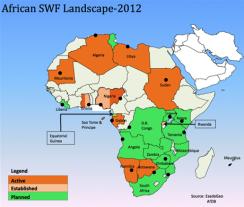

I’ve said it before, but I’ll say it again: In the coming decade, Africa will become the largest sponsor of sovereign wealth funds (SWFs) on the planet. Don’t believe me? Check out this map!

You probably find it a bit odd that the poorest continent in the world would have the highest number of sovereign wealth funds. But this popularity specifically reflects the struggles that African countries have had with their resource revenue management and, moreover, their desire to break free of the ‘resource curse’ and grow. Indeed, the countries above have made the decision to create these special purpose investment vehicles to help them more professionally manage their sovereign assets, and, personally, I think they’re absolutely right to do so. A sovereign wealth fund is an important part of a broad institutional toolkit for resource revenue management.

But here’s the thing with sovereign funds; they aren’t all that easy to set up and operate. In fact, it’s downright hard to run an effective, professional, commercial and independent sovereign fund anywhere ... let alone Africa. And things only get more complicated when a government wants to use the sovereign fund to facilitate and indeed catalyze private investment into local economies and infrastructure assets. But (again) I think it’s worth trying.

When thinking about Africa, it’s important to first recognize that African countries will use SWFs in different ways than Western countries. Whereas the latter are largely concerned with Dutch Disease and intergenerational equity, the former will have significant domestic needs today; these are often capital starved economies. And that means that the African funds need to find ways to deploy some or even most of their capital domestically. After all, what’s the point of taking the wealth out of the ground and sending it off to Europe and North America for decades while the locals suffer? Doesn’t that sound off to you? It does to me, too.

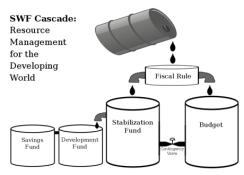

So it’s precisely for this reason that my frequent co-author Adam Dixon and I came up with a policy framework specifically for Africa that advised these governments to set up three types of SWFs over time. We called this the “SWF Cascade” (see photo below).

First, we argued these countries should set up a stabilization fund, which would be useful for smoothing volatile commodity revenues. Indeed, research shows that commodity price volatility is the most damaging factor for developing economies; a stabilization fund would immediately minimize volatility by smoothing resource revenues.

Second, we argued that a ‘development fund’ (if established as a separate entity and operated by professional investment managers that are relatively insulated from government) could help facilitate growth in the local economy and in particular in the efficient construction of infrastructure. A local “for profit” SWF focused on domestic investing in infrastructure could add an important layer of accountability and efficiency to the domestic construction and infrastructure industry. Moreover, it could also be a catalyst for bringing foreign capital into the country by offering foreigners a credible partner with which to co-invest.

Third, only after those two funds were up and running (and lots of capital had also gone through the fiscal rule into the state budget), we advised African countries to set up an inter-generational and international savings fund.

Anyway, that's my thinking on the topic. And you might be wondering why I’m suddenly so interested in Africa’s funds? Well, as it turns out, I’m headed to Africa next week to meet with a bunch of the new and existing sovereign funds at an Institutional Investor event in Cape Town. And we’ll be talking through many of the above topics and themes. So, if you’re going, come say hello!