Much of the unbridled enthusiasm around emerging-markets countries has dissipated in recent years. Economic growth rates have fallen by nearly half from their pre-2008 highs. Although emerging-markets equities outperformed those in developed markets by 293 percent from 1999 to 2009, they have significantly underperformed — by 36 percent — since 2010 (see chart 1). The volatility in key debt markets this summer, prompted by the hint that the U.S. Federal Reserve Board would taper its bond purchases, has caused additional concern about the sustainability of these markets and economies.

Source: MSCI Emerging Markets US$ Total Return and MSCI World US$ Total Return used as benchmarks for this calculation.

During the past 25 years, major crises — India in 1991, Mexico in 1994 and Russia and Southeast Asia in 1998 — have kick-started economic reform. Improvements in fiscal management, the introduction of productivity-enhancing policies and smarter financial regulation have bolstered long-term, broad-based growth and driven emerging markets forward. Although arguably no emerging market is currently going through a comparable crisis, the significant slowdown in growth is cause enough to push forward much needed reforms. But what are they? To answer that question, we need first to examine factors in emerging-market growth.

Emerging markets have benefited from three major tailwinds that will likely not continue to the same extent going forward.

The first is high, across-the-board commodity prices. The China-driven commodity boom helped drive growth in Latin America, Russia and other commodity exporters after years of stagnation. From 2003 to 2011, energy and metals prices tripled and agricultural prices surged by 50 percent. Major impacts of this development included allowing emerging-markets countries to increase public expenditures, with Russia raising public spending to upwards of $9,000 per person; and leading commodity exporters such as Brazil and Chile to build reserves that dampened volatility and reduced the risk of a future crisis.

The second major tailwind is growth in trade and economic openness. The ascension of China to the World Trade Organization in 2001 was a watershed moment for global trade. Low- and middle-income countries saw their share of global exports more than double, from 21 percent to 43 percent, between 1994 and 2008. During this time China and India had annual growth in exports of 18 percent and 14 percent, respectively. The next important phase of global trade, so-called South-South trade between emerging economies, is set to grow at a rate of more than 18 percent a year, further enhancing the importance of financial openness for these countries.

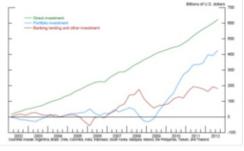

The third tailwind is financial openness and capital flows. From 2002 to 2012, capital flows into emerging economies increased dramatically, with cumulative net inflows to a set of major emerging-markets countries of more than $1.2 trillion. This boost ?was the result of financial liberalization and improved fiscal management in many economies, as well as a global search for yield during a period of persistently low interest rates in the developed world (see chart 2).

Source: Federal Reserve

Recently, many and perhaps all of these three tailwinds have stalled, if not outright reversed. Prices of key commodities, including gold, copper and oil, have stagnated because of slack demand as well as positive supply shocks, particularly in oil. The ratio of trade growth to GDP growth has collapsed from approximately two times to less than one times, similar to the less-open world of a few decades ago. Finally, on the capital flows front, we are seeing the unintended consequences of significant capital flows, such as credit expansion, and now the whispers of capital controls as central banks in emerging markets struggle to control monetary policy with such volatile flows. If capital controls are put back into place, that can even further disrupt markets.

Given the challenges that exist for emerging markets on the policy front, what are the reforms with which investors should be concerned?

First and foremost, emerging-markets economies must start putting into place productivity-enhancing policies to reignite growth — and quickly. This priority is particularly important for two reasons. The first is that the demographic dividend of many large emerging markets has largely run its course, making productivity gains even more important for continued growth in GDP. China’s labor force, for example, will lose 67 million workers during the next 20 years.

Second, commodity exporters cannot rely as much on trade gains from high commodity prices going forward. There are a slew of public policies that emerging markets can undertake to improve productivity, as outlined in a recent International Monetary Fund study on the topic. These include further financial liberalization, removal of agricultural subsidies, reduction of trade tariffs and opening of borders. Investors would be well advised to follow the efficacy, structure and implementation of these programs in detail, as much of the future growth of emerging markets depends on them.

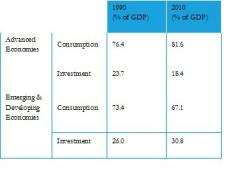

These countries also need to undertake reforms to promote domestic rebalancing. By and large, emerging markets have been following an investment-led approach toward growth. Developed economies have been pursuing a consumption-led model, which cannot continue because of high levels of indebtedness and an impending long deleveraging process. Managing this transition will be very important for emerging economies, which will need to improve the environment and incentives for higher consumption-led growth while still making capital investments (see chart 3).

Source: "The Global Economy's New Path," Zhu Min, Project Syndicate, January 21, 2013

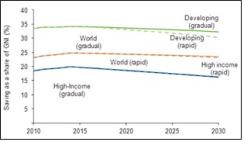

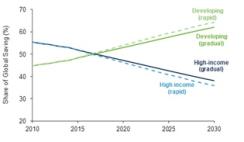

The third and perhaps most important reform issue concerns domestic savings pools. As charts 4 and 5 from a World Bank study indicate, under both “rapid” and “gradual” convergence scenarios between developing and high-income countries, emerging economies have much higher savings rates than developed economies; in 2017 they are forecast to constitute a larger percentage of global savings than developed economies. Currently, a large portion of those savings is in investments such as bank deposits, U.S. Treasuries and property. Once financial markets develop in these economies using these savings, we will see a dampening of emerging-markets volatility, which will be a boon for foreign and domestic investors alike.

Source: World Bank

Source: World Bank

There are recent signs of success, or at least what we at Investec feel are the correct first steps, in policy reform in key emerging markets. The news out of the Chinese plenum in November was positive: President Xi Jinping outlined the framework of a plan to move toward a more market-oriented economy. The policies of Raghuram Rajan, the new governor of the Reserve Bank of India, have put fiscal stability and financial liberalization at the top of the country’s agenda. Each country will have to deal with these challenges and reform agendas within their own contexts. As investors, we need to better incorporate them into our asset allocation models and decisions.

Rahm Emanuel, mayor of Chicago and former chief of staff to President Barack Obama, once said, “You never let a serious crisis go to waste. And what I mean by that it’s an opportunity to do things you think you could not do before.” Officials in major emerging economies would be smart to heed this advice.

Aniket Shah is an investment specialist with the Investec Investment Institute, part of Investec Asset Management.

See Investec's legal disclaimer. Get more on emerging markets.