Although many observers, including us at PIMCO, have reduced their forecasts for global growth, we remain optimistic on U.S. housing as an asset class that stands to benefit from low interest rates and the steep decline in energy prices. Even in this volatile environment, we expect home prices to continue growing at 3 to 4 percent a year.

The recent bursts in market volatility arose from fears around China’s policies and falling oil prices, though both of these factors are supportive for U.S. housing. Uncertainty in global markets has caused the Federal Reserve to slow its anticipated pace of rate increases and has precipitated further easing in Europe and Japan, driving rates on $10 trillion in government bonds negative. Foreign capital has flowed into the comparatively attractive positive-yielding U.S. market and kept interest rates low.

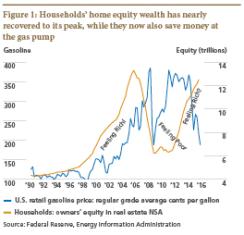

All of this is positive for U.S. housing: Low mortgage rates, combined with positive employment and income growth, are strengthening consumer balance sheets, improving housing affordability and boosting home prices. Gasoline prices are down nearly 50 percent over the past two years, and although certain markets in oil-producing regions are negatively affected, homeowners overall will keep more money in their pockets (see chart 1).

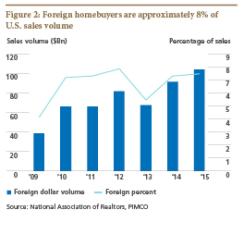

There have been some concerns that slower global growth, notably in China and Brazil, and a stronger U.S. dollar could weaken the housing market by reducing demand from foreign buyers who have been active — at least anecdotally — in recent years in regional markets such as New York, Miami and even here in Orange County, California. Nationwide, however, foreign buyers account for only approximately 8 percent of transaction volume and 4 percent of sales, according to the National Association of Realtors (see chart 2). These data include residents on visas or green cards whose decision to buy a home is independent of the economy in China. Nonresident foreigners, who would more likely be purchasing real estate as an investment, represent only one half of foreign transaction volume.

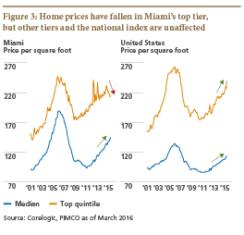

Our analysis shows some weakness at the higher end of the New York and Miami markets. But the middle and lower tiers, which support many housing-related investments, continue to perform well enough that aggregate statistics of home price growth are unaffected (see chart 3).

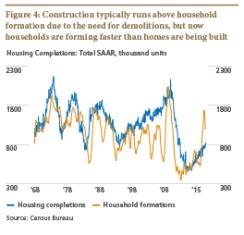

The strongest case for continued appreciation comes down to simple supply and demand. Comparing expected demographics and anticipated household formations with the number of homes being built suggests that we could even face a housing shortage in the near future. Household formations are difficult to measure and forecast. Recent trends suggest about 1.2 million new households are being created each year. This number is expected to rise to 1.5 million annual household formations over the next decade. All the while, although only some 1 million housing units are being completed per year and about 250,000 homes are being demolished, there is a net of 750,000 new homes annually (see chart 4). During the first few years following the 2008–’09 financial crisis, the excess supply from overbuilding and mortgage delinquency provided a buffer while household formations lagged. That excess has now turned into a deficit. Long-term demographic demand trends are very strong. Even indebted Millennials need a place to live. You can’t build houses overnight to meet demand.

The ongoing recovery in housing has important implications for housing-related investment opportunities. In the current environment, many borrowers are credit-constrained and underserved, but potential improvements in their fundamental financial health also have important repercussions for investments in whole loans or public mortgage real estate investment trusts. All of these have come under pressure and now trade at deep discounts to their book values, offering attractive yield potential for investors.

Overall, we at PIMCO believe U.S. housing remains on a firm footing. Whereas we do not expect home prices to appreciate at the same pace as during the years immediately following the late-2000s recession, we believe the price growth trajectory will remain positive and stabilize around 1 percent above the overall rate of core inflation. In times of global economic turbulence, there’s no place like housing.

Daniel Hyman is a managing director and co-head of the agency mortgage portfolio management team, and Emmanuel Sharef is a residential housing analytics specialist; both at PIMCO’s headquarters in Newport Beach, California.

See PIMCO’s disclaimer.

Get more on macro.