Many investors in emerging markets believe that identifying the fastest-growing economies is the key to finding higher returns. But while this approach has been effective in fixed-income investing, our research shows that it’s fairly useless for guiding country selection in developing-markets equities.

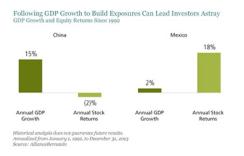

Imagine that it’s the early 1990s and your crystal ball has identified an emerging-markets nation whose economy is on the cusp of growing more than 20-fold over the next two decades. You’d probably think you had found the investment winner of a lifetime. But you’d be wrong. That country was China. Despite compound annual gross domestic product (GDP) growth of 15 percent since 1992, Chinese stocks fell by an annualized 2 percent through December 31, 2013 (see chart 1).

Now, what if the same crystal ball also — correctly — predicted that Mexico was headed for low-single-digit GDP growth over that same 20-year period? You’d likely look for better investment opportunities elsewhere. And you’d be wrong again. Mexican stocks have delivered annualized gains of more than 18 percent since 1992, placing them among the period’s best performers, despite 2.4 percent annual GDP growth.

“Follow the GDP growth” is a seductive mantra. After all, stock prices ultimately track growth in corporate profits, which then feed into GDP by way of spending and investment. What’s more, managing country-specific risks is important for equity portfolios, especially in emerging markets, where stock market volatility and currency fluctuations are more pronounced than in developed economies.

But our research suggests that many economic statistics have shown little or no predictive value in helping investors pick countries or stocks within developing markets over the past 20 years. Even if you knew exactly what a country’s nominal or real GDP growth per capita would be for the coming year, it wouldn’t have provided any predictive insight on the performance of that country’s equity market over that period.

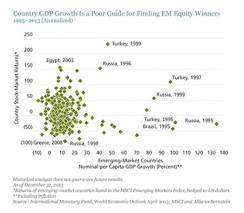

Indeed, we found little relationship between a country’s economic output growth in any given year and its equity returns during that time (see chart 2). The results were similar whether we looked at nominal, real or per capita GDP growth. For this analysis, we used hedged equity return data, which best reflects the experience of nondomestic investors by factoring out local-currency translation effects. In U.S. dollar terms, the correlation between GDP growth and equity returns is actually fairly tight, but this is primarily because of currency translation effects. In fact, the relationship between nominal GDP growth in local-currency terms and equity returns hedged to U.S. dollars is practically nonexistent.

Stock returns are a function of company earnings growth and the price multiple paid for those earnings. Earnings depend more on competitive positioning, strategic focus, industry dynamics and quality of management than on the underlying economy. That’s why Mexican companies were able to generate high returns for stock investors — by delivering fast earnings growth — despite the lackluster economy.

Valuation is important too. During the 1994–’95 Tequila crisis, sentiment toward Mexican stocks was particularly poor and they traded at under six times earnings. Having since delivered solid profitability for two decades, they now trade at a multiple four times higher. Earnings grew even faster over this period, but the rise in the multiple assigned to those earnings has been an important source of return. By contrast, Chinese stocks listed in the early 1990s have seen neither earnings growth nor multiple expansion.

The composition of a country’s stock market also helps explain the disconnect between equity market returns and GDP growth. The markets track the profits only of a country’s existing pool of publicly traded companies, which may not be very representative of underlying economic activity. For example, the MSCI China Index was launched in 1992 with only 24 constituents; some important sectors, such as energy, telecoms and technology, were not represented at all. Following two lively decades of initial public offerings, there are now 141 constituents across a far broader spectrum of sectors that include many fast-growing and dynamic companies. As a result, Chinese equity returns have improved markedly over the past ten years.

We’re not saying that what’s happening at the country level isn’t important to equity investors. It is. But the fundamental gauges of companies actually listed on local exchanges have proved to be much better guides than macro trends for finding stocks with outperformance potential.

Morgan Harting is an emerging-markets portfolio manager and Nelson Yu is the co-head of equities quantitative research at AllianceBernstein in New York.

See AllianceBernstein’s disclaimer.

Get more on emerging markets and on equities.