Fundraising by infrastructure fund managers is at an all-time high but so is the amount of funds raised that has not been invested. The amount of so-called “dry powder” has been multiplied by three in ten years and now stands at more than $200 billion (USD). While infrastructure investment takes time and is also increasingly popular, this 200% increase in 10 years in the amount of funds committed but not invested points to a particular bottleneck in the unlisted infrastructure sector: hurdle rates.

When closing a fund, the general partners (GPs) agree with their limited partners (LPs) on a hurdle rate, that is, a minimum return above which GPs will receive a share of profits. In effect, hurdle rates are benchmarks that fund managers must beat to be rewarded, and they would typically decide not to invest in projects with expected returns below the fund’s hurdle rate.

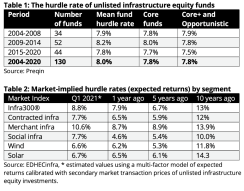

Hurdle rates are stuck in the past

Data shows that the hurdle rate of infrastructure funds have been stuck at 8% for the past 15 years. In effect, there is no difference between the hurdle rates of so-called “core” funds, which are supposed to be investing at the lower end of the risk spectrum, and the “core+” and “opportunistic” funds that invest in risker, presumably higher return assets (table 1). Thus, despite considerable changes in market conditions, including significant yield compression, hurdle rates remain set in a completely ad hoc manner, without any relation to fair market prices.

Conversely, looking at gross mark-to-market expected returns (table 2) suggests that yields have indeed compressed over time, but also that different styles of infrastructure investing call for different levels of expected returns. This data also shows that risks are properly priced in markets, yet they are not reflected in fund hurdle rates.

Indeed, with an 8% hurdle, equity investments like renewables energy projects are virtually impossible. But as the data shows, most funds continue to reproduce the same model. This situation creates misaligned incentives and unnecessary costs.

High hurdle rates means higher risk

Faced with decreasing yield and stuck with a relatively high hurdle rate requested by investors badly informed on the actual market yield of infrastructure assets, fund managers have no other choice but to take more risk and add more fund leverage or stray from their original mandate to invest in infrastructure. In the end, these risks are passed back to LPs who are invested in vehicles that may not have the risk-return profile they intended.The intuition that a high hurdle rate is in the interest of investors in infrastructure funds does not correspond to reality or create virtuous incentives for asset managers to manage the risks of their investments.

High hurdle rates also cost LPs entering funds at second or third close who must pay equalization interests , which are calculated on the basis of hurdle rates instead of mark-to-market returns.

Dry powder is very costly

Finally, the opportunity cost of all this dry powder is enormous. Had even half of the infrastructure dry powder been invested in the infra300 index, which tracks the global unlisted infrastructure equity market, during the past 10 years, LPs and GPs would have been able to share approximately $100 billion (USD) of extra payouts. That’s at least 20% more than all distributions made by infrastructure funds over that period. Instead, the accumulated commitments have yielded very little.It is clear that by ignoring the expected yield implied by current market prices, investors in infrastructure funds are doing themselves a great disservice.