In a rare embrace of modernity for deeply conservative Saudi Arabia — which faced violent clashes after the introduction of television 50 years ago and still doesn’t allow women to drive — Deputy Crown Prince Mohammed bin Salman revealed last summer that the kingdom’s future will be digital. Prince Mohammed, the brash young face of the House of Saud and chair of the country’s Council of Economic and Development Affairs, boarded a private jet to California in June to mingle with Silicon Valley whiz kids and the venture capital gods who can make or break them. Swapping his traditional thobe for a pair of blue jeans and a blazer, the grinning 31-year-old posed with Mark Zuckerberg for a photo shoot at Facebook’s headquarters in Menlo Park. Just a few weeks earlier, Saudi Arabia’s Public Investment Fund had broken the record for the all-time biggest single investment in a venture-backed company when it cut a $3.5 billion check to Uber Technologies.

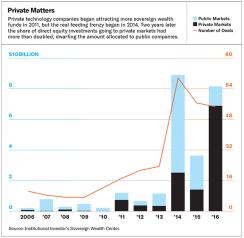

PIF may be one of the most aggressive state-owned investors in tech these days, but it’s not alone. A number of sovereign wealth funds, their portfolios hobbled by years of heavy investment in low-yielding bonds, have been plowing billions into new technologies and start-ups, hoping to bag the next Facebook. According to data from Institutional Investor’s Sovereign Wealth Center, these government-owned investment funds poured nearly $7 billion into private technology companies in 2016, shattering their previous record of $2.5 billion, set in 2014. But the Uber investment raises the question of whether PIF — and investors like it — are in over their heads.

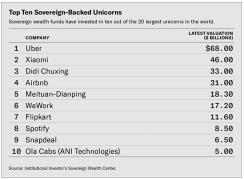

Saudi cash took the unicorn club (venture-backed private companies valued at more than $1 billion) to new heights when Uber’s valuation topped $68 billion last June. But shortly after that news broke, the San Francisco–based taxi app rode into a maelstrom of controversies: CEO Travis Kalanick got caught berating an Uber driver in a viral video, hundreds of thousands of users staged a boycott over Kalanick’s support of President Donald Trump, a former employee published an account of sexual harassment, and the company continues to face an exodus from key management positions.

Uber’s troubles are a bad omen for a market that pundits and soothsayers have been calling a bubble. The number of venture-backed companies worth $1 billion or more soared from 45 in January 2014 to 154 as of December 2016, according to data from the Wall Street Journal. As unicorns multiplied at a speed that would put rabbits to shame, sovereign wealth funds, which collectively manage about $6.5 trillion, emerged as a promising source of long-term private capital. But some experts question whether the funds have the technical know-how to avoid getting burned in today’s frothy technology markets.

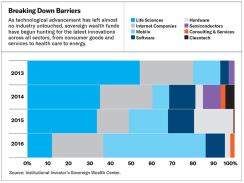

Long considered a trailblazer and role model in the sovereign community for both its prudent approach to direct investing and its tech savvy, Singapore’s sovereign wealth fund GIC, which holds about $354 billion, according to Sovereign Wealth Center estimates, decided years ago to devote special attention to the risks and opportunities arising from the breakneck speed of technological adoption and innovation across all sectors, from health care to energy to manufacturing.

“It’s increasingly hard to categorize which are technology companies and which are not,” says Lim Chow Kiat, GIC’s chief executive and group chief investment officer. “To the extent the traditional definition of ‘technology sector’ is still relevant, we look at it as comprising the entire chain, from start-ups to established industry giants. There are strong linkages amongst the firms at various stages, but the key is not in top-down allocation but bottom-up, name-by-name selection.”

Over the past decade state-owned investors have pumped $25.7 billion into direct technology equity investments, with more than 80 percent of that total coming in since the start of 2014. GIC and its sister institution, Temasek Holdings, accounted for about two thirds of those investments, committing $7 billion and $10.2 billion, respectively, since 2006.

Though publicly listed tech companies typically have received the lion’s share of sovereign dollars, last year marked a significant turnabout, with private market investments accounting for more than 84 percent of the total. Sovereign funds have been known to err on the side of risk aversion, but lately these institutions have been allocating more to high-risk start-ups and later-stage growth companies, popping up as anchor investors in pre-IPO funding rounds — sometimes even taking the lead. Robert Nelsen, co-founder of ARCH Venture Partners, actively tries to recruit sovereign wealth funds into earlier rounds because they’re prone to buy and hold up to and through an IPO.

“Instead of thinking about how to sell after the IPO, they’re thinking about how to buy more,” says Nelsen, who specializes in biotechnology. The life sciences segment, including biotechnologies and medical devices, attracted 11.5 percent of sovereign funds’ direct technology spending in 2016. Mobile companies received a little over half thanks to Saudi Arabia’s investment in Uber, which accounted for 43 percent of the total. Otherwise, Internet companies would have taken the lead, with nearly $2 billion deployed in 13 investments. The remaining $1.1 billion was divided among software, hardware, and consulting companies. About $200 million went to online and mobile financial technology companies.

Biotech has been a natural fit for large sovereign wealth funds because the lab work involved typically requires a larger amount of capital up front than start-ups in other industries need. Because these institutions manage tens of billions of dollars, Nelsen says, they usually won’t even consider an investment opportunity of less than $50 million. “If you’re a sovereign wealth fund, a $10 million check is immaterial,” he says. “It has to be a reasonable amount of capital that can reasonably be put to work in a company to have an impact.”

The challenge of investing at scale is one of the biggest reasons some sovereigns are eschewing venture capital funds in favor of direct investing. Venture capital as an asset class is tightly constrained by the size and number of start-up companies available. Moreover, many of the top-performing venture firms stopped taking on new limited partners years ago. When Bessemer Venture Partners was raising its most recent, $1.6 billion, fund in 2015, partner Ed Colloton says, there was no need to market the fund beyond the firm’s existing investors, which are mostly foundations, university endowments, and family offices. “You’re not going to raise a bigger fund, so everybody just comes back to the table and reups for the new one,” he says.

Taking matters into its own hands, Saudi Arabia’s PIF announced in October that it would put a stunning $45 billion toward the creation of a technology fund run by Japanese telecommunications giant SoftBank Group Corp. Despite the kingdom’s vast oil wealth, that’s not exactly pennies for PIF. Originally created as a development fund to divert a portion of Saudi Arabia’s oil money into strategically important industries and projects, the fund managed $157 billion in assets as of June 2016, mostly in domestic stocks and loans to local businesses.

The fund, which started in 1971 but until recently had little or no international visibility, emerged as the linchpin in Prince Mohammed’s economic reform agenda to wean the country off its dependence on hydrocarbons. Under new leadership PIF reengineered itself before taking the international stage in a full-blown tech offensive. It has since received a $27 billion transfer from the kingdom’s central bank, the Saudi Arabian Monetary Agency, as well as the kingdom’s ownership stake in the world’s biggest oil producer, Saudi Arabian Oil Co. Saudi officials insist the latter could be worth as much as $2 trillion, but that’s all tied up until the company’s planned IPO — if and when that happens.

In November, PIF dumped half a billion dollars on Noon, an online shopping website under development in Dubai that aspires to be the Amazon.com of the Middle East.

But in a not too shocking twist, it turns out Amazon also aspires to be the Amazon of the Middle East: The U.S. e-commerce behemoth reached an agreement to acquire Souq.com, an established online marketplace operated out of Dubai, for more than $650 million in March. The development underscores just how unpredictable and cutthroat the tech business can be — and just how bold Saudi Arabia’s PIF is for throwing a quarter of its current assets behind the imperfect science of technological disruption. “Historically, it’s always been hard to judge which companies are going to make money,” warns Colloton, who chairs the investment committee at Bessemer, a top-performing venture firm. “This business is not for the faint of heart.”

For anyone keeping tabs on sovereign wealth funds, Saudi’s investment in Uber felt like déjà vu. Two years before PIF arrived on the scene, the Qatar Investment Authority, which manages $338 billion by Sovereign Wealth Center estimates, raised eyebrows when it wrote a nine-digit check to Uber in 2014, for a $40 billion valuation. Founded in 2005, QIA had a reputation for hoarding glamorous hotels and luxury brands but relatively little experience identifying innovations outside its high-end comfort zone.

The Qatari sovereign fund announced in March that it will open a Silicon Valley office later this year. According to the Sovereign Wealth Center’s transaction database, QIA made its first independent foray into the tech sector in 2011, directly taking minority stakes in U.S. e-commerce start-up Coupons.com and French chip maker Altis Semiconductor SNC, for an estimated total of $50 million. That may only represent a basis point of the fund’s total portfolio, but neither company appears to be the next big thing: Altis was sold during insolvency proceedings last year, and Coupons.com’s share price has collapsed by 65 percent since its 2014 IPO.

In April the $23.5 billion New Zealand Superannuation Fund (NZSF) revealed that its investment in cleantech start-up Ogin had gone bust; the company is now being wound down. The Kiwi sovereign fund invested $30 million in the Massachusetts wind turbine developer in 2013, a deal sourced through a little-known sovereign wealth fund coalition dubbed the Innovation Alliance. Hoping to pool skills and resources to better uncover, research, and invest in venture capital–style deals, New Zealand established the partnership in 2012 with the Abu Dhabi Investment Authority (ADIA), which manages some $600 billion for the emirate by Sovereign Wealth Center estimates, and Alberta Investment Management Corp., which oversees $70 billion-plus in public funds for the Canadian province, including the $14 billion Alberta Heritage Savings Trust Fund. The trio had mostly stayed out of the public eye before NZSF announced it had written down its investment in Ogin. AIMCo had also invested in the company; ADIA had passed.

“Commercially, this has not been a successful investment for the NZ Super Fund, and we are disappointed with the outcome,” chief investment officer Matt Whineray said in a statement. “We went into this investment knowing that the company was early-stage. We accepted that because of the earlier-stage investment there were a broader range of possible outcomes associated with the potential for high returns.”

In Silicon Valley, where companies that have yet to turn a profit receive mind-boggling valuations, it’s even harder for investors to know whether they’re getting a raw deal. And sovereign funds aren’t the only new kids in town. In the past few years, mutual funds, hedge funds, pensions, and endowments have flocked to private tech companies in hopes of juicing their performance. Yet top entrepreneurs tend to gravitate toward established firms with legendary venture capitalists. “It’s against all odds to try to build a great company,” says Bessemer’s Colloton. “If you’re an entrepreneur, you want people in your boardroom who have experience in a particular area and understand the challenges and pitfalls out there.”

A common approach for large asset owners that want a little more bang for their buck is to partner with venture capital or private equity firms through co-investment opportunities, but building trust and credibility in this insular community is no walk in Menlo Park. Even funds like GIC, with hundreds of billions in the bank, have deemed it necessary to set up shop halfway around the world in Silicon Valley. Malaysia’s Khazanah Nasional opened an office there in 2013, and Singapore’s $180 billion state-owned investor Temasek opened a San Francisco office in February.

“While our investments are largely anchored in Asia, we recognize North America as a geography that offers good investment opportunities, particularly in the areas of technology, health care and life sciences,” a spokesman for Temasek tells Institutional Investor. In January the firm bought an $800 million minority stake in Mountain View–based medical technology company Verily Life Sciences (formerly Google Life Sciences) from parent company Alphabet. “The setting up of our San Francisco office brings us closer to these opportunities and complements our existing team in New York, thereby increasing our coverage and connectivity across the U.S.,” the spokesman adds.

Russia has taken a similar approach. RUSNANO Corp., an investment company established by the Russian government in 2011, opened an office around the corner from Stanford University that same year. Its mission: “to develop the Russian nanotechnology industry through co-investment in nanotechnology projects with substantial economic potential or social benefit.”

Although sovereign funds represent the financial interests of foreign governments, these notoriously passive shareholders typically don’t have a political agenda unless they’ve been given an explicit policy objective, usually in the form of economic development goals. “I think the larger, more global SWFs are mostly about financial gain, and I’ve seen little on the strategic side,” says Steve McLaughlin, founder and CEO of Financial Technology Partners, a San Francisco–based investment bank. “On the other hand, some SWFs, like EDBI in Singapore, have specific mandates to help bring business relationships to Singapore over time.”

EDBI, the investment arm of Singapore’s Economic Development Board, participated in a $105 million funding round, led by Temasek in July, for Sprinklr. Valued at $1.8 billion, the New York–based social media management software developer planned to use the fresh capital to expand into Singapore.

Saudi’s PIF may have led the sovereign community in terms of dollars invested in tech companies in 2016 thanks to its one-off investment in Uber, but Singapore’s state-owned investors participated in the most deals: Temasek invested $1.3 billion in 22 deals, according to Sovereign Wealth Center data, while GIC invested $2.2 billion in 12. Khazanah Nasional rounded out the top three with six direct equity investments totaling $380 million.

In the past decade Temasek has made 143 direct equity investments in tech companies — and cashed in. For example, a well-timed 2011 investment of about $37 million in China’s e-commerce platform Alibaba Group Holding is now worth nine times that amount. So it’s no surprise that in 2016, when Temasek posted losses for the first time since the financial crisis, its solution was to double down on the tech sector. Last year telecommunications, media and technology overtook financials as the largest sector in Temasek’s portfolio, with a weighting of 25 percent. The firm’s roots in the TMT sector date back to 1974, when the government of Singapore established Temasek as a holding company to manage state-owned enterprises, including Singapore Telecommunications.

Alibaba has also proved to be a winning investment for sovereigns including GIC, Khazanah, and China Investment Corp. But like Uber and so many other tech giants, its valuation is hotly disputed. Alibaba’s 2014 IPO was the largest in history, luring tech bears out of hibernation to talk about the perceived market bubble on cable news. Bubble or no bubble, a report published last year by SharesPost, which researches private market investments, estimated that roughly one in three unicorns in the U.S. will experience a drop in its valuation when it goes public or sells out.

That’s exactly what happened to Square. At first blush, it would appear that GIC got burned after it led a $150 million Series E round for the U.S. mobile card reader maker only to see the company’s valuation slashed in half at its IPO a year later. But the Series E–round investors had in place an IPO protection — known as a ratchet — that promised them additional shares if the company’s stock priced below $18.56 a share, for a guaranteed return of 20 percent in the event of an IPO. Moreover, Square’s share price is up 40 percent since the IPO.

All of this makes GIC look downright savvy — hardly an inexperienced, deep-pocketed sovereign recklessly throwing money at the first unicorn it saw. Indeed, some experts say state-owned funds, though late to the venture capital party, have proved to be fairly sophisticated investors. As FT Partners’ McLaughlin sees it, sovereign wealth funds are anything but dumb money. “We’ve got a ton of respect for these firms,” he says. “We find the talent and diligence levels equal to or greater than some of the established funds.”

Ashby Monk, executive director of Stanford’s Global Projects Center (and a columnist for Institutional Investor; see “Avenue of Giants,” page 32), agrees with this assessment but warns that the interests of large institutions aren’t always aligned with those of the general partners at private equity and venture capital firms. “They aren’t dumb,” says Monk, who offers advisory services to sovereign funds entering Silicon Valley. “But they’re stepping out of their comfort zone and trusting their GPs to do right by them, and that’s not always the case.”

That concern may be among the reasons Norway’s $930 billion Government Pension Fund Global, the world’s biggest sovereign wealth fund, has yet to enter the pre-IPO tech fray. Since establishing its rainy-day fund with excess oil revenue in 1996, the Norwegian government has kept private equity and unlisted stocks off-limits. Restricted to an ultraconservative mix of stocks, bonds, and real estate, Norges Bank Investment Management (NBIM), the arm of Norway’s central bank that oversees the fund, has explored innovations in passive investing but has grown discontented with sitting on 1.3 percent of all shares in listed companies around the globe.

These days the fund is in the minority. A poll taken at Institutional Investor’s Sovereign Investor Institute’s Global-West Government Fund Roundtable in London last May found that 60 percent of the funds in attendance were already investing in venture capital. The sample represented a geographically diverse group of investors, with 24 percent coming from institutions with more than $100 billion in assets and an additional 11 percent representing funds with over $50 billion.

“They’re missing out on an entire asset class,” says ARCH’s Nelsen of sovereign funds that don’t invest in private markets. “In a portfolio theory sense, as that asset class grows as a percentage of global wealth, they’re actually accepting more risk because they don’t have a balanced portfolio. And they’re left out of large segments of excess returns as the financial markets change.”

Those potential dangers are not lost on NBIM, which was forced to forgo an offer from Facebook for a pre-IPO investment. The firm’s executives have expressed dismay in the past about the slowdown in new corporate listings and their inability to access innovative and fast-growing companies, like Uber and Airbnb, that are staying private for longer.

“For the first time ever, we have a set of companies that have pushed off going public, and they’re raising capital when the companies are valued at tens of billions of dollars,” says Bessemer’s Colloton. “At any other prior period, those would’ve been public companies.”

In a forthcoming paper in the Hastings Law Journal, Duke University associate law professor Elisabeth de Fontenay explains how booming private markets are sucking the life out of public markets. “No longer the promised land for companies poised to grow, the public stock market is quickly becoming a holding pen for massive, sleepy corporations,” de Fontenay writes.

Historically, the two main incentives for going public have been the ability to raise large amounts of capital and the ability to create liquidity for investors. But as sovereign wealth funds have gotten bolder and regulatory changes have allowed private equity and venture capital firms to get larger, more-innovative companies are putting off the day when they will tap public markets and subject themselves to the pressures of quarterly earnings targets.

“We can provide greater financial support for companies with proven technologies and help them avoid the rush to IPO,” Colm Lanigan, head of principal investments at the Abu Dhabi Investment Authority, told the Sovereign Wealth Center in a 2014 interview.

While creating liquidity is still a plus for private equity and venture capital firms that ultimately need to sell a company or take it public to pay back investors, sovereign wealth funds may have a different endgame entirely.

“For the liquidity piece, sovereign wealth funds are playing a really significant role in the sense that they really don’t need an exit for a long time, and they may not want an exit for a long time,” Duke’s de Fontenay tells II. “From that standpoint, you have something that didn’t used to exist: a huge chunk of equity capital that can stay in place for a long time without requiring an exit.”

Otherwise forced to reconcile low growth prospects in public markets to their boards, even the most conservative asset owners may be pressured into private markets. Norway’s Parliament has said it will consider letting its sovereign fund invest in private equity at the beginning of next year. Even if the fund’s private equity allocation was capped at 5 percent of its total portfolio, as its real estate allocation is, NBIM would have about $47 billion to put to work. Its sheer size would put it on equal footing with buyout heavyweights — Carlyle Group, for example, has $51 billion in assets in its corporate private equity division — but whether this unabashed index-investing enthusiast could hold its own against these rivals is an open question.

On the other hand, averaging real growth of just 3.79 percent a year since inception and short of its 4 percent target, Norway may have more to gain than it does to lose. That may well be what’s driving its peers to dive into private markets.

“I don’t understand this idea that public markets are somehow pure,” says ARCH’s Nelsen. “In the deals we do, our investors know way more about a company and all its gory details than any public investor would ever know.”

Jess Delaney is head of research and data for Institutional Investor’s Sovereign Wealth Center.