“More for less” is the mantra of the post-credit-crunch world. In these straitened times, firms must deliver extra services for the same or lower fees. Those that provide administration and custody to hedge funds are feeling the pinch, with some smaller administrators charging less simply to survive.

“Fund administrators have moved up the value chain,” says Andrew Collins, London-based head of business development for Europe, the Middle East and Africa with Citigroup’s alternative-investment services division. Having ventured beyond calculating net asset values and providing custody and administration services like shareholder record keeping and independent audit review, they now also perform specialized tasks such as valuation of over-the-counter derivatives, explains Collins, whose firm’s $13.84 trillion in assets under custody make it No. 4 in Institutional Investor’s ranking of the World’s Largest Global Custodians. “This is often for an overall fee similar to before in terms of basis points as a share of assets under management.”

Although hedge funds are reluctant to talk, the average fees they pay administrators have fallen dramatically. “Fees are down from 15 to 18 basis points of assets under management five or so years ago, to a rough maximum of 12 basis points now, with fees negotiated by some of the industry’s largest hedge funds down to as low as single digits,” says Howard Eisen, New York–based managing director for Conifer Group, which provides administration, prime brokerage and trading services to hedge funds. “The same clients who are paying lower fees are also demanding more services for these fees.”

The additional services include data warehousing, which involves the creation of large repositories of information whose uses include complex analysis, Eisen says. He gives examples of questions posed by hedge fund clients that could now be answered much more easily thanks to their administrators: “How much did you lose on the day of the flash crash or during the 2008 credit crisis?”

Robert Mirsky, London-based global head of hedge funds for professional services firm KPMG, attributes lower fees to what he calls a very competitive market. “The margins are really getting tighter,” he says.

Under pressure themselves to reduce fees, hedge funds want their service providers to share the pain. The increasing consolidation of fund administration in the hands of a few big banks with deep pockets makes competition even fiercer by creating vast economies of scale, says Allee Bonnard, audit partner for investment management clients at professional services firm Deloitte’s London office. “The IT costs are huge, but a lot of the costs of fund administration, including much of the IT, are fixed,” Bonnard notes of the banks. “So the more funds they can get, the greater the cost recovery.” This encourages banks to secure as many clients as possible by charging low fees, she adds.

Citi’s Collins says his firm shells out $25 million a year alone on the IT needed to service clients in the alternatives business, in addition to substantial spending by the securities and fund services division as a whole.

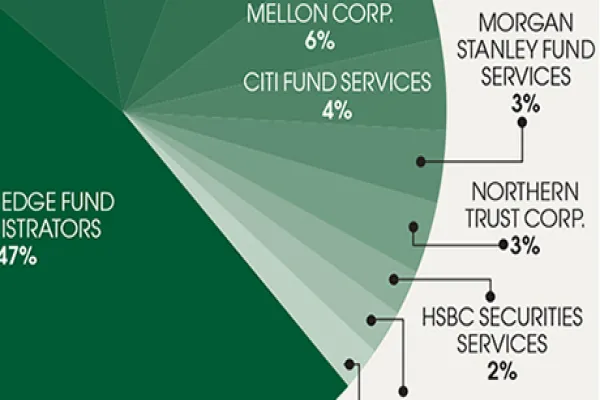

Given these downward pressures, how much lower can fees fall? “I don’t think hedge fund managers select administrators based purely on fees,” says Scott Carpenter, Boston-based senior vice president in alternative-investment solutions at State Street Corp., the world’s biggest hedge fund administrator and the No. 3 custodian, with $18.88 trillion in assets under custody. “The top providers can still receive a quality premium, though it’s narrowing,” Carpenter adds. Some other large custodial banks charge lower fees to break into the market, he says, arguing that such a practice makes it tough to sustain quality.

Deloitte’s Bonnard describes hedge fund administration as “highly commoditized.” In her view most of its services don’t require scarce specialist skills, so competition is mainly on price. Fees could drop even more if big banks start using hedge fund administration as a loss leader to win lucrative prime brokerage services from the same clients, Bonnard predicts. Citi and State Street say they have no such plans.

Administrators have yet to hear the thud of fees falling through the floor, but hedge funds may yet get even more for even less. • •

See more of our research and rankings.