By Debbie Carlson

AT A GLANCE

- Retail beef prices hit a record in July, as base demand across all grades, from prime to select, remained “incredibly good”

- Trading volume in Feeder Cattle and Live Cattle futures and options set records in 2023 as processors and others managed price risk

Cattle supplies are tight and are likely to stay that way for the next few years as drought and high input prices will limit herd expansion.

A smaller herd comes at a time when beef demand remains strong, and that is driving cattle prices higher. Since bottoming during the depths of the COVID-19 pandemic in spring 2020 at $81.45 per hundredweight (cwt), front-month live cattle futures prices have more than doubled, trading around $185 in fall of 2023. Feeder Cattle futures have seen a similar jump in values over that time. Given the biological nature of raising cattle, it will take a few years for inventories to bottom and herd expansion to begin, completing the cattle cycle.

“The earliest opportunity for any increase in production would be in late 2026, and in all likelihood, 2027,” says Don Close, chief research and analytics officer for Terrain Ag.

In January, the U.S. Department of Agriculture estimated U.S. cattle inventory at its smallest level in eight years, at 89.3 million head. Beef cow supplies are at the lowest level since 1962, at 28.9 million head.

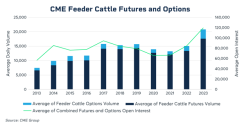

The tight market conditions have shown up in cattle futures and options trading in 2023 as producers and others manage their price risk. Average daily trading volume in Feeder Cattle futures and options reached a combined record of 20,865 contracts per day. Open interest – the number of unsettled contracts – also reached a combined 120,046 record. Live Cattle futures and options also saw record trading at a combined 83,347 contracts per day.

Drought, High Costs Limiting Expansion

David Weaber, beef analyst at Terrain Ag, says drought drives cow slaughter and limits herd expansion. Feed costs have been high as CBOT corn and soybean prices were elevated for much of the year. Pasture and range conditions remain lackluster, so ranchers are supplementing with hay, adding to expenses.The jump in interest rates after the Federal Reserve’s rate-tightening cycle has also prevented expansion, he says, as the interest costs to finance and buy cattle have doubled. “That’s another $100, $125, a head of revenue that you have to make up for,” he says.

Some of this uncertainty is leading to heightened volatility in the cattle market, where both Live Cattle and Feeder Cattle options trades were showing volatility ramping up in mid-November, according to the CME Group Volatility Index (CVOL).

Troy Sander, chair of the National Cattlemen’s Beef Association and chief operations manager for Heritage Beef, says the current high cattle prices give some leverage to the cattle feeder and away from the meat packer.

“That’s obviously a good thing for the cattle feeder, and it was time for the producer to actually see some profits because they were going through a period of pretty small margins,” Sander says.

Despite the challenges cattlemen face with higher costs and loftier interest rates, margins are improving and could stay positive for a while. “There is a lot of optimism in the cattle-feeding industry right now,” Sander says.

Heifer retention will be key to strong cattle-feeder margins. Cow-calf operators are still selling heifers into the feeding system, Sander says. Citing data from CattleFax, auction receipts show heifer sales even with 2022, but video sales show heifers make up a higher percentage of sales in 2023 versus 2022. As long as that trend continues, he expects margins to stay high.

“I don't think we'll see as high margins in the future compared to what we're seeing today, but I think they will still be positive for the foreseeable future,” he says.

Close says the market is structured for cow-calf producers to do well into 2024. The limited cattle supply is challenging others in the industry, such as the cattle backgrounder and feedlot operators, but they are “rolling with the flow,” he says, adding that the processor is feeling the biggest squeeze on margins.

Memories of 2014-15

The sources say the current supply and demand situation reminds cattlemen of 2014, when prices rose to the mid-$160 levels. At that time, producers embarked on an expansion, but prices soon dropped and stayed at lower levels for several years. However, today is a different situation.

This year’s drought is more severe than the 2014 drought and interest rates at the time were lower, as were feeder cattle prices. Those factors should limit aggressive expansion, Sander says.

“The cost of doing business today is probably going to slow down expansion, more so than it did in 2014 and 2015,” he says.

Retail Prices Hold Firm

High live cattle prices translate to higher beef cuts at the meat counter, and Weaber says retail beef prices hit a record in July, with a slight retreat in August. Costly cuts didn’t dissuade shoppers, though. Base demand across all the grades, from prime to select, show that demand is “incredibly good,” Close says.

However, Close notes Terrain Ag is starting to see evidence that consumers are trading down on cuts, opting for a branded product – a beef program certified by the USDA – versus a prime steak, or choosing choice versus a branded product. Thick-meat prices for cuts such as chucks and rounds are holding up better than some of the rib and loin cuts. Part of that might be seasonal, as cooler weather in the northern part of the U.S. may encourage consumers there to buy roasts. Still, Close says, the trend is worth watching.

“We’re seeing some signs that suggest the consumer is saying, ‘OK, we’re going to be more cautious,’” he says.

That said, Weaber says grocery stores are promoting higher-end beef cuts in their weekly advertisements. “We've seen some pretty attractive beef ads over the last month or two that look like retailers are still interested in chasing premium consumers’ dollars.”

Some consumers may be trading down in beef quality, but they’re not trading out, Weaber adds. Pork demand languished most of this year, and chicken demand fell in August.

High Prices, Dollar Strength Ding Export Markets

U.S. beef exports picked up over the last several years, but that pace may be challenged as prices are high and the U.S. dollar remains strong. Weaber says compared to last year, beef exports by tonnage are down nearly 14% year-to-date as of the start of fall.

Australia offers stiff competition to the U.S., which was aggressively building herd numbers and the U.S. herd contracted, Close says. The cards might be in the island nation’s favor as well. Australia is entering a drought and they have an oversupply of cattle which is weighing on the country’s flat price, and it’s likely Aussie cattlemen may liquidate herds, which will bring more beef to market in the short term.

A bright spot for U.S. exporters is Mexico, as beef demand from there is growing year-over-year brought on by demographic changes such as higher incomes and urbanization, Close says. The economic and competitive advantages the U.S. has with its southern neighbor also helps.

“Even though they’re a very solid producer of cattle and beef, we’re a strong supplement to their supply,” Close says.