In 2022, investment decision makers at insurance companies identified three factors – inflation risk (63% of respondents), risk of recession (50%), and rising interest rates (39%) – as the most serious macroeconomic considerations for insurers’ investment strategies in the near term. (See “Adapt and Thrive: Insurers Seek Opportunity in the Changing World.”)

Now, as insurers head into the final months of 2023, they face familiar challenges in managing their portfolios that may well be as acute now than in years past. The U.S. Federal Reserve has raised rates eight times since the beginning of 2022, effectively tripling the federal funds rate and driving it to its highest level in 22 years. As of August 2023, Fed policy seems to have balanced inflation, growth, and interest rates, especially in the United States, but insurance CIOs with a long and circumspect view may well remain cautious.

This shift in Fed policy may be welcome news for some insurers, as it brings higher yields on fixed income assets and offers valuation relief for the liability side of the ALM equation. Accordingly, insurance companies are likely to make good on their plans for a robust review of their strategic asset allocation, as revealed in the 2022 BlackRock insurance study. Such strategic allocation reviews are less likely to bring a dramatic realignment than incremental shifts in how asset classes are managed, according to the 2022 study. “Rather than prompting big shifts across asset classes, the new environment is leading us to rethink how each asset class is managed,” says the Group CIO of global insurance giant Generali. “Beta will be less relevant; more active and high-conviction strategies will be critical, including private assets,” he says. He and his team are not alone, as others are embracing private markets. “We have allocated approximately 35% of our new money to private assets over the past five years,” says the CIO of Lincoln Insurance, and we expect to continue to grow that allocation into the future, focusing on asset classes with strong underwriting processes, protective covenants, and proven risk-adjusted returns to provide downside protection in a decelerating economy.”

Meanwhile, regulatory oversight of the insurance industry around the world is changing materially. In the United States, insurers now must model and report their current and expected credit losses under the new CECL mandate, comply with post-Dodd Frank regulatory mandates, and adapt to other significant changes to the insurance regulatory regime. European regulation of insurance is similarly experiencing shifting mandates from individual countries and the European Union at large. Elsewhere, an executive from Sumitomo Life Insurance company says, “We will invest in technology as we prepare for the new regulatory regime. Reporting requirements will most likely change so we will need to adapt our capability there. From an ALM perspective we are considering the integration of quantitative simulation and risk management methods.”

Amid these and other shifts in asset allocation and regulatory requirements, the need for technology that brings order and discipline to insurers’ investment process seems increasingly clear. But, today, that order and discipline is governed by the quality, accuracy, and consistency of the data available—delivered as a common language across teams. Nearly two-thirds of respondents in the 2022 study anticipate that technology and digital transformation will be a primary driver of the insurance industry in the years ahead; sadly, 59% of study participants also lament the technical challenges in upgrading their legacy infrastructure build on heterogenous systems from many vendors on many platforms.

Good news for insurers with complex operating models and legacy systems

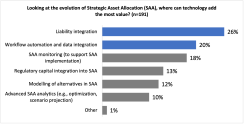

As insurers look to private markets and other new asset classes, their legacy systems, built piece by piece, year after year, become increasingly cumbersome to use and costly to maintain. Perhaps most troublingly, they become a less effective tool with which to manage insurers’ strategic and tactical portfolios and comply with the moving target of regulatory compliance. Indeed, a preview of the embargoed data from BlackRock’s 2023 insurance study reveals that insurance investment decision makers seek technology that supports integration of asset management with liability management more effectively, as shown in the chart below:

The good news is this: Technology in the form of platforms-as-a-service can provide data and analysis for investment decision making, reporting, and regulatory compliance for insurance companies. And the application of artificial intelligence to investment management may soon offer next-generation solutions that can disrupt the insurance industry further. Investment management data and technology are also widely available as services and accessible to people who aren’t software engineers. Accordingly, multi-year IT projects and lengthy development timelines may give way to brisker deployment of first-rate data and technology solutions for insurers in the years ahead.

Insurance companies also face increasing competition from their most ambitious peers, which have adopted new technology to streamline their investment decision making, portfolio management, and regulatory compliance activities. Insurance management teams are wise to ask whether they have the data and understanding to build, manage, and report on portfolio segments across all of their increasingly broad asset classes. Do they manage strategic and tactical allocations in ways that are scalable and will support their underwriting and regulatory mandates? Will they be able to attract the top talent required to manage a highly dynamic insurance portfolio? Can they position their firms as acquirers or valued acquisition targets? And ultimately, can they achieve all this while contributing to the growth and scale their firms?

The answers to these and other questions are tied to the efficiency and effectiveness of an insurer’s operating model–that is, the combination of systems and processes that it uses to manage its assets and liabilities, support underwriting, and comply with expanding regulatory mandates. Put more simply, an “efficient” operating model is a means through which insurers can manage their businesses while maintaining or improving their investment decision making, financial performance, and responses to regulatory mandates.

As insurance companies wrestle with how to improve their operating models, they are wise to consider the potential business impact of deploying a robust investment management platform. Four metrics offer an especially useful framework for assessing the financial and operating impact of a highly efficient, recast set of systems for managing insurance assets, modeling risk, and complying with regulation:

- Technology and operations spending. How much can the insurance firm save by lowering middle- and back-office costs? Such savings may include the licensing and staff cost of decommissioned out-of-date systems and data feeds, along with the future costs avoided by relying on a platform provider’s development team rather than legacy systems and their developers and implementers.

- Greater efficiency, productivity, and support for underwriting, investment and regulatory teams. How much time and attention can be freed up among staff and top talent across an insurers’ underwriting? Can we increase connectivity, communication, and collaboration between the front, middle, and back office? How much time and money can be saved by providing better support for underwriting and other business functions – and by having investment staff focus on high-value activities such as risk modeling and asset allocations rather than, say, reconciling cash balances?

- AUM growth. How can a more productive investment organization allow the business to scale dramatically without adding additional resources? How can a new technology platform support the firm as it brings new offerings to market? How can the technology platform deliver new products, onboarding new asset types, or expansion into new regions?

- Operating margin. How do you improve operating models without eating into performance?

While each of these elements may be transformative at the macro level, these and other opportunities become reality for insurers through analytically intensive risk modeling and deft execution at the individual firm level. For insurance companies to do so, they need the right underlying mechanism – robust technology and data – to support their risk, investment management, and regulatory processes. Insurers with such investment management systems may be well positioned to model their risks effectively, provide the unique investment outcomes required to meet underwriting commitments and comply with regulators’ expanding requirements.