For a few years now, the song has remained essentially the same for institutional asset owners and the managers with whom they partner – cost pressure squeezes them incessantly, and with high valuations and low yields, meeting return expectations is a more elusive and difficult goal to achieve. To potentially add incremental portfolio performance and offset some holding costs, investors and managers have looked to perhaps the most versatile tool they can leverage: Exchange Traded Funds (ETFs), and the potential securities lending benefits they can provide.

How securities lending works, and transaction mechanics

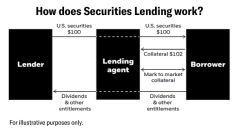

Securities lending is a well-established practice in which an investor who owns a security temporarily loans the security to a borrower in exchange for a fee. The lender retains all economic interests of the security, and therefore maintains exposure to the security’s performance for the life of the loan. Because the transfer of ownership is temporary, the securities can be returned by the borrower or recalled by the lender at any time.

The loan is initiated when a borrower, typically a large financial institution, engages with a lending agent, who acts on behalf of the lender. Borrowers look for a host of securities from the lending agent, including individual stocks and bonds held within ETFs as well as units of an ETF itself. In return for the borrowed securities, the borrower delivers collateral back to the lending agent. This collateral in excess of the market value of the loan, with a daily mark-to-market process during the life of the loan. Additionally, the borrower is required to any distributions on the securities (dividends or interest payments) that occur during the life of the loan back to the lending agent.

ETF investors can potentially derive benefits from two levels of securities lending: (1) the lending of underlying individual constituent securities – which is initiated and managed by the ETF provider and reflected in ETF performance. (2) the lending of the ETF unit itself. By choosing to lend the ETF itself, investors can potentially accrue the benefits of both levels of borrow demand.

Global revenue generated from securities lending reached $7.1 billion in 2018 and $6.4 billion in 2019. It’s not surprising that in what has been a highly volatile 2020, year-to-date global securities lending revenue is down about 20% through October.1 It is noteworthy, however, that global ETF units lending revenues were $132 million through October 2020, a 26% year-on-year increase, as market participants increasingly borrow ETFs to gain broad market exposure.2

Potential for additional yield

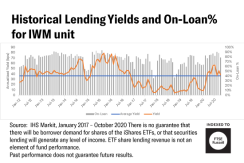

The lending landscape of each ETF varies based on the characteristics of the underlying holdings and market conditions. For example, a basket of small-cap stocks – such as those represented in the Russell 2000 Index – is typically more expensive and operationally complex to manage given their low liquidity relative to larger cap stocks. The relative scarcity can result in attractive lending fees on both the individual securities and of the ETFs that hold the underlying securities. This may potentially contribute to favorable conditions for long holders looking to generate additional returns.

Further, in bearish market conditions borrower demand for small-cap stocks can increase. Investors with a long position in the iShares Russell 2000 ETF (IWM) can aim to take advantage of this by lending the ETF itself to help offset the expense ratio and generate additional income potential.

Use case: Long holders of ETFs seeking yield enhancement opportunities

A pension fund manager held ETFs for long-term beta exposure. The manager periodically engaged with the iShares Markets Coverage team to identify which of their ETF holdings offered potential for attractive lending yields. By lending these ETFs, the manager was able to:

- Maintain exposure to the ETF throughout the life of the loan.

- Potentially offset fund management fees while seeking to generate additional income without deviating from the targeted exposure or asset allocation. (Note: lending income may be subject to a split with the manager’s lending agent)

- Continue to receive all distributions on the security that occurred during the loan.

- Recall the securities on-loan to the borrower at any time.

1 IHS Markit, January 2017 – October 2020

2 IHS Markit

There is no guarantee that there will be borrower demand for shares of the iShares ETFs, or that securities lending will generate any level of income. ETF share lending revenue is not an element of fund performance and share lending is not a service provided by iShares ETFs or BlackRock Fund Advisors, the funds' investment manager and an affiliate of BlackRock Investments LLC.

Carefully consider the Funds' investment objectives, risk factors, and charges and expenses before investing. This and other information can be found in the Funds' prospectuses or, if available, the summary prospectuses which may be obtained by visiting www.iShares.com or www.blackrock.com. Read the prospectus carefully before investing. Investing involves risk, including possible loss of principal.

This information should not be relied upon as research, investment advice, or a recommendation regarding any products, strategies, or any security in particular. This material is strictly for illustrative, educational, or informational purposes and is subject to change.

Small-capitalization companies may be less stable and more susceptible to adverse developments, and their securities may be more volatile and less liquid than larger capitalization companies. Shares of iShares ETFs may be bought and sold throughout the day on the exchange through any brokerage account. Shares are not individually redeemable from the ETF, however, shares may be redeemed directly from an ETF by Authorized Participants, in very large creation/redemption units. There can be no assurance that an active trading market for shares of an ETF will develop or be maintained. Buying and selling shares of ETFs will result in brokerage commissions.

The iShares Funds are distributed by BlackRock Investments, LLC (together with its affiliates, “BlackRock”).

The iShares Funds are not sponsored, endorsed, issued, sold or promoted by Russell, nor does this company make any representation regarding the advisability of investing in the Funds. BlackRock is not affiliated with Russell.

©2020 BlackRock. iShares and BlackRock are registered trademarks of BlackRock. All other marks are the property of their respective owners.

FOR INSTITUTIONAL USE ONLY. NOT FOR PUBLIC DISTRIBUTION.

ICRMH1220U-1353099-1/1