beyond a country’s borders for the next generation of emerging-markets success stories.

Sammy Suzuki is the portfolio manager of strategic core equities at AllianceBernstein in New York.

See AB’s disclaimer.

Get more on equities.