The market convulsions of the past few weeks have many investors thinking twice about owning stocks. There’s a way to stay the course in equities without abandoning comfort zones, however: Consider strategies with built-in shock absorbers.

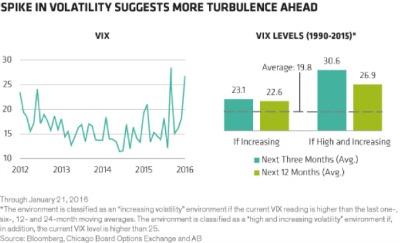

Markets have been growing more unruly since last fall (see chart 1, left). Interlocking issues surrounding the collapse in oil prices, slowing growth in China and shifting U.S. monetary policy have raised doubts about the vitality of the global economy and rattled nerves. And spikes in volatility tend to presage future turbulence (see chart 1, right). Four months later, and the ride continues to be rocky.

Investors may be tempted to rush for the exits. But history teaches that such responses — and, indeed, most efforts at market timing — have proved costly. Investors risk locking in losses and missing out on the market’s eventual recovery.

In our view at AllianceBernstein, current conditions appear to be consistent with a transient midcycle correction, rather than a prolonged recession or credit crisis that will lead to an extended bear market, as in 2008. We are unconvinced that China’s transition and the disruptions in the energy market will significantly erode global economic conditions. The U.S. consumer appears strong, job growth is accelerating, and conditions in Europe and Japan look steady, if uninspiring. So whereas we expect higher volatility to persist, we don’t think it’s time to reduce exposure to equities.

Many equity investors tackle the risk issue by defaulting to traditional passive cap-weighted, index-tracking strategies and ETFs. Yet whereas passive approaches may address concerns about relative risk, they can’t help investors mitigate absolute risk when markets decline.

An allocation to a less-volatile portfolio of stocks can help investors get the long-term upside potential of equities with less of the nasty side effects of gyrating markets along the way. Granted, purely passive approaches are not wholly without risk. Most passive strategies screen strictly for low beta, with no consideration of valuation or potential for return. This characteristic can leave investors overly exposed to pricier subsets of stocks, industries or countries.

These types of strategies are particularly risky, in our view. After multiyear outperformance, for example, low-beta stocks are trading at some of their highest valuations of the past 25 years (see chart 2, right). Some would say the MSCI World Minimum Volatility index, the most commonly used proxy for low-beta stocks, has become the “safety at any price” benchmark. It currently trades at a 32 percent premium to the MSCI World index based on 12-month forward earnings and a 26 percent premium based on free cash flow.

The index is also concentrated in many so-called bond proxy sectors, such as utilities, which adds unintended interest rate sensitivity. And going with the passive flow could mean forgoing any potential for future upside in returns when investors need it most — an era in which broad market performance is likely to be more subdued.

Low-volatility equities come in many shapes and sizes. Notably, many cash-generative companies with good business models are still trading at reasonable valuations (see chart 2, left), and that is precisely why we believe a multifaceted, active approach is the way to go when investing in this space.

An active strategy can adjust exposures depending on insights into current fundamental attractiveness and risk, even pivoting into sectors not typically associated with low volatility. For instance, we’ve found desirable opportunities in software companies with large installed bases and low capital needs. Within health care, even after the strong biotech-led outperformance last year, there are many large, diversified pharmaceuticals companies with strong and stable cash flows that are still selling at discounts to the market.

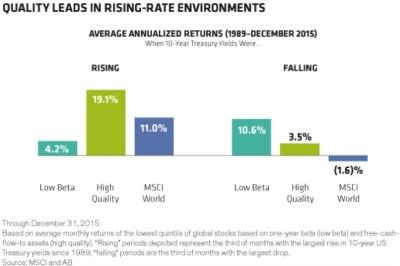

Our research suggests that combining built-in downside defenses with traits of high quality of fundamentals — such as high return on assets, strong cash generation and disciplined balance-sheet management — can produce better risk-adjusted returns than focusing on low volatility alone. That’s because these two attributes offer complementary, tag-teaming features. High-quality stocks provide participation in bull markets, including during periods of rising interest rates (see chart 3), whereas low-beta portfolios are much better at tempering losses in market slumps.

The equity market’s recent schizophrenia has been unnerving. It also comes with the territory. By actively trading off between quality and stability and remaining sensitive to valuation, it is possible to build a portfolio that can weather future bouts of volatility through a variety of environments. Given where we are in the investment and rate cycle, that’s particularly important. A smoother journey that’s easier on the nerves can help keep equity investors on course when turbulence strikes and improve their odds of getting to their desired investment destination.

Kent Hargis is portfolio manager, strategic core equities; Chris Marx is portfolio manager, equities; and Sammy Suzuki is portfolio manager, strategic core equities; all at AllianceBernstein in New York.

See AB’s disclaimer.

Get more on equities.