By Erik Norland, CME Group

AT A GLANCE

- Slower copper production in recent years has led to a shortage with demand rising.

- Copper prices followed China’s pace of growth, which rebounded in the second half of 2020 and the first half of 2021.

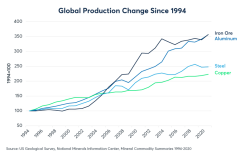

Slow Growth in Copper Supplies

Over the past three decades mining output for copper grew far more slowly than for most other metals, rising just 123%. Over the same period, aluminum production grew by 256% and iron ore production rose by 257%. Since 2013 copper mining output has grown slowly, at just 1.7% per year, less than half aluminum’s 4.6% annual pace of supply growth.The exceptionally slow growth in copper supplies resulted from a combination of factors. First, copper prices fell 58% between the beginning of 2010 and the beginning of 2016, falling close to the metal’s cost of production and thereby discouraging new investments in mines and ore-processing facilities. Secondly, the copper content of copper ore has declined steadily over time. While total discovered reserves of copper have continued to climb, the cost of extracting copper has been on the rise and a large part of that cost is energy.

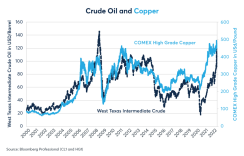

Energy Costs and Copper

Mining and refining metals is an energy-intensive business. As such, copper prices tend to show a great deal of co-movement with the price of West Texas Intermediate crude oil, as well as other crude oil benchmarks. In the past, one might have assumed that this relationship was mostly on the input side: higher/lower crude oil and natural gas prices made mining and refining copper more/less expensive. That assumption is still valid today.However, the sharp rise in oil and natural gas prices in 2021 may be raising demand for copper by fueling interest in alternative technologies such as wind, solar, batteries and electric vehicles, all of which imply the use of copper either directly or indirectly. This may be especially true in Europe and Asia, home to 75% of the world’s population, where natural gas prices have risen to 7-8x North American levels.

The Energy Transition

The energy transition may generate strong demand for copper and other metals such as lithium and cobalt. During the past decade, the cost of solar energy fell by nearly 70% while the cost of batteries fell by a similar amount. Since 1990, the costs of solar energy and battery storage have fallen by close to 98%. If such trends continue over the next few decades, it will be possible to imagine a future of abundant, carbon-free energy, but one that requires a great deal more copper wiring.The transition is already becoming apparent in ground transportation. Sales of electric vehicles (EVs) surged 160% worldwide in 2021 to 2.6 million vehicles. Moreover, those EVs accounted for less than 4% of the global vehicle sales. If EVs sales continue to grow at this fast pace, increasing their market share relative to combustion engine powered cars, it implies potentially strong demand growth for copper and other metals. The cost of EVs has been falling rapidly, and EVs may become less expensive than vehicles power by combustion engines by the second half of the 2020s.

Among the world’s major economies, the fastest growth in EV demand has come from China, where EV sales grew by nearly 190% last year. Even outside of EV sales, China’s economy has been the single most important source of copper demand for the past two decades.

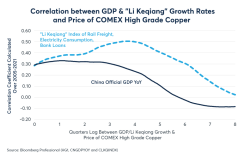

China’s Influence

Each year China buys about 40%-50% of the newly mined copper. Some of raw copper is used domestically, while much of it is re-exported in the components of intermediate or finished goods. The pace of growth in China’s manufacturing sector has often correlated strongly both to the current price of copper as well as copper prices three to five quarters in advance. To measure the pace of growth in China’s manufacturing sector we prefer to use the Li Keqiang Index, which measures electricity consumption, rail freight volumes and bank loans. This particular measure has been a much stronger indicator of demand for copper and other commodities than China’s official GDP, which includes other components such as services and government spending that are less relevant to raw materials.

Having dipped sharply early in the pandemic, China’s pace of growth rebounded strongly in the second half of 2020 and the first half of 2021. Copper prices followed this rebound closely. Since then, the pace of China’s industrial growth has slowed significantly. As China slowed, copper prices traded sideways for several months before recommencing a relatively tepid rally in the past few months. Copper’s recent gains may be in response to the Russo-Ukrainian conflict. Russia produced 850,000 tons of copper in 2021, about 5% of the world’s total.

China’s economy, though still growing, is encountering several headwinds including those coming from higher raw materials prices, declining housing prices, slower export growth, high levels of debt, sharply higher corporate bond yields and a highly valued currency. Should China’s growth continue to slow, it might increase the risk of copper prices coming under pressure later this year or in 2023. However, if copper prices continue to rise, despite potentially slower growth in China, the aforementioned energy transition may be the reason why.

The Pandemic Shift in Consumer Demand

Between December 2019 and December 2021, U.S. consumers spent 18% more on manufactured goods but only 6% more on services, and they weren’t alone. In the U.S. and around the world,consumers shifted to purchasing more manufactured goods, including consumer electronics and other items that involve significant copper content.However, most of the world is returning to a new version of life-as-normal, and in most regions of the world consumers appear set to shift their spending back towards experiences and away from purchases of manufactured goods. This may limit demand growth in copper and may also hamper export growth in China. In the short-term such a shift in consumer demand might offset some of increased demand for copper resulting from the energy transition.

Read more articles like this at OpenMarkets