The UK senior housing sector has evolved from a niche alternative asset class into a major component of institutional real estate portfolios. Below, we examine the forces shaping the market, including supply-demand fundamentals, performance dynamics, and broader challenges and opportunities.

Rapidly aging population

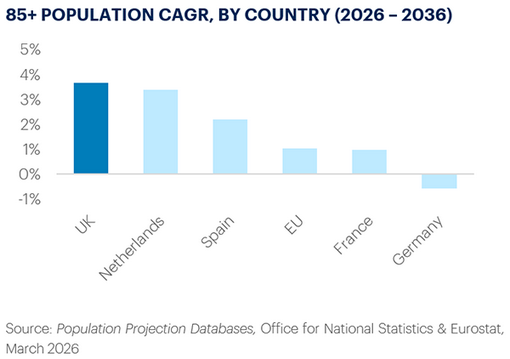

The UK population is ageing at one of the fastest rates in Europe. Over the next decade, the 85+ age cohort is expected to grow by 48%, faster than in peer countries like France (39%) and Spain (29%). This translates to over 85,000 additions to this high-dependence age category every year.1,2 Affluent baby boomers now make up a large and influential demographic force. This group has not only accumulated significant wealth over their working lives – they also demand choice, flexibility, and quality in later life living options. Demand is reinforced by structural changes in household composition, with many older adults living longer, often with chronic but manageable health conditions. The spectrum of senior living options now spans traditional care homes (residential and nursing care) to purpose-built retirement communities and assisted living units.

Supply constraints

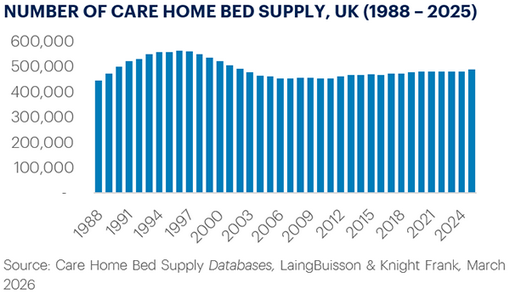

Despite rapidly rising demand, the UK faces severe challenges in delivering senior housing. Current stock is estimated at approximately 500,000 beds, but supply has grown only 0.3% annually over the past decade, while the 75+ population has increased 3% per year.3

According to the Mayhew Review conducted in 2022 by the longevity thinktank ILC UK, at least 50,000 new beds are required annually to keep up with demand.4 In 2024, only 86 new care home beds were delivered nationwide.5 Knight Frank estimates the UK could face a shortfall of 200,000 care home beds by 2050 if current trends persist.6

Development remains challenging

Development remains constrained due to planning constraints, onerous environmental rules, and rising costs of construction and labor. Debt costs remain elevated, keeping development margins for new schemes tight and making returns dependent on location and build quality. In the UK, high-income catchments with strong private pay demand are concentrated in London and the southeast of the country, where half of all beds are self-funded versus only a third nationwide.7 However, even in the southeast, new development is challenged by widespread NIMBYism, ongoing planning problems, and the scarcity and high cost of suitable land plots. The narrow focus on higher-end retirement living also leaves large gaps in the mid-market segment and in rental-oriented supply, further amplifying occupancy and pricing pressures for existing homes.

High occupancy drives fee growth

The widening gap between demand and supply will continue to drive performance. Recent industry data indicates occupancy levels approaching 90%, the highest since the pandemic. According to Green Street, UK occupancy fell as low as 79% during the COVID outbreak, but the sector has since rebounded.8 Fee growth has also been strong; Knight Frank data shows that average weekly fees have grown by approximately 9% p.a. over the last three years.

Rising fees reflect factors such as higher operational costs (increases in minimum wage and national insurance) and limited supply growth, which pushes up pricing power for operators. Rental inflation may have moderated in other property types (e.g. UK residential), but in the care sector, there is little evidence of a slowdown.

Falling wage inflation spurs margins higher

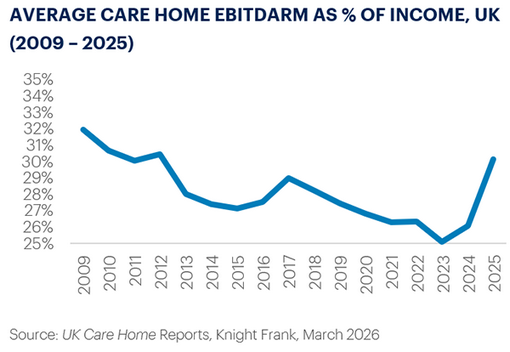

Labor remains the largest cost for care home operators, historically representing 56–58% of income. Post pandemic wage and inflation pressures pushed this to 62% in 2023, with nurse pay up a third since 2020 and carer wages up 50%. More recently, these pressures have eased, and staff costs fell back to 55% of income in 2025, which has improved sector profitability.9

The use of technology and AI is also raising margins. Integrated building infrastructure reduces operating costs and reduce system failures, while real-time monitoring lowers maintenance needs. Automation and digital tools streamline administrative tasks and cloud-based platforms support efficient decision-making. Together, these technologies improve operational efficiency and the resident experience through enhanced safety and improved wellbeing.

Attractive yield profile and long-term growth

Compared to other property sectors, yields in UK senior housing remain attractive on a capex-adjusted basis. Knight Frank data for February 2026 shows that prime assets in the southeast of the UK are priced at 5.5% yield, significantly higher than the 4.00-4.25% range quoted for prime BTR in London and the southeast.10 Senior housing yields in Continental Europe tend to be even higher, typically above 6%, reflecting the lower level of sector maturity and liquidity in the mainland. Compared to Europe, the UK is seen as a more mature, more consolidated and institutionally penetrated market with lower operational and regulatory risk. Green Street’s forecasts for rent growth in UK senior housing (~3.4% p.a.) are among the strongest in the European real estate universe.11

Ongoing institutionalization with greater engagement from international investors

The UK care home sector, though ahead of its European peers, still offers substantial room for institutionalization. Much of the stock is outdated and unsuitable for the needs of today’s residents - 80% of senior housing is over 20 years old, two in five homes are converted rather than purpose-built, and one in three beds still lacks en‑suite facilities.12

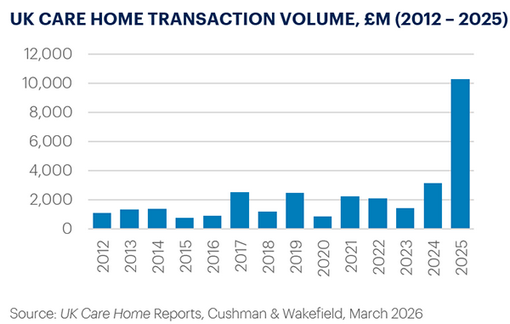

Institutional capital is rapidly moving in. The market has shifted from fragmented, small-scale operators to large, high-value deals. In 2025, M&A activity hit record levels, with WholeCo transactions making up 90% of annual volume and total deal value surpassing £10bn—five times the prior five-year average.13 The US REIT Welltower deployed more than £7bn in the sector last year, including one of the largest transactions ever completed – the acquisition of Barchester Healthcare (284 assets, including developments) for £5.2 bn, structured under a long-term management contract and triple-net lease arrangements. Other major deals were the £1.2bn purchase of HC One (also by Welltower), and CareTrust REIT’s £450m acquisition of Care REIT, currently under review by the Competition and Markets Authority.14

Momentum is expected to remain strong. US investors with lower capital costs continue to target the UK, attracted by stable, yield‑driven real assets backed by resilient demand. Interest is also rising in B- and C‑grade portfolios with consolidation and value‑add potential. Across Europe, senior housing now ranks just behind student housing in investor appeal.15

Future Considerations: Labor, Regulations, and AI

The shortage of skilled care workers remains a major constraint for UK operators. More than 100,000 carer roles remain unfilled in the sector, and the gap is expected to widen as the population ages, driving up labor costs and putting downward pressure on operator margins.16 Workforce pressures intensified in 2025 when the government rolled back relaxed visa rules for overseas care workers, a move likely to increase reliance on domestic recruitment and retention.

Unsurprisingly, operators are exploring the application of AI and advanced technology in care settings. These include the use of inexpensive wearables and in‑room sensors to track vital signs, detect falls, and reveal health trends, enabling earlier intervention, safer independence, and potentially lower staffing needs. A UK pilot has shown significant reductions in falls and ambulance calls. AI chatbots can also offer low‑cost companionship and cognitive support, helping ease loneliness and communication barriers, though they cannot always replace human interaction.

Heitman’s Approach to Investing in UK Senior Care

Heitman’s experience in the UK senior housing sector spans 15 years. We believe the sector continues to offer compelling investment opportunities, driven by structural demographic shifts, long-term undersupply, and resilient operational performance. Learn more about Heitman’s approach to investing in European alternative sectors here: Heitman | Find Value in the European Alternative Sectors

1National population projections: 2022-based, Office for National Statistics, January 2025

2 EUROPOP2023 – Population projections at national level, Eurostat, June 2023

3Healthcare Development Opportunities 2026, Knight Frank, March 2026

4 The Mayhew Review – Future-proofing retirement living: Easing the care and housing crises, International Longevity Centre UK, November 2022

5 Just 86 extra UK care home beds created in 2024, data shows, Financial Times, March 2025

6 Healthcare Development Opportunities 2024, Knight Frank, May 2024

7 Empowering Quality Care: Private Pay's Impact on Care Home Excellence (England), Cornerstone Care Solutions, July 2023 8 Healthcare Sector Update, Green Street, September 2025

9 Care Homes Trading Performance 2025, Knight Frank, December 2025

10 UK Living Sectors Yield Guide, Knight Frank, March 2026

11 Global Property Allocator, Green Street, March 2026

12 Healthcare Development Opportunities 2026, Knight Frank, February 2026

13 Marketbeat Elderly Care Q4 2025, Cushman & Wakefield, February 2026

14 Watchdog investigates Welltower’s £7bn takeover of 600+ UK care homes, Care Home Professional, February 2026

15 European Investor Intentions Survey 2026, CBRE, February 2026

16 From Crisis to Collapse: Care England Express Concern Over Sudden End to Overseas Recruitment, Care England, May 2025