If there were any remaining questions about the returns generated by the private equity buyout industry, a new paper by Chris Higson of the London Business School and Rüdiger Stucke of the University of Oxford will put them to bed. They argue, in “The Performance of Private Equity”, that buyout funds have, over the pat 30 years, performed unequivocally better than public equity markets. Here’s a blurb:

“We show that U.S. buyout funds with vintage years from 1980 to 2008 have outperformed the S&P 500 by over 500 basis points per annum (as of June 2010).”

That’s a lot! And why does this asset class outperform? The authors have a nice explanation:

“Private equity firms are highly selective in their acquisitions and seek to cherry pick targets that have significant value creation potential. They tend to focus on industries within their expertise. They do extensive due diligence and arrive with a clear strategic plan that they execute urgently, motivating senior management with a large stick and a large carrot. They recoup invested equity as quickly as possible and use financial leverage to amplify the return on invested equity. Given the intensity of this process, it would be truly surprising if private equity investors did not generate positive gross returns.”

Clearly, then, private equity is where it’s at! So, investors, get out there and fill your boots up! Right? Wait, what’s that you say? There’s a catch?

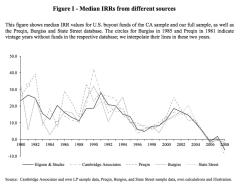

“However we find a significant downward trend in absolute returns over all 29 vintage years. There is also a considerable cross sectional variation in the performance of funds. Just over 60% of funds earn a positive IRR spread against the S&P 500, and the average fund did much better than the median, suggesting that excess returns are mainly driven by positive outliers.”

Let me translate “excess returns are mainly driven by positive outliers” for you. What the authors are saying is that top quartile managers really deliver for their LPs...while everybody else sort of muddles along, collecting their 200 bps in management fees for providing public market returns.

And there’s the problem: Private equity funds are fantastic...if you can get in the right ones. Good luck!