Andrew Harrer/Bloomberg

Zero Hedge made a splashy return to Twitter over the weekend, months after being banned from the website.

The financial news site’s first order of business? Attacking Robinhood, the popular retail investment platform.

#FinTwit was ripe for the takedown: Some retail investors are making major returns using the trading app, despite the market’s volatility.

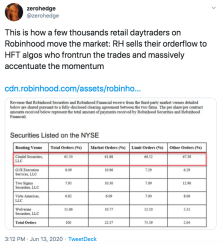

Zero Hedge tweeted on Saturday that retail investors are moving markets because Robinhood sells its order flow to high-frequency trading firms who “front-run” the trades and increase momentum.

Zero Hedge also pointed out that Robinhood engages in a practice called payment-for-order-flow, sharing a tweet that showed “Robinhood’s financial arrangement with Citadel”.

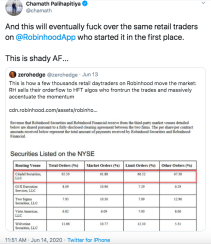

The first tweet was shared more than 2,000 times by other Twitter users, including billionaire investor Chamath Palihapitiya, who claimed that the arrangement will “f--- over” retail investors.

The thing is, though, payment-for-order-flow is nothing new in the investment industry. Short-seller Carson Block’s Muddy Waters Research responded to Palihapitiya’s tweet, pointing out just that.

The practice, said to be pioneered by Bernie Madoff, is something used by Fidelity, e*Trade, Charles Schwab, and TD Ameritrade, among others, SEC Rule 606 disclosures show.

Here’s how it works: An equity retail trader uses a broker like Robinhood to place a trade order. The broker routes that trade to a market maker, which then executes the trade.

If the broker, as Robinhood does, is using a no-commission model, the retail trader doesn’t have to pay a fee on the trade. However, in a pay-for-order-flow model, the market maker pays a pre-set fee (in Robinhood’s case, less than a penny per executed trade) to the broker.

“This has enabled the zero-commission capability,” one industry insider said by phone Monday.

Both FINRA and the Securities and Exchange Commission oversee this practice, and brokers are required to disclose whether they engage in it.

“There’s a whole notion of selling flow and this insinuation that something nefarious is happening,” the source said. “It seems to come up when one of the retail brokers gains traction.”

According to the source, some retail brokers cap how many trades they send to market makers, usually by percentage, to manage risk and concentration concerns. But that isn’t the case everywhere, and it’s unclear whether Robinhood implements this type of cap.

Robinhood’s website shows that the market makers it works with pay rebates at the same rate.

“To ensure we have a fair system, we don’t take rebates into consideration when we choose which market maker will execute your orders,” Robinhood’s site shows.

This is the same fee structure Robinhood uses with all its market makers, including Citadel Securities.

[II Deep Dive: The Unusual Ambitions of Chamath Palihapitiya]

Robinhood, however, has not avoided regulatory scrutiny: FINRA fined Robinhood in December 2019 for “best execution violations related to its customers’ equity orders and related supervisory failures,” an announcement showed. Robinhood paid the $1.25 million fine without admitting or denying wrongdoing.

The settlement was not over the market maker structure itself, but instead over whether Robinhood considered all execution quality factors — like price improvement — instead of simply execution quality. Robinhood has since hired an independent consultant to review the firm’s practices.

A spokesperson for Robinhood declined to comment. Zero Hedge did not respond to a tweet seeking comment. Palihapitiya did not return an email seeking comment.