Talk about following the herd. Today nearly all global bond portfolios use issuance-weighted indexes as benchmarks. Big, developed bond markets like the U.S., Europe and Japan dominate such indexes. As these cash-strapped countries and regions keep churning out debt, investors buy more of their bonds.

To a small but growing number of money managers, that’s asking for trouble. “No bank would make lending decisions that target the most indebted people,” says Jamie Stuttard, who oversees $600 million as head of international bond portfolio management for Fidelity Investments in London. Fundamentals such as gross domestic product are a better starting point for weighting global bond portfolios, Stuttard contends: “GDP gives you an indication of the tax base and thus revenues that can be used to service that debt.”

With that in mind, Fidelity launched its Global Bond Fund and International Bond Fund in May. The two actively managed funds, which have $100 million in total assets, are benchmarked to GDP-weighted indexes: the Barclays Global Aggregate GDP Weighted Index and the Global Aggregate ex-USD GDP Weighted Index, respectively. They join a clutch of similar portfolios, including the Pimco Global Advantage Strategy Bond Institutional, which was launched in February 2009. It now manages $5.2 billion.

“Traditional notions of risk-free sovereign debt in developed economies and riskier sovereign debt in the emerging world have been turned upside down,” says Michael Faloon, COO of Standish Mellon Asset Management Co. in Boston, a Bank of New York Mellon fixed-income specialist that manages $97.5 billion. Bond portfolios’ exposure to slow-growing, debt-laden countries has surged in recent years. But emerging economies, which have grown faster and built surpluses, scarcely register in issuance-weighted indexes. “We feel the traditional approach is not representative of the opportunity set,” Faloon says.

In May, Standish unveiled an actively managed global bond strategy benchmarked to the new World GDP Index from Barclays. Developed with Standish, the index weighs ten countries and country blocs based on nominal GDP. Within each country and bloc, all government, corporate and securitized bond offerings of $500 million or more are then issuance-weighted to reflect market opportunities.

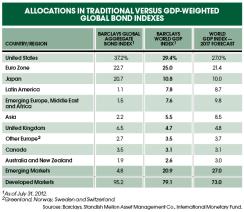

The approach yields substantial differences. The World GDP Index puts Japan’s weighting at 10.8 percent as of July 31, versus 20.7 percent in the Barclays Global Aggregate Bond Index. The U.S. shrinks too, but it’s still the largest component at 29.4 percent, down from 37.2 percent. By contrast, total emerging-markets exposure soars to 20.9 percent, from 4.8 percent in the Global Aggregate index.

Faloon and Fidelity’s Stuttard believe GDP-weighted benchmarks offer more diversification because country allocations are less concentrated. The new benchmarks also provide a better chance of higher risk-adjusted returns, thanks mostly to emerging-markets exposure. Between January 2009 and this August, the volatility of the World GDP Index was slightly higher than the Global Aggregate’s — 6.94 percent versus 6.13 percent, according to Standish — but its annualized return was 7.23 percent compared with 5.92 percent.

GDP-weighted benchmarks are no magic solution, though. Even the soundest emerging-markets economies can suffer extreme short-term volatility and illiquidity, says Brett Cornwell, fixed-income specialist at investment consulting firm Callan Associates in San Francisco. “You’re increasing the risk profile of your benchmark,” he explains.

Also, two of the world’s fastest-growing economies, China and India, don’t appear in standard GDP-weighted indexes because neither country’s debt market is developed enough. And GDP isn’t much use for evaluating corporate bonds, which commonly sit alongside currencies and government paper in global bond portfolios. “There is not one index that solves for all three,” Stuttard says. “You need an active approach.”

Although the Government Pension Fund of Norway adopted a GDP-based approach this year with its global government bond portfolio, many investors aren’t biting yet. “We’ve done a few global manager searches recently, but none have gone with the new GDP approach,” Callan’s Cornwell says. Fidelity and Standish are still waiting for their first institutional commitments to the strategy.