After several challenging years, it finally feels like a great time to be a value investor again. Market conditions have become much more conducive to finding undervalued, controversial stocks with long-term payoff potential. Even after this year’s equity market rally, we think the rebound in value is just beginning.

The 2008–’09 financial crisis delivered a huge shock to investor behavior. Fears of global economic collapse dominated market sentiment. Extraordinary volatility prompted investors to flee from risky stocks toward safe assets. Little attention was paid to company fundamentals, so correlations spiked as stocks generally traded in the same direction. It was a toxic environment for stock pickers like us who focus on deep-value stocks, which over the past few years have often been found at the riskier end of the equity market. (Read more: “How to Prevent a Market Crisis”)

Things are changing. This year global equities have shrugged off geopolitical and macroeconomic threats — from the civil war in Syria to the fiscal standoff in Washington — that would have sent markets into a tailspin in the risk-averse world of just a year or two ago. Meanwhile, stock correlations have fallen much closer to normal levels, indicating that company news is driving markets once again.

This environment means that investors can successfully use research to identify cheap stocks with much better prospects than widely perceived. Value investing relies on investors’ emotions to create opportunities, yet the payoff can only come when investors realize they have overreacted to bad news and reprice a stock accordingly. This behavior typically comes in response to some stock-specific good news, such as a positive earnings announcement. This reaction did not occur in the anxiety-driven market following the financial crisis, but it is happening today.

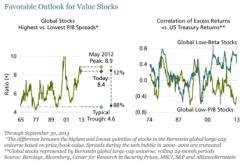

We think the recovery of value stocks is still in its infancy. Our measure of the value opportunity looks at spreads between the cheapest and most expensive quintiles of global stocks based on their price-to-book-value (P/B) ratio. Even after this year’s equity rally, these spreads remain very wide (see chart 1). Spreads probably have not narrowed as much as might have expected because the market dislocations created by the financial crisis were so profound. The lingering distortive effects of the safety trade left defensive, low-risk stocks at near-record premiums to the market and riskier, cyclical stocks at near-record discounts.

In the past, when these spreads narrowed, value stocks outperformed strongly. Yet by the end of September, P/B spreads had narrowed only about 12 percent of the way toward a typical trough, meaning this trend is likely to continue. Our research shows that unlike seemingly safer low-beta stocks, low P/B stocks have low correlations with bond returns, so cheaper stocks should continue to outperform in a rising interest rate environment.

Moreover, these spreads remain wide across sectors. There are attractively valued stocks in many different sectors and a broad diversification of risk exposures. There are plenty of cheap stocks with underappreciated earnings prospects in a variety of industries as disparate as aerospace, high tech and pharmaceuticals.

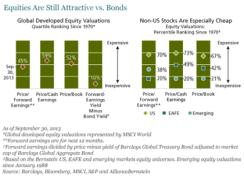

Skeptics might argue that global stocks are no longer as cheap as, say, a couple of years ago. It is indeed true that valuations have largely rebounded to normal levels, as per quartile rankings going back to 1970 (see chart 2). But compared with bonds, equity valuations are still a bargain. And while U.S. equities are indeed trading at relatively high prices, non-U.S. equities remain much cheaper, especially in emerging markets.

Of course, there are still major challenges to take into consideration, from U.S. fiscal issues to instability in the Middle East. One should constantly be on the lookout for potential sources of volatility, a relapse of risk aversion and how such a relapse could affect company-specific outlooks.

Nonetheless, investors seem more willing than they have been for a long time to pay attention to company activities and fundamental earnings drivers. With so many stocks still trading at discounted prices, we think this is the right time to get back into value.

Kevin Simms is chief investment officer of international value equities at AllianceBernstein.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AllianceBernstein portfolio-management teams.

Read more about equities.