A debate is taking place among policymakers over whether relatively low inflation levels, as measured by recent consumer price index (CPI) figures, are harmful to the recovery. The peril of outright deflation is fairly well understood by economists, but present levels of disinflation are, in our view, not harmful and may have a positive impact on economic conditions. Indeed, the sources of some of these disinflationary pressures are found in tremendous advances in U.S. energy production and in the expanded use of information technology, both of which are clearly positive factors for economic growth.

In late 2013 the CPI maintained its benign trajectory, with core CPI realizing 1.7 percent year-over-year growth and headline CPI at 1.2 percent. Beyond U.S. borders, euro zone inflation also remained below trend, and U.K. inflation unexpectedly turned down. In Japan inflation is beginning to slowly materialize, with November core CPI, which excludes food and energy, hitting 0.6 percent, and headline CPI reaching 1.5 percent year-over-year, though it still remains low. It is BlackRock’s view that inflation — and its volatility — is likely to remain subdued for some time to come.

During the past several years, the U.S. has witnessed a tremendous level of capital expenditure in the energy sector, contributing to the development of innovative processes and technologies to extract previously unattainable oil and gas reserves from deep shale formations. That dynamic has led to a veritable revolution in U.S. energy production. Since 2005, and after decades of decline, U.S. dry and liquid natural gas production has jumped by 37 percent. Likewise, U.S. crude oil production increased by more than 25 percent during this same period, also after decades of decline.

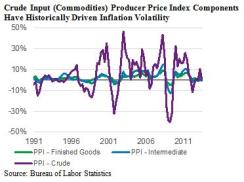

These production gains represent a fascinating opportunity for the U.S., which historically has needed to import a significant amount of oil to meet its energy needs. With greater levels of domestic production coming online, oil imports are likely to continue to slow, which should also help the U.S. trade balance. Moreover, because energy commodities have historically led to fluctuations in inflation, we believe these changes may mean less volatility on this front (see chart 1). That would be a positive development for consumers and businesses alike. With domestic production expected to increase for years, this additional supply should help keep a lid on energy prices, reducing both inflation and political risks in terms of potential supply shocks from abroad.

Advances made in information systems and technology contribute to a second disinflationary force that we believe is having a profound impact not only on the general price level but also on domestic labor markets (a key component of prices). Businesses have made significant capital expenditures in information technology in recent years, resulting in incremental gains in productivity. With greater efficiencies achievable through the latest technologies, which each year deliver greater processing capacity at lower cost, many businesses are finding they are able to save more, invest less and still generate the incremental productive capacity they desire.

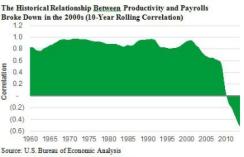

Paradoxically this shift toward technology spending has also weighed on employment, with productivity gains requiring fewer overall employees; it has also suppressed wage growth. That development is a bit confounding because, historically, increased corporate productivity has led to greater hiring levels. That appears to be no longer the case, which we think is in part due to the impact of technology substitution (see chart 2). Of course, all these factors push core inflation rates downward, even as they help generate economic growth.

From a fixed-income investment standpoint, subdued inflation should mitigate macroeconomic headwinds to nominal bond sectors, whereas different parts of the Treasury Inflation-Protected Securities yield curve may occasionally appear attractively valued. Overall, we believe rates are at an early stage of a long climb back to normalized levels, but this process is occurring at a varying pace, depending on what part of the yield curve one is considering. For example, we think the ten-year Treasury is approaching its fair-value range, but central bank policy has continued to distort curve valuations at the short end. This suggests to us that the risk of rate volatility lies close to the front end, whereas back-end rates should be fairly stable, possibly climbing higher as the year unfolds, and should perform reasonably well in the year ahead.

Rick Rieder is chief investment officer of fundamental fixed income for BlackRock.

See BlackRock's legal disclaimer. Get more on fixed income.