Sovereign wealth funds are nothing more than rainy day funds. And over the past few years, it’s been pouring. Commodity prices are depressed. Budgets are stressed. It should come as no surprise that governments are drawing down on their accumulated sovereign wealth in order to fill deficits. What is perhaps surprising, however, is the speed at which some SWFs are shedding assets.

Russia’s combo of Reserve Fund and National Welfare Fund, which had close to $200 billion in 2014, may be exhausted by 2018. Saudi Arabia took $80 billion from its reserves this year. All this raises an important question: Are we witnessing the end of SWFs as we’ve come to know them?

Nah. I have no doubt we’ll see shifting investment strategies and approaches in the years ahead, but the foundational logic that governments want to manage long-term liabilities and uncertainties via pools of financial wealth is now ingrained. If anything, I expect we’ll see a proliferation of new types of sovereign funds, launched out of novel sources of wealth. I anticipate that governments will creatively convert intangible national endowments into financial capital, thereby monetizing noncore state assets. And the reason I think this is that I’ve seen governments actually doing this over the past few years.

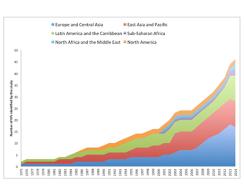

Specifically, I’ve been working on a project about how governments are experimenting with immigrants and even citizenship as an untapped store of sovereign wealth. That’s right: A growing number of governments are thinking about translating the inherent charm and allure of their state into a financial asset that can be used to catalyze economic development. I know that sounds like an off-the-wall concept in the era of Donald Trump, but it’s legit. And, in a new working paper with Alan Gamlen of Victoria University of Wellington and Christopher Kutarna of the University of Oxford, we cite 60 different immigrant investor programs (IIPs) in 57 countries, all of which involve the sale of national membership privileges to foreigners. Considering that as of 1975 there were only three IIPs in the world, this policy tool is disseminating rapidly.

But don’t be fooled. The idea of monetizing citizenship or membership in society is not new. As we show in the paper, the French sold noble titles going back to at least the 16th century. The practice reached a peak under the reign of Louis XIV, when titles were sold to wealthy commoners both to finance wars and to expand the technical capacity of the state. Today, IIPs aren’t all that different. They allow governments to, quite literally, monetize immigration. In a climate of shrinking public budgets, IIPs help governments raise the capital needed to provide the core benefits of citizenship while monetizing that very status.

A back-of-the-envelope calculation would suggest that these programs are unlocking over $35 billion annually for governments globally, and this could quickly grow with the right policies and governance. This is why we think IIPs may become a new form of sovereign wealth, which will inevitably wind up being managed in sovereign wealth funds. In our paper — “Re-Thinking Immigrant Investment Funds” (IIFs)— we document and analyze the rise of the IIPs, situating them within the migration politics as well as sovereign wealth management. Like all SWFs, IIPs and IIFs offer a fascinating overlap of policies and institutions that could easily form the basis of a doctoral thesis project.

And like SWFs, the IIPs and IIFs are not without serious controversy. If you recall 2007–’08, the international community was very worried about the rise of SWFs. Many people wondered if governments could be trusted to use these financial assets constructively. Many people questioned the sources of capital, even doubting aloud whether the subsoil assets in these countries should be converted to financial capital. Others questioned whether currency manipulation and the artificial discounting of domestic labor could be justified by reserve accumulation. Many think citizenship shouldn’t be sold, and that doing so is both intrinsically corrupt and a magnet for bad people and bad money. When you’re reduced to selling off your good name, aren’t you headed for a crash?

There is another hiccup about IIPs beyond the controversy over legitimacy: Most IIPs have been, to be blunt, badly executed. Programs may have been rhetorically rationalized by the objective of raising capital for key sectors or strategies, such as economic transformation or infrastructure renewal, but such statements of intent seldom matched up with any specific fund management strategies or outcomes. Instead, the capital that was given to the government, which was typically absorbed into the general treasury, often lost any distinctive identity or capacity to be harnessed for a specific objective.

We believe our paper offers a way of resolving such difficult issues, drawing on migration policies and tools for managing sovereign wealth to help the 57 governments that currently have IIPs — and those countries that are considering them — get the most from them. As was the case with SWFs generally, good governance practices may be a path to minimize some of the fears and concerns about a type of policy that, let’s be honest, sells citizenship. By our reckoning, IIPs have the best chance of achieving their objectives when they are paired with some form of immigrant investment fund.

An IIF may appear to be an odd or unique investment vehicle, in large part thanks to its unique source of investable assets (via IIPs). But we would simply label IIFs as a new type of sovereign wealth fund — more specifically, a form of sovereign development fund (SDF). In a few cases IIPs do in fact channel revenues into institutional investment vehicles. Malta’s National Development and Social Fund is mandated to “contribute to major projects of national importance,” including initiatives in “education, research, innovation, justice and the rule of law, employment and public health.” British Columbia’s Immigrant Investment Fund (BCIIF) was set up to manage that province’s share of the funds generated by Canada’s former Immigrant Investor Program (which was terminated in 2014). Its mandate was to invest in public infrastructure (to lower the borrowing costs to taxpayers of such projects) and venture capital (to promote jobs and investment), with a smaller share put into recoverable deposits to help ensure the stable financial performance of the fund.

The best IIFs would drive positive development outcomes by leveraging the capitalist system. Drawing lessons from other SDF types, modern IIFs could incubate start-ups led by and for immigrants and even refugees, pursuing commercial objectives as well as facilitating refugee and immigrant integration. IIFs could also stimulate infrastructure growth and other public goods, which would allow the IIF to show the value — unequivocally — of their immigrant investors. In this way IIFs might help flip the anti-immigrant narrative that is dangerously poisoning politics in many countries, including the U.S. As Alan, Chris and I argue, for the establishment of well-designed and -governed immigrant investment funds to separately manage the proceeds of IIPs, as an alternative to scattering them into either the general public purse or the broad economy. It would improve the chances of IIP success — by clarifying objectives and documenting specific outcomes — and would reduce the anxiety over the implicit selling of citizenship . . . a topic that people are probably right to have some anxiety about.

In sum, the current macroeconomic climate may underpin a demise of certain SWFs, but we are most certainly not done with the rise of SWFs generally. I expect IIFs are just the latest in a line of new mechanisms for sovereigns to cultivate and manage their implicit wealth.

Countries with immigrant investor programs, by region, 1975–2015: