Investing with conviction might seem easy when markets are calm and the outlook is clear. As recent volatility reminds us, however, that’s rarely the case. The good news is that investors can prepare by understanding the performance patterns of high-conviction strategies.

High-conviction equity investing can take many forms. It’s much more than just having high active share in a portfolio. So how can investors determine allocations among many strategies with markedly different angles on the market?

The first step is to understand how different equity approaches behave in different environments. Imagine it’s 2009, and you have a big allocation to quality strategies, which delivered a return of 31 percent that year, ranking highest among rival equity categories. But just one year later, quality strategies were at the bottom of the pack, returning a healthy 11.9 percent — but well below other types of equities.

Seasoned investors are familiar with the dilemma: One year’s winner is the next year’s loser. Just as the performance of different asset classes can vary from year to year, the return patterns within high-conviction equities can be capricious, as the quilt display shows. No single strategy is consistently at the top or the bottom. Yet as we’ve shown in a previous post, holding onto skilled portfolios with high-conviction characteristics like these is very effective through full market cycles.

To gain comfort with employing high-conviction equity allocations, it’s important to understand how market conditions can affect their behavior. Both rising and falling markets matter. To find out how much they matter, we looked at the annualized relative return achieved by skilled high-conviction managers in the best third of market returns and the worst third of market returns over the past decade.

When markets were falling, managers who featured low beta, quality and income provided the best downside protection (see chart 1). This makes sense, given the more defensive characteristics of these factors.

When markets were rising, managers with a clear focus on value, momentum and growth provided the best upside capture. This, too, makes sense, because these factors are driven by long-term earnings growth and recovery.

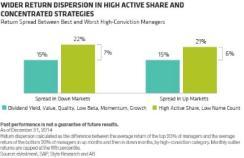

What about strategies with low name count or high active share? On average, these types of portfolios were less sensitive to the surrounding environment and delivered positive alpha in both the best and worst thirds of the market. But there’s a catch. In these portfolios, there was a much wider dispersion of returns when compared with other high-conviction strategies (see chart 2). In other words, by relying only on low name count or high active share as an expression of high conviction, investors may sacrifice consistency.

The wider range of returns among high active share and concentrated portfolios may be a result of the limitations of these groupings as conviction metrics. Neither measure provides any information about a portfolio’s underlying philosophy. As a result, in different market conditions, their performance can be expected to vary. In high-conviction strategies with a clear approach, the narrower dispersion reflects the fact that there’s much more visibility about how these portfolios invest and how they are likely to perform in changing market conditions.

Maintaining conviction isn’t always easy. When markets are falling, conviction managers of all stripes may face pressure to stray from their areas of focus to add protection to a portfolio.

So to invest effectively in changing markets, in our view at AllianceBernstein, it’s essential to have a properly diversified allocation to complementary high-conviction equity strategies that demonstrate an ability to stand firm in stormy markets. And by sticking with exposures to different equity factors over a full market cycle, we believe, there’s a better chance that the strongest years of performance will offset the weaker periods and deliver a much smoother return experience.

Dianne Lob is senior managing director of equities, and Nelson Yu is co-head of equities quantitative research; both at AllianceBernstein in New York.

See AllianceBernstein’s disclaimer.

Get more on equities.