The past year was a challenging one for active investors. There was a bevy of critical uncertainties in the market: The timing of the Federal Reserve’s rate hike, the oil price path and the trajectory of China’s growth and policy were just a few. Some of these uncertainties will persist in 2016. We at BlackRock believe, however, that dispersion in both macroeconomics and asset price returns will create idiosyncratic opportunities for investors willing to move away from traditional market betas and consensus trades. The reason: We think the economic, credit and market cycles are in later stages than many believe — although we do not see a full-fledged U.S. recession this year.

A typical characteristic of late-cycle periods is a divergence between corporate top-line and bottom-line growth, as significant financial engineering takes place. Nominal gross domestic product growth has diverged from what recent corporate earnings reports are telling us. Many corporate balance sheets have added significant leverage, and we are seeing prodigious levels of share buybacks and mergers and acquisitions. These are all signals that we have moved into a late-cycle stage of the recovery.

The economic cycle still looks fairly stable in the U.S., but the profit cycle appears long in the tooth. This divergence has been facilitated by the Fed’s extraordinarily accommodative policy and, further, has important implications for credit markets, particularly when judged alongside a growing list of factors that could cause market dispersion to persistently turn higher. Consider:

•The volatility and dispersion created by the Fed are beginning to normalize interest rates, while the effect of China’s structural slowdown late last year may spill over into 2016.

•Global growth is likely to diverge by country based on whether governments are led by structural reformers, are effectively politically stagnant or are pursuing retrograde policies.

•Companies have perhaps inadvertently made themselves more fragile by pursuing strategies that dramatically lower share counts while simultaneously adding to debt. This means that future earnings per share are likely to be more volatile and vulnerable to either an economic downturn or to low nominal GDP growth.

•New, disruptive technologies are creating a winner-takes-all economy that leads to wider gaps between corporate winners and losers. The winners often run capital- and labor-light business operations, and the losers are burdened by capital- and labor-intensive structures.

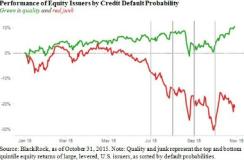

All this has contributed to the recently increased divergence in returns by credit-quality segment. High-quality companies outperformed lower-quality peers, as judged by expected default probabilities, during last year’s late-summer market swoon (see chart 1). It is likely such return dispersions will persist in 2016.

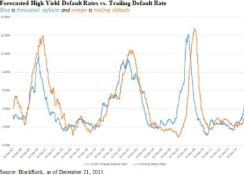

In our view, the signals of late-cycle economic characteristics do not suggest an imminent recession. Rather, they imply that the cycle has peaked and is in the process of turning. The late-cycle turn can last one to two years, in our experience. One indicator that concerns us, however, is the recent rise in our 12-month high-yield default rate forecast. That measure, driven by macroeconomic, corporate-lending cycle and market-derived insights, increased from 3.1 percent to 4.3 percent through the fourth quarter. That is particularly concerning because our default forecast series has a pretty good track record as an early-turn indicator, which has been upheld since its launch in 2007 (see chart 2). By contrast, merely analyzing the widening of credit spreads tends to be both premature and produces a high incidence of false calls.

Does the rise in high-yield implied defaults reflect a broad U.S. slowdown in the next year, which is the usual predictive relationship? Or is it the result of the slump in global industrial production and in the oil and energy sector? We believe the answer is the latter, which clearly has its roots in China’s economic transition and technological and policy-related oversupply that has driven oil prices dramatically lower.

Bottom line: Even if economic growth is unlikely to falter in 2016, the credit cycle may well see more distress in the year ahead. This suggests taking a cautious stance toward high-yield. We think a lower exposure to credit — particularly the lowest-quality segments — and overall caution on the asset class would be prudent for investors who will have to deal with greater return dispersion this year.

Tom Parker is chief investment officer of model-based fixed income, and Garth Flannery is a portfolio manager with the factor-based strategies group; both at BlackRock.

Get more on fixed income.