In a world of scarcer growth and rising competition, the future belongs to companies that understand the transformative power of technology and successfully integrate it within their core business models. This was demonstrated and accelerated by the Covid-19 lockdowns of 2020. The outperformance of technology and technology-related companies is a powerful reminder that tech opportunity is no longer confined to hardware, software, and the internet giants. What’s more, the tech-driven growth is far from over.

Research by Jennison Associates, a leading active manager with more than $241 billion of assets under management (as of June 30, 2021) supports the position that there’s a wide frontier ahead for new market leaders to emerge. Thousands of smaller companies around the world, and millions of people in developed and emerging markets, are just beginning to adopt many established and evolving technologies. And of course, tech innovations are also occurring across large companies, if not with the dramatic growth potential that smaller or less well known businesses offer.

In the United States, traditionally at the forefront of technology disruption, next-economy capex spending has risen above 50% of total capex spending. Jennison’s analysts believe this trajectory will continue – and believe that companies elsewhere in the world, including in Southeast Asia and Latin America, are trending in the same direction. While China is another example of a market that has been influenced by technology, the nation’s sociopolitical dynamics introduce a different set of investment considerations.

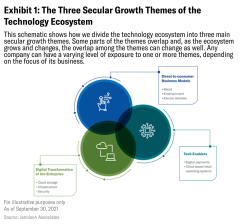

Three tech themes to watch

As Jennison performs ongoing analysis to identify equity investments with above-average, lasting growth potential, overarching themes often emerge. Amid rapid technology change and adoption, the bottom-up conclusions from their most recent research point to three catalysts for earnings and revenue growth in the U.S. and globally:- Direct-to-consumer business models

- Technology enablers

- Digital transformation of the enterprise

This special report will examine each of these key investment themes in depth.

But that’s exactly what Mark Baribeau, Managing Director and Head of Global Equity at Jennison Associates, will tell you. During a recent conversation with II, he explained why he believes the three tech trends shown in Exhibit 1 are vital for investors to monitor – especially select B2B and B2C companies including smaller, fast-growing businesses with a niche focus.

You believe the growth opportunity in tech is really only getting started and that it has legs for a long time to come. How extended do you think the opportunity is?

Just think about the recent tech cycles that we’ve been through. The 1990s was about personal and networked computing, and then the cell phone. The internet dominated the 2000s. Since 2009, it’s been mobile internet. So every cycle is different, with different winners. Technology is one of the richest investment arenas because you’re constantly moving to the next set of solutions.Looking ahead, our analysis at Jennison has identified three big trends that we believe are going to dominate spending and markets for the next few years.

Number one is the transition to direct-to-consumer business models. That’s in e-commerce, but also in global brands and new entrepreneurs who are creating brands.

Second, you have the technology enablers in that ecosystem. These companies are providing everything from digital payments to cloud-based retail operating systems, like Shopify, and they’re enabling the big digital transition to occur.

Then, third, we’ll see accelerated digital transformation of the enterprise. This is really the move to cloud-based solutions, which will be the biggest pure technology shift we go through. And we’re truly just getting started with the transition to cloud, too.

Please talk more about the transition to direct-to-consumer models. We’ll get to the other two themes in a moment...

Sure. Transitioning to a direct-to-consumer model is important for many reasons. It gives companies better control of inventory. They’ll know where demand is strong around the world and can move products in and out of markets quickly. It allows them to change their product lineup quickly based on changes in tastes and other factors. This makes them less susceptible to markdowns and solves many other problems.Some companies, like Tesla, were built with a direct-to-consumer model. Others have successfully made the transition. If you think of luxury brands such as LVMH, the majority of their fashion and leather sales now occur only in their own boutiques or on their websites rather than via third party wholesalers.

But many of the companies that have transitioned already had at least some experience selling in direct-to-consumer channels. There are large global consumer brands that don’t know how to do it, usually because they’ve only sold through third-party wholesalers. These companies are using technologies like Shopify to go direct-to-consumer and their transitions are in the very early days.

The need for so many brands to move to direct-to-consumer models is one reason why we haven’t even scratched the surface in e-commerce.

That seems incredible. During the pandemic there were probably enough boxes delivered to homes to stretch to Neptune and back. How is it possible that we’ve barely scratched the surface in e-commerce?

Because the real excitement in e-commerce is in emerging markets, excluding China. Think of Southeast Asia and Latin America. Many only have an e-commerce penetration in the high-single digits, so they have a long runway of growth ahead to get to the 20% or 25% seen in the rest of the world. And these markets have digitally savvy regions with millions of people where e-commerce is only now exploding in growth.Investors have long looked to emerging markets for high growth potential…

Yes, but we think about emerging markets differently. We don’t think it’s important to have exposure to them just for the old-fashioned growth advantage, or beta play in the market. That’s actually no longer valid. Most of the stock market indices in these countries are dominated by old companies and old industries. Today, you must take a stock selection approach to focus on the digital revolution occurring in those markets.To do that, just look at the top-10 app downloads for any country. The big companies like Google, Facebook, Instagram, Netflix and Spotify will dominate the list, but the last two or three slots will be local businesses. They’re the Mercado Libres of the world, or the new tech platforms developed locally to solve local problems. Look at those companies.

I’m sure many fit the description of tech enablers. How can investors spot the winners in this category?

The tech enablers work behind the scenes to support e-commerce businesses. They’re especially vital in digital payments. As an example, years ago we noticed there was a huge transformation in digital payments going on in China. WeChat Pay and Alipay were defining a very disruptive shift because they identified an opportunity to take a market that was underserved. And they became the two biggest payments companies in the world. They’re now bigger than MasterCard and Visa’s global business.Many tech enablers like these are in emerging markets, but you’ll find them elsewhere, too. For example, we saw a company in the Netherlands go public – it’s called Adyen. Their customer base included Uber, Netflix, Airbnb and other huge digital players – and that’s rule one for spotting tech enablers. If leading-edge tech companies are using the service, they’re doing something right. The big tech firms are usually early adopters of the best-of-breed of technologies, so the services or products they use will often be an indicator of a company’s potential.

Adyen’s competitive advantage is that they have a pure technology stack that’s designed and optimized for e-commerce and can be scaled efficiently and be easily customized, so they can keep innovating. And their growth rate has been dramatically higher than other companies in the digital payments industry. All of those criteria are important.

So that’s how we identify tech enablers. And as long as they continue to win market share quarter after quarter, year after year, their competitive advantage won’t be easy to break.

In general, we stay away from hardware companies. Winning tech enablers almost always offer a software solution because that’s much harder to commoditize than a hardware-based solution.

The third key theme is digital transformation of the enterprise, which you said is really moving to the cloud. As with e-commerce, it feels like we’ve been talking about the cloud forever. How could the opportunity in cloud migration also just be starting?

If you think about the massive IT budgets being spent each year, only a fraction of that is on the cloud.Also, many companies were forced to accelerate their digital transformation during the pandemic and their experience has been positive. So now we’re seeing one application after another getting replaced by a cloud-based application in companies across the world.

Take the communications sector. As just one small example, we’ve been seeing the migration to cloud-based telephony since before the pandemic and that’s accelerating now. So instead of having an office closet full of wiring and your phone service coming in, companies are moving that all to the cloud. You’ll get a platform that offers all services, from video and voice to call centers, and you can use that cloud infrastructure anywhere in the world.

And, again, remember that communications is just one sector in which cloud adoption is now really only beginning for the majority of companies around the world.

How can institutional investors best incorporate these opportunities into their portfolio?

One way is to obviously find growth-oriented investors who specialize in technology and partner with them. Some asset managers buy ETFs or other passive products that focus on tech, but that alone can be too static because technology changes quickly. A combination of active and passive approaches can be good at finding the evolving trends and exiting maturing trends.Learn more about the three themes to watch for tech growth opportunities.

Moving cash online with security and speed is a critical need

Digital payments are a vital and growing part of the digital economy. The transaction value for global digital payments was $5.4 trillion in 2020,3 and payments today account for about 40% of total bank revenues versus just 33% five years earlier.The long-term shift from cash to electronic credit and debit transactions will likely continue, with annual growth rates over the next five years expected to exceed 15% in the United States and Europe and 10% in China.4

Many consumers, especially in emerging markets, are excluded from banking systems because of expense or inconvenience.5 Providers of e-commerce platforms and online financial products and services have a significant opportunity in this large and underserved demographic.

Jennison’s research suggests the potential growth in digital payments remains significant, as the conversion from cash to digital payments is only half completed (Exhibit 4).

Making complex transactions simple

Netherlands-based company, Adyen, is a prime example of a successful tech enabler. The company provides a single-payment platform for companies around the world to process transactions across multiple channels, including online, mobile, and in-store. Adyen’s strength, Jennison’s analysts believe, lies in the fact that it makes an extremely complex and difficult process – payments – simple, reliable, and secure for its clients. But just as important, Adyen’s business is its platform. It is focused on innovating, improving service, and addressing challenges such as security threats. And it’s expanding its footprint across the world, offering companies across industries and geographies the opportunity to incorporate its services into its business model.Adyen’s success shows that companies can bring their disruptive ideas to market, supported by tech expertise that is innovating and constantly improving – all at a manageable cost.

Accessing e-commerce

Canada’s Shopify is another example of a tech enabler, but with a broader array of services. The company provides a one-stop service for businesses seeking to establish online storefronts, taking the hassle out of digital payments management and website creation. Shopify makes it easy for companies and entrepreneurs of all types to quickly set up a business online while maintaining a direct brand relationship with their customers (as opposed to an indirect relationship like selling products through Amazon). Shopify also allows customers to process online payments across a number of different vendors, such as ApplePay or Google Wallet, alleviating the burdensome task of setting up and maintaining separate payment services. Shopify has benefited significantly from rising demand as a greater number of companies participate in e-commerce (Exhibit 5).Jennison notes that this tech enablers secular growth theme is playing out around the world, and they believe it offers opportunities to incumbents but especially to the innovators and disruptors, which are building bigger platforms that serve more customers with different services than was previously considered possible. Much of this opportunity is based upon the third major theme from the tech ecosystem – the digital transformation of the enterprise.

Learn more about the three themes to watch for tech growth opportunities.

Cloud migration has also driven demand for both software – the programming companies need to run their operations – and hardware – the servers needed to host and process software and data. Globally, public cloud revenue is projected to grow at an average annualized rate of nearly 25% to reach $679 billion in 2025 (Exhibit 6).

An old trend: Ever more dollars spent on the new

Jennison notes that this third key investment theme is, in some ways, the latest iteration of a long-standing trend in technology: US capital spending patterns reveal an ongoing shift towards next economy industries at the expense of old economy industries.From the early 1980s through early 2020, the amount of capital spending allocated to old economy industries has fallen from close to 80% to approximately 50%, while capital spending on next economy industries has more than doubled from the mid 20% range to just over 50% (Exhibit 7). In recent years, investment in software and research and development has risen, while spending on technology equipment has dwindled (Exhibit 8). We believe that this shift, while clearly evident, is not yet complete.

The growth of a business’s investment or reinvestment often directly corresponds to the business’s ability to exploit opportunities and raise its overall growth rate. Even among the big scalable platforms, capex spending is higher than the overall market. This investment in technology infrastructure is a core driver of future revenue and earnings growth.

In the realm of giants, small players disrupt

Across industries, Jennison sees profit margin expansion among companies evolving to asset-light balance sheets. Compared to asset-heavy models, benefits can include better return on assets, lower profit volatility, greater flexibility, higher scale-driven cost savings, and higher sales per dollar of assets.In providing cloud services, small companies can make a big impact if their product solves a key need. Cloud-based companies can even disrupt their respective industries, as DocuSign has shown.

As companies increasingly realize efficiencies through the adoption of big data, automation, and software, Jennison believes this should drive growth in the providers of the underlying technology products and services.

This includes companies in the Software as a Service (SaaS) industry, which provides companies with the specialized software they need to take advantage of cloud-based services.

Adapting Faster

Every company is scrambling to digitalize their business as fast as possible. This is a race for survival. While it can be easy to spot a technology-driven company, it is far more difficult to determine which of those are able to grow rapidly and, at the same time, defend their business model and profits.Only a small fraction of companies ultimately create genuine value for themselves, their customers, and shareholders over the long term. These companies can be category leaders or at an earlier stage of their life cycle, and they have a rare combination that our research analysts seek: high quality growth that has both magnitude and duration.

The extended growth opportunity in technology is less about the success of a single product or concept than about a company’s ability to capture more revenue streams from adjacent products or services. A company can diversify its business mix over time in order to capture cash flows from a variety of sources, ranging from digital advertising to cloud services subscriptions.

Identifying next-economy leaders across the world

Further, it’s important to remember that, globally, sales growth has grown more scarce. This increases the need for investors to pinpoint sources of growth with greater accuracy. The proportion of companies in the MSCI ACWI Index growing at 15% or greater per year over five-year time periods has declined from more than 50% in 2008 to about 20% in 2021 (Exhibit 9).The shock of the pandemic has more clearly revealed this new world of technology-driven change. Many companies that had invested in technology or incorporated it deeply into their strategies were well positioned, and we do not expect this trend to weaken even as the worst of the pandemic passes. Across industries, companies are evolving to asset-light balance sheets, leading to higher margins and more sustainable profitability. Compared to asset-heavy models, benefits can include higher return on assets, lower profit volatility, greater flexibility and higher scale-driven cost savings. For investors, we believe this represents an extraordinary opportunity to gain exposure to long-term growth and returns from this unfolding secular change.

Next, in the final section, we’ll take a deep dive into the process Jennison uses to value high-growth companies.

Learn more about the three themes to watch for tech growth opportunities.

But first, where does e-commerce stand now?

E-commerce as a share of global retail sales was about 14% just before the pandemic, but it leapt to nearly 18% as lockdowns and health precautions forced people to stay home (Exhibit 2). Jennison expects this to be a new baseline for continued growth.

Disruptive technology trends have historically occurred first in the U.S. or China before spreading throughout the rest of the world; however, we are starting to see regional models emerge that are unique in their own right. Today, e-commerce penetration in China is in the high 20% range, while in the United States it is at 20%.1 Compared to this, the penetration rates in Latin America and Southeast Asia are both in the single digits, which suggests there’s significant room for growth over the next several years.2

One company, Argentina-based Mercado Libre, has become the dominant e-commerce platform for Latin America. The company’s online trading service enables individuals and businesses to electronically sell and buy items in thousands of categories. It also offers integrated shipping and payment systems. Much of its growth comes from its payments business as well, something that is central to many emerging markets internet and gaming business models. This is very different from what we see in business models of developed markets e-commerce companies.

Why DTC is a vital strategy for businesses

Direct-to-consumer (DTC) business models are based on the growth of e-commerce and are becoming essential for certain types of companies to develop relationships with consumers and bypass intermediaries (and avoid the exorbitant fees or investments they require). They enable companies to build customer loyalty through superior personal service and expand their target markets, projecting their marketing and sales presence across borders without requiring new physical storefronts. The DTC model is fundamentally changing the competitive landscape in several industries and Jennison believes it will only continue to grow.Here’s how DTC is affecting key consumer segments:

Retail

DTC business models are increasingly important in retail. They allow brands to distribute through several different channels – both online and in-store – and control distribution of their product throughout the process.

Companies that have developed successful DTC businesses reap the benefits of an omni-channel approach, which is catching on across the retail spectrum, from luxury goods to athleisure. The approach’s mix of online and physical footprints proved particularly helpful during the pandemic-related shutdowns. We believe retail companies with effective DTC strategies and investment are positioning themselves well for the future. These include companies that employ a DTC model, as well as those that are strategically reducing their exposure to wholesale distribution in favor of the DTC approach.

Entertainment

Netflix used the DTC model to launch and define its content streaming business. By allowing consumers to decide when and where they consume content, through a commercial-free, subscription-based platform, Netflix created a new standard that provided a wholly different alternative to cable television, or linear TV. Netflix was the first streaming content company to invest aggressively in the production of original content (Exhibit 3). The success of its programming has helped attract new subscribers and is now a key part of the company’s competitive advantage, especially against rivals such as Hulu, Disney+, and Amazon Prime.

Netflix has also benefited from its growth in global customers, which reflects the company’s decision to not just stream non-English language content but also invest in creating it. In addition to creating shows that are designed to appeal to global audiences, Netflix has cast popular local talent in vehicles that reflect regional tastes. This approach has given Netflix a foot in the door in local markets and is one of the main reasons it has been able to add more global subscribers (Exhibit 3) than competitors. The company is expected to add games to its platform in 2022 – a format that could further differentiate its platform from its competitors and create room for Netflix to raise subscription fees.

Entertainment is not a winner-take-all industry, in our view, and a few platforms will account for the majority of future revenue.

Electric vehicles

Tesla is a market leader in the electric vehicle industry for a number of reasons, but it also employs a DTC model that sells its cars directly to consumers online. This approach brings the company closer to its end customers, with the added benefit of eliminating the costs associated with dealer networks. As Tesla is demonstrating, the DTC model can generate higher returns on capital and represents a major innovation in an industry that has conducted business in virtually the same way for almost 100 years.

The success of DTC companies is heavily dependent on other parts of the tech ecosystem. Even just a few years ago, new businesses and entrepreneurs faced daunting challenges when using technology. To interact with customers, they had to create a website, manage it, and invest in the infrastructure to support it. Today, this infrastructure, expertise, and innovation can be accessed easily and relatively cheaply through companies that exist to make it easier to conduct e-commerce.

Jennison calls these companies technology enablers, and believes they are a large and growing category of investment opportunities.

Learn more about the three themes to watch for tech growth opportunities.

Valuation is a critical component of Jennison’s growth investment process. The goal of the research analysts’ valuation analysis is to identify underestimated growth opportunities at their inflection point of growth, early on in a company’s life cycle. There is no single overarching valuation methodology used across the firm. Jennison’s analysts use varying valuation methodologies that work best in their particular industry; many use multiple models to arrive at the valuation profile of a company.

P/E can be misleading in high-growth companies

Jennison’s deeply resourced investment team develops an informed view of each company’s earnings profile several years into the future. For companies that are growing revenues and earnings at a very high rate, and trade at high near-term P/E multiples, it is more challenging to forecast a likely outcome over the next several years than it is for companies with slower, but more consistent, growth.For high growth companies, this year’s P/E, or even next year’s P/E, should not be emphasized because they will not adequately capture the true growth potential.

At scale, Shopify could have very high operating margins. Shopify’s business model is driven by high gross margin subscription services that are augmented by highly scalable fixed fee revenue generated from Shop Pay. Importantly, Shopify is focused on innovating, improving service, and addressing challenges, such as security threats. They continue to add services and capabilities that can benefit merchants of all sizes. In particular, Shopify has made big pushes into cross border ecommerce, shipping solutions, and small-to-medium business lending solutions.

Jennison’s way to value these businesses

In valuing these companies, Jennison’s analysts consider several scenarios based on a range of assumptions regarding growth, profitability, and size of addressable market. Additionally, by reverse-engineering a discount cash flow (DCF) model, we also seek to determine the strength of growth, returns, and length of the competitive advantage period reflected in the current market price of these companies. Ultimately, the objective of these efforts is to understand the value created by both the duration and magnitude of growth – areas that the market often gets wrong, usually by underestimating one or both.If Jennison’s analysts believe the market is being too conservative, they may see the stock as a very attractive opportunity.

Growth companies must build an expensive moat – fast

The challenge in valuing these high growth businesses is that their growth opportunities and addressable markets are significant, of course. Emerging as an industry leader is critical because the company must take market share quickly and build up barriers to entry in order to lengthen its competitive advantage period. To do this, growth companies must invest a tremendous amount of their cash flow in sales, marketing, and engineering to build out their product suite. These investments will depress margins and earnings over the near term (about 1–2 years), but are necessary for long-term success.As long-term investors, Jennison looks past these near-term investments and their impact on margins and earnings because their analysts are focused on how these investments will affect the business over the next 3–5 years. Forecasts become more difficult beyond that point. At the three-year period – when the company’s growth is typically more mature, its revenue base is normally higher and it has leverage and scalability. Jennison analyzes the margin structure and discounts the cash flows back to the present. If the discounted valuation is very attractive, Jennison will acquire the stock despite the fact P/E multiples on current earnings may be elevated.

If the analysis described above has correctly captured the growth rate, the duration and magnitude of the growth rate, and the size of the market opportunity, the investment should generate excess returns. If that thesis is not borne out – e.g., the analysis overestimated the size of the market opportunity or the product matures more quickly than anticipated – Jennison exits the position.

As the investment thesis plays out over time, Jennison will begin trimming the position size as the company reaches a more mature state and approaches an internal price target. If the thesis exceeds expectations, Jennison will revise its price targets upward.

Jennison’s growth investing

Most market participants are uncomfortable taking a longer-duration approach to valuation. This is the market inefficiency that Jennison’s market experts – as active fundamental growth investors – seek to exploit. In the long term, the market will always reward the best-positioned company, even if it looks expensive over the short term. The key is to realize when the market is being overly conservative and underestimating the opportunity.Learn more about the three themes to watch for tech growth opportunities.

1 China and US data: “How e-commerce share of retail soared across the globe: A look at eight countries,” McKinsey & Company, March 5, 2021.

2 ASEAN data: J.P. Morgan estimates, Euromonitor, EDTA, and MOEA. As of December 31, 2019. Latam: Statista, EBANX; AMI. March and April 2020.

3 Resarchandmarkets.com, June 7, 2021.

4 Statista, as of January 2021

5 According to the World Bank, 1.7 billion adults remained “unbanked” as of 2017 (the most recent data), yet two-thirds of them own a mobile phone that could help them access financial services. World Bank, “The Global Findex,” April 19, 2018.

Important Information

For Professional Investors Only. All investments involve risk, including the possible loss of capital.

Publishing date: September 30, 2021.

This material is only intended for investors which meet qualifications as institutional investors as defined in the applicable jurisdiction where this material is received. This material is not for use by retail investors and may not be reproduced or distributed without Jennison Associates LLC’s permission.

These materials are for informational or educational purposes only. The information is not intended as investment advice and is not a recommendation about managing or investing assets. Jennison makes no representations regarding the suitability of any securities, financial instruments or strategies described in these materials. In providing these materials, Jennison is not acting as your fiduciary. These materials do not purport to provide any legal, tax or accounting advice.

The views expressed herein are those of Jennison investment professionals at the time the comments were made. They may not be reflective of their current opinions, are subject to change without prior notice, and should not be considered investment advice.

Certain third party information in this document has been obtained from sources that Jennison believes to be reliable as of the date presented; however, Jennison cannot guarantee the accuracy of such information, assure its completeness, or warrant such information will not be changed. Jennison has no obligation to update any or all such third party information. There is no assurance that any forecasts, targets, or estimates will be attained.

The financial indexes referenced herein are provided for informational purposes only. All indexes referenced are registered trade names or trademark/ service marks of third parties. References to such trade names or trademark/service marks and data are proprietary and confidential and cannot be redistributed without Jennison’s prior consent. Investors cannot directly invest in an index.

Jennison uses the Global Industry Classification Standard (GICS®) for categorizing companies into sectors and industries. The Global Industry Classification Standard (GICS®) is the exclusive intellectual property of MSCI Inc. (MSCI) and Standard & Poor’s Financial Services, LLC (S&P). Neither MSCI, S&P, their affiliates, nor any of their third party providers (“GICS Parties”) makes any representations or warranties, express or implied, with respect to GICS or the results to be obtained by the use thereof, and expressly disclaim all warranties, including warranties of accuracy, completeness, merchantability and fitness for a particular purpose. The GICS Parties shall not have any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) even if notified of such damages.

The S&P index(es) (“Index”) is a product of S&P Dow Jones Indices LLC and/or its affiliates and has been licensed for use by Jennison Associates, LLC. Copyright © 2021 S&P Dow Jones Indices LLC, a division of S&P Global, Inc., and/or its affiliates. All rights reserved. Redistribution or reproduction in whole or in part are prohibited without written permission of S&P Dow Jones Indices LLC. For more information on any of S&P Dow Jones Indices LLC’s indices please visit www.spdji.com. S&P® is a registered trademark of S&P Global and Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC.

The MSCI All Country World Index is a free float-adjusted market capitalization weighted index designed to measure the equity market performance of developed and emerging markets. It comprises approximately 24 developed and 21 emerging market country indexes. The net benchmark return is reported net of reclaimable and non-reclaimable withholding taxes. Withholding tax rates used for the benchmark differ from, and may be higher than, the withholding tax rates used when calculating the composite return. The financial indices referenced herein are provided for informational purposes only. When comparing the performance of a manager to its benchmark(s), please note that the manager's holdings and portfolio characteristics may differ from those of the benchmark(s). Additional factors impacting the performance displayed herein may include portfolio-rebalancing, the timing of cash flows, and differences in volatility, none of which impact the performance of the financial indices. Financial indices are unmanaged and assume reinvestment of dividends but do not reflect the impact of fees, applicable taxes or trading costs which may also reduce the returns shown. All indices referenced in this presentation are registered trade names or trademark/service marks of third parties. References to such trade names or trademark/service marks and data is proprietary and confidential and cannot be redistributed without Jennison's prior consent. Investors cannot directly invest in an index.

Certain information contained in this product or report is derived by Jennison in part from MSCI’s MSCI Emerging Markets Index (the “Index Data”). However, MSCI has not reviewed this product or report, and MSCI does not endorse or express any opinion regarding this product or report or any analysis or other information contained herein or the author or source of any such information or analysis. Neither MSCI nor any third party involved in or related to the computing or compiling of the Index Data makes any express or implied warranties, representations or guarantees concerning the Index Data or any information or data derived therefrom, and in no event shall MSCI or any third party have any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) relating to any use of this information.

Any use of the Index Data requires a direct license from MSCI. None of the Index Data is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such.

Jennison Associates LLC (‘Jennison’) has not been licensed or registered to provide investment services in any jurisdiction outside the United States. The information contained in this document should not be construed as a solicitation or offering of investment services by Jennison or a solicitation to sell or a solicitation of an offer to buy any shares of any securities (nor shall any such securities be offered or sold to any person) in any jurisdiction where such solicitation or offering would be unlawful under the applicable laws of such jurisdiction.

Please visit jennison.com/important-disclosures for important information, including information on non-US jurisdictions. In the United Kingdom, and various European Economic Area jurisdictions, information is issued by PGIM Limited. PGIM Limited registered office: Grand Buildings, 1-3 Strand, Trafalgar Square, London, WC2N 5HR is authorised and regulated by the Financial Conduct Authority of the United Kingdom (registration number 193418) and duly passported in various jurisdictions in the EEA. Jennison Associates LLC & PGIM Limited are wholly owned subsidiaries of PGIM, Inc. the principal investment management business of Prudential Financial, Inc. (‘PFI’). PFI of the United States is not affiliated in any manner with Prudential plc, incorporated in the United Kingdom or with Prudential Assurance Company, a subsidiary of M&G plc, incorporated in the United Kingdom. This information is intended only for persons who are professional clients or eligible counterparties as defined in Directive 2014/65/EU (MiFID II), investing for their own account, for fund of funds, or discretionary clients.

©2021 Prudential Financial, Inc. (‘PFI’). PGIM and the Rock symbol are service marks of PFI and its related entities, registered in many jurisdictions worldwide.