Passive investments are often misunderstood; instead of providing static positioning, as the label would imply, market and sector turbulence makes them prone to fluctuation. To tame a passive asset, we think investors need to exert more active control over the dynamics of volatility.

Sound confusing? Not really. Think of it this way: volatility determines much of the risk profile of any asset. So when market volatility fluctuates, the risk of a passive investment in the market's index changes.

For example, if you invested $100 in the MSCI world index earlier this year, when volatility was hovering near 11 percent, you risked losing $11. Yet just more than a year earlier, when volatility was hovering around 25 percent, the same $100 in the same index put $25 at risk. With this in mind, isn't it a misnomer to describe a fund with such variable risk as a passive investment?

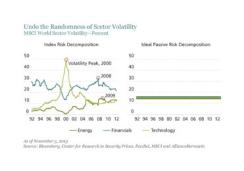

Our colleagues at AllianceBernstein have written extensively on the concentration risks of investing in a benchmark. For example, in 2000, the technology sector ballooned to nearly 30 percent of the S&P 500 index, leaving investors exposed to excessive risk when the crash occurred. Less attention, however, is typically paid to the volatility risks of erratic sector behavior.

About the same time that indexes were getting bloated with technology stocks, the risk of being in that sector shot up fourfold, accounting for 50 percent of the total risk on the index. When oil prices flare up amid tensions in the Middle East, the volatility of the energy sector typically rises as well. And of course, during the global financial crisis, the financial sector accounted for more than 30 percent of the total volatility in the MSCI world index.

In other words, you may have ditched your active manager to invest in a market-cap-weighted global equity index, but instead you let the world actively manage your money. Conventional wisdom that passively managed buy-and-hold portfolios (such as many market-cap benchmarks) yield passive investments tells an incomplete story. Passive management of an investment portfolio in a dynamic world results in active and variable risk-taking.

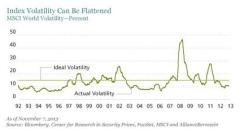

Is there a way to create a portfolio that delivers truly passive risk? We think so. The trick is to take a dynamic approach that aims to undo the randomness of volatility. An ideal passive benchmark would flatten the waves into a fixed, straight line. The flat lines reflect equal passive nonvarying risk-taking in each sector. So if there are seven sectors in the benchmark, a flat line at about 15 percent would yield equal risk for each sector.

When such a strategy is applied, lessened volatility can be achieved. At the index level, the idea is to limit risk exposure to equities when overall index volatility rises.

For example, when chairman Ben Bernanke started talking about tapering the Federal Reserve Board's asset purchase program in May, the average volatility of the S&P 500 jumped from 12 percent to 20 percent. In other words, stocks became nearly twice as risky as they were before, so a $100 investment in the S&P 500 was risking $20 instead of $12. To maintain the initial risk profile, the prudent response would have been to get rid of the additional risk by moving $40 — nearly half of the total — out of the index and into cash. That way, even though index volatility had nearly doubled, an investor would not have taken on any more risk. By doing this, the varying risk of an index can be flattened to a desired constant in expectations.

The same exercise can be done at the sector level. When a sector's volatility spikes, shift some of the exposure into other sectors and/or cash. Thus you can maintain a static risk profile even when one sector or another suddenly becomes more precarious.

This approach may sound complex, but the good news is that it can be achieved at a reasonable incremental cost: slightly more expensive than a purely passive approach yet much cheaper than an actively managed portfolio. We think that's a small price to pay to keep volatility from spoiling your passive portfolio.

Ashwin Alankar and Michael DePalma are co-chief investment officers of tail-risk parity services at AllianceBernstein. Guoan Du is a quantitative analyst at AllianceBernstein.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AllianceBernstein portfolio-management teams.

Read more about equities.