Roberto Croce, PhD, Avishek Hazrachoudhury, Sladja Carton, and Suren Karapetyan for Fidelity Investments.

Fidelity proprietary research has found that in a trend–following approach, it is possible to complement defensive characteristics with alpha-focused strategies to boost the potential return profile.

Key takeaways

- Trend-following strategies, backed by their long and proven track record of defensive performance, have played a critical role in portfolio crisis risk offset.

- Our research found that risk-taking in a trend-following approach is dominated by beta timing, rather than relative value investments implied by trend positioning within asset classes.1

- Furthermore, beta timing is the main driver of “crisis alpha” of trend following, exhibiting a negative correlation to equities, particularly during periods of market stress. In contrast, relative revalue investments contribute very little to crisis alpha.

- This suggests it may be possible to keep the crisis alpha characteristics intact while reallocating the relative value component toward a richer set of alpha signals.

- Increasing exposure to trend beta and complementing it with a market neutral strategy, such as carry, results in a more resilient portfolio with a similar crisis alpha profile but higher return potential, particularly in environments where equities are performing well.

Understanding return and defensiveness in managed futures

A trend-following approach is often viewed as primarily suited for defensiveness, while otherwise being neutral, or even detracting, from portfolio returns. We sought to challenge this long-held belief, by exploring what drives the crisis alpha of trend-following and assessing how it can be preserved while improving overall return potential. Specifically, we examine whether crisis alpha is driven by the relative value investments implied by trend positioning within asset classes or beta-timing decisions—namely, whether to be long or short across asset classes. We believe this to be a crucial issue to understanding how the stability and overall return of a trend strategy might be improved while still preserving its valuable defensive characteristics.

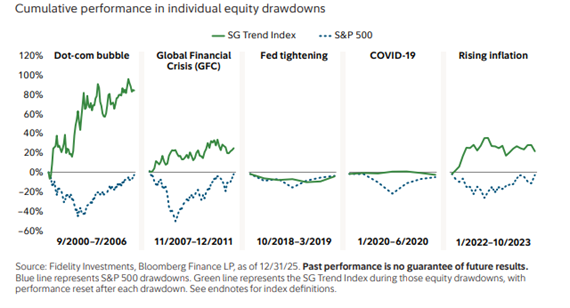

As illustrated in Exhibit 1, trend-following strategies, as represented by the SG Trend Index, have performed very strongly relative to the S&P 500 during equity drawdowns, particularly during major financial dislocations since 2000. This performance is the basis for the term “crisis alpha,” which captures their core return profile.

Exhibit 1: SG Trend Index outperformed during equity drawdowns, especially during prolonged periods of market distress and dislocations.

In our research, we created a hypothetical trend-following model and decomposed it into beta-timing decisions (whether long or short, and by how much) and relative value decisions (whether long or short one market versus another). We evaluated the results of those two separate hypothetical sub-portfolios, finding that 76% of the risk and 78% of the excess return comes from the beta-timing rather than the relative value component.2 Beta-timing decisions also drive most of the prototypical characteristics of trend-following approaches, including the crisis alpha profile. Specifically, we found that on average across asset classes, the beta timing component was more than twice negatively correlated to equity compared to the relative value component.

These results raise the question of whether it is possible to preserve the crisis alpha defensive characteristics while enhancing trend strategies with a richer set of alpha signals. Our research suggests that it is indeed possible to completely replace the relative value component with a significant allocation to another, higher Sharpe ratio relative value strategy, and keep most of the crisis alpha benefits of the strategy. That is the key finding of this paper. If you want trend-following crisis alpha but also want a strategy with higher average return—particularly in markets where equities are thriving—our research analysis suggests it’s possible to have both.

Conclusion

When investors are weighing an allocation to managed futures, it is important to consider specific goals over the short- and long-term. A trend strategy may not deliver strong results during normal market environments when crises are absent and trends are muted, but as our research has shown, there is a way to maintain defensive characteristics while enhancing return potential. For this reason, a managed futures strategy is well-suited for customization depending on an investor’s goals and risk appetite. In particular, incorporating a broader toolkit of strategies complementary to trend can help better achieve investor objectives.

Learn more about alternative investment strategies at Fidelity Institutional.

Please visit Fidelity’s Communities on Alternative Investments.

1 For more, please see, “Trend-following crisis alpha: Does it come from beta timing or market selection?” Fidelity Investments, April 2026.. 2 Ibid

Endnotes See “Trend Following with Managed Futures: The Search for Crisis Alpha,” by Alex Greyserman and Kathryn Kaminski, Wiley, Aug. 1, 2014.

Intended for investment professional or institutional investor use only.

Unless otherwise expressly disclosed to you in writing, the information provided in this material is for educational purposes only. Any viewpoints expressed by Fidelity are not intended to be used as a primary basis for your investment decisions and are based on facts and circumstances at the point in time they are made and are not particular to you. Accordingly, nothing in this material constitutes impartial investment advice or advice in a fiduciary capacity, as defined or under the Employee Retirement Income Security Act of 1974 or the Internal Revenue Code of 1986, both as amended. Fidelity and its representatives may have a conflict of interest in the products or services mentioned in this material because they have a financial interest in the products or services and may receive compensation, directly or indirectly, in connection with the management, distribution, and/or servicing of these products or services, including Fidelity funds, certain third-party funds and products, and certain investment services. Before making any investment decisions, you should take into account all of the particular facts and circumstances of your or your client’s individual situation and reach out to an investment professional, if applicable.

Views expressed are as of March 2026, based on the information available at that time, and may change based on market and other conditions. Unless otherwise noted, the opinions provided are those of the author and not necessarily those of Fidelity Investments or its affiliates. Fidelity does not assume any duty to update any of the information.

Risks

Commodity interest trading involves substantial risk of loss.

Past performance is no guarantee of future results.

Managed futures techniques are different from the risks ordinarily associated with traditional equity investments and are considered complex trading strategies. Such techniques and strategies include the use of derivatives, short sales, leverage, and investments in commodities and commodity-linked securities. Short sales pose more risk than long positions. Because a short position loses value as the security’s price increases, the loss on a short sale is theoretically unlimited. Regulatory bans on certain short selling activities may prevent a fund from fully implementing its strategy. Leverage can increase market exposure, magnify investment risks, and cause losses to be realized more quickly. The use of futures, forward contracts, options, swaps, and other derivative instruments may result in losses. The value of these derivative instruments may pose risks in addition to and greater than those associated with investing directly in securities, currencies, or other instruments and may be illiquid or less liquid, volatile, difficult to price, and leveraged so that small changes in the value of underlying instruments may produce disproportionate losses. The use of derivatives is a highly specialized activity that involves investment techniques and risks different from those associated with investments in more traditional securities and instruments. Moreover, a relatively small price movement in a derivative contract may result in substantial losses, exceeding the amount of the margin paid. The use of derivatives can increase the risk exposure to underlying assets and their attendant risks, while also exposing the risk of mispricing or other improper valuation and the risk that changes in the value of a derivative may not correlate as anticipated with the underlying asset, rate, index, or overall securities markets, thereby reducing their effectiveness. Stock markets, especially foreign markets, are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments. Fixed income investments entail interest rate risk (as interest rates rise, bond prices usually fall), the risk of issuer default, issuer credit risk, and inflation risk. Securities selected using quantitative analysis can perform differently from the market as a whole as a result of the factors used in the analysis, the weight placed on each factor, and changes in the factors’ historical trends. The value of commodities and commodity-linked investments may be affected by the performance of the overall commodities markets as well as weather, political, tax, and other regulatory and market developments. Commodity-linked investments may be more volatile and less liquid than the underlying commodity, instruments, or measures. Non-diversified funds that focus on a relatively small number of stocks tend to be more volatile than diversified funds and the market as a whole. These alternative investment strategies may not be suitable for all investors and are not intended to be a complete investment program for any investor.

Past performance and dividend rates are historical and do not guarantee future results.

Fidelity Investments is an independent company, unaffiliated with Institutional Investor LLC. There is no form of legal partnership, agency affiliation, or similar relationship between your financial advisor and Fidelity Investments, nor is such a relationship created or implied by the information herein. Fidelity Investments is a registered service mark of FMR LLC.

Fidelity Investments® provides investment products through Fidelity Distributors Company LLC; clearing, custody, or other brokerage services through National Financial Services LLC or Fidelity Brokerage Services LLC, Members NYSE, SIPC.

Institutional asset management is provided by FIAM LLC and Fidelity Institutional Asset Management Trust Company.

1233739.2.0