By Blu Putnam, CME Group

AT A GLANCE

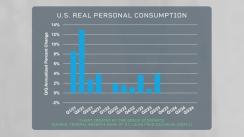

- U.S. real personal consumption has held up well in the face of higher interest rates because jobs kept growing.

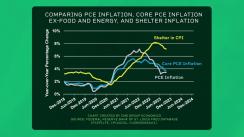

- Inflation has receded in virtually every category, although shelter is coming down more slowly due to the confusing and lagged calculation of owners’ equivalent rent.

We entered 2023 with a pessimistic consensus outlook for U.S. economic performance and for how rapidly inflation might recede. As it happened, there was no recession, and personal consumption posted sustained strength. Inflation, except shelter, declined dramatically from its 2022 peak.

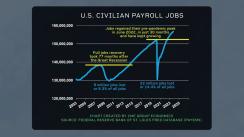

The big economic driver in 2023 was job growth. Jobs had recovered all their pandemic losses by mid-2022 and continued to post strong growth in 2023, partly due to many people returning to the labor force.

When the economy is adding jobs, people are willing to spend money. The key for real GDP in 2023 was the strong job growth that led to robust personal consumption spending. For 2024, labor force growth and job growth are anticipated by many to slow down from the unexpectedly strong pace of 2023, leading to slower real GDP growth in 2024.

And there is still plenty of debate about whether a slowdown in 2024 could turn into a recession. Followers of the inverted yield curve will point out that it was only in Q4 2023 that the yield curve decisively inverted (meaning short-term rates are higher than long-term yields). It is often cited that it takes 12 to 18 months after a yield curve inversion for a recession to commence. Using that math, Q2 2024 would be the time for economic weakness to appear based on this theory. Only time will tell.

The rapid pace of inflation receding in the first half of 2023 was a very pleasant surprise. Indeed, inflation is coming under control by virtually every measure except one: shelter. The calculation of shelter inflation is highly controversial for its use of owners’ equivalent rent, which assumes the homeowner rents his house to himself and receives the income. This is an economic fiction that many argue dramatically distorts headline CPI, given that owners’ equivalent rent is 25% of the price index.

Once one removes owners’ equivalent rent from the inflation calculation, inflation is only 2%, and one can better appreciate why the Federal Reserve has chosen to pause its rate hikes, even as it keeps its options open to raise rates if inflation were to unexpectedly rise again.

The bottom line is that monetary policy reached a restrictive stance in late 2022 and was tightened a little more in 2023. For a data dependent Fed, inflation and jobs data for 2024 will guide us as to what might happen next. Good numbers on inflation or a recession might mean rate cuts. Otherwise, the Fed might just keep rates higher for longer.