By Steven A. Sass and Jorge D. Ramos-Mercado

Center for Retirement Research at Boston College, May 2015, Number 15-9 (full text with Appendix available here.)

Introduction

The discussion proceeds as follows. The first section introduces the data and methodology. The second section explores whether the financial assessments of young, middle-age, and older workers primarily reflect the household’s ability to meet day-to-day as opposed to distant financial needs. The second section explores the same issue for workers by income. The final section concludes that Americans at all ages and income levels are shortsighted about their finances and on their own cannot be expected to devote much effort to addressing distant financial problems. Given the significantly expanded reliance on household saving, this finding suggests a need to make it easy and automatic for households of all ages and income levels to save enough to secure a basic level of financial well-being in retirement.

Data and Methodology

This study tests whether the financial self-assessments by workers of different ages and income levels primarily reflect their ability to meet the household’s day-to-day as opposed to distant financial needs. It uses data from the FINRA Investor Education Foundation’s 2012 State-by-State Financial Capability Survey, an online survey of 25,509 American adults. The sample used in this study includes 9,473 households in the labor force ages 25-60 that provide the information needed for the analysis.2

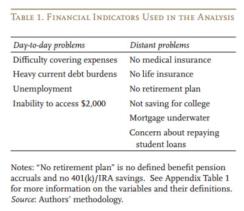

At the beginning of the interview, workers were asked: “Overall, thinking of your assets, debts and savings, how satisfied are you with your current personal financial condition?” The assessments use a 10-point scale, where 1 means “Not At All Satisfied” and 10 means “Extremely Satisfied.” Respondents were then asked a series of questions about a reasonably comprehensive set of their day-to-day and distant financial needs. This study focuses on whether these needs go unmet – for example, if a household is unable to access $2,000 or lacks health insurance – so the needs are referred to as “problems” or “deficiencies.“

To test whether Americans are shortsighted about their finances, this study measures the strength of the relationships between households’ financial satisfaction and their day-to-day or distant financial problems. It measures these relationships by running ordinary least-squares (OLS) regressions estimating the following equation: financial satisfaction = f (day-to-day problems, distant problems, controls).

The regression results thus estimate the reduction in financial satisfaction associated with a particular deficiency relative to the financial satisfaction of workers who do not have that deficiency. Table 1 lists the day-to-day and distant problems included in the analysis.3

Are Americans of All Ages Shortsighted?

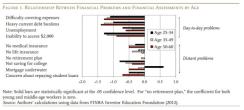

To test whether workers are shortsighted about their finances at different ages, the sample was divided into three age groups: young workers (ages 25-34); middle-age workers (ages 35-49); and workers approaching retirement (ages 50-60).4 The results of the regressions for each group, presented in Figure 1 and Appendix Table 2, show that financial assessments at all ages are clearly short-sighted. In all three age groups, all four day-to-day problems are associated with large, statistically significant reductions in financial satisfaction. The reductions are generally 1 point or more on the scale from 1 to 10, with only one less than 0.5. Reductions associated with distant problems, by contrast, are never greater than 1 and are greater regress than 0.5 in only three cases.5

Statistically significant relationships between financial assessments and specific problems, especially distant problems, vary considerably by age. Among day-to-day problems, the inability to access $2,000 is associated with much larger reductions in satisfaction at younger ages, and heavy debt burdens are related to a greater reduction at older ages.

Among distant problems, only not saving for college and not having medical insurance are associated with statistically significant reductions in all three age groups.6 Among young workers, such reductions are also associated with concern about repaying student loans; among middle-age workers, with not having life insurance and having a mortgage greater than the value of one’s house; and among workers approaching retirement, with concern about repaying student loans and having a mortgage greater than the value of one’s house. A surprising result is that having no retirement plan – neither defined benefit pension accruals nor 401(k)/IRA savings – has no statistically significant effect on the financial assessments of workers in any age group, even those approaching retirement.

While the relationship between worker assessments and specific financial problems varies significantly by age, the incidence of problems is much more similar across age groups (see Figure 2). This similarity is especially true for day-to-day problems, which are associated with the largest reductions in financial satisfaction.7

Are Americans at All Income Levels Shortsighted?

To gauge whether the financial assessments of workers at all income levels are shortsighted, the study divided each age group into terciles based on household income, adjusted for household size.8 The top, middle, and bottom income terciles of each age group were combined into the top, middle, and bottom income terciles used in the analysis.

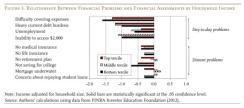

The results of the regressions for each tercile, presented in Figure 3 and Appendix Table 3, show that the financial assessments of workers in all three income groups are clearly short-sighted. With one exception, all four day-to-day problems are associated with large statistically significant reductions in financial satisfaction in all three income terciles. The reductions are again generally equal to or greater than 1 and in only one case less than 0.5. Reductions in financial assessments associated with distant problems, by contrast, are never greater than 1 and exceed 0.5 only once.9

Relationships between financial assessments and specific deficiencies vary much less by income than they do by age. The major exception is not having a retirement plan. The study found no relationship between this deficiency and the financial satisfaction of workers in any age group. But, among income groups, having no retirement plan is associated with a statistically significant reduction in financial assessments for the top income tercile.

Not surprisingly, the incidence of financial problems varies much more by income than it does by age: deficiencies are much more prevalent in lower income households (see Figure 4). For example, 80 percent of households in the bottom third indicate that they have difficulty covering expenses compared to 33 percent of households in the top third.

Conclusion

This study finds that worker financial assessments are present-minded at all ages and income levels. The relationship between financial satisfaction and particular issues varies by age much more than by income. But at all ages and income levels, financial assessments are highly correlated with day-to-day problems, with much more muted relationships to distant problems. Workers at all ages and income levels thus cannot be expected to devote much effort to addressing distant financial needs.

This lack of attention to distant needs does not mean that people will resist efforts to nudge them in the right direction, as evidenced by the success of auto-enrollment in dramatically raising 401(k) participation rates, especially among young and low-income workers. A lack of salience, rather than hyperbolic discounting, would seem to underlie the muted relationships between financial assessments and distant deficiencies. With the shift in financial responsibility to households, it is important to make saving easy and automatic for households at all ages and income levels, so that they can set aside enough to secure a basic level of financial well-being in retirement.

Steven A. Sass is a research economist and Jorge D. Ramos-Mercado a research assistant at the Center for Retirement Research at Boston College.

Endnotes

1 Sass, et al. (2015a and 2015b).

2 “Households in the labor force” excludes households in which the respondent, spouse, or partner is retired or disabled; or the respondent is living with parents or roommates, and thus not responsible for the finances of a household. The age of the respondent is taken as the age of the household. The dataset includes population weights, which are used to make the sample nationally representative, as the exclusions did not result in any significant differences in demographic characteristics between the study sample and all respondents ages 25-60 in the dataset.

3 The analysis also includes the following control characteristics: marital status, education, ethnicity, financial literacy, risk aversion, has seen a financial advisor, county unemployment rate, household income, and age.

4 The sample sizes were 2,397, 4,125, and 2,951, respectively.

5 The day-to-day problem associated with a reduction in financial satisfaction of less than 0.5 is unemployment among middle-age households, a reduction of 0.4. Note that the estimate is for the reduction in financial assessments in addition to the effect of unemployment on other financial conditions, such as the household’s ability to cover daily expenses and current debt payments. The three instances where distant problems are associated with reductions in satisfaction of greater than 0.5 are young and middleage households not saving for college (-0.8 and -0.6, respectively); and older households concerned about repaying student loans (-0.7).

6 The reduction is relative to the financial assessments of households without dependent children or with dependent children that are saving for college.

7 Note that our measure of prevalence indicates the presence of a deficiency, not its effect on the household’s objective financial condition. Measures that indicate the effect on a household’s objective financial condition could produce different results.

8 Incomes were adjusted for household size using the OECD equivalence scale (OECD, no date.). The adjusted household incomes in the middle tercile of the 35-49 age group range from $25,000 to $62,500 in 2012 dollars.

9 Unemployment in the top income tercile is the one day-to-day concern that is not associated with a statistically significant reduction in household financial assessments. The only distant concern associated with more than a 0.5-point reduction in household assessments is not saving for college by households in the low-income tercile – a 0.7-point reduction relative to households without dependent children or with dependent children that are saving for college. This somewhat surprising result could be due to the OECD equivalence scale underestimating the financial burden that children represent for low-income households and/or a relatively large increase in the financial assessments of low-income households that are saving for college.

References

FINRA Investor Education Foundation. 2012. Financial Capability in the United States. Washington, DC: FINRA Investor Education Foundation. Available at: http://www.usfinancialcapability.org/ downloads/NFCS_2012_Report_Natl_Findings. Pdf

OECD. no date. “Adjusting Household Incomes: Equivalence Scales.” Paris, France. Available at: http://www.oecd.org/eco/growth/OECD-NoteEquivalenceScales.pdf

Sass, Steven A., Anek Belbase, Thomas Cooperrider, and Jorge D. Ramos-Mercado. 2015a. “What Do Subjective Assessments of Financial Well-Being Reflect?” Working Paper 2015-3. Chestnut Hill, MA: Center for Retirement Research at Boston College.

Sass, Steven A., Anek Belbase, Thomas Cooperrider, and Jorge D. Ramos-Mercado. 2015b. “Dog Bites Man: Americans Are Shortsighted About Their Finances.” Issue in Brief 15-4. Chestnut Hill, MA: Center for Retirement Research at Boston College.