In a February 6 speech in Philadelphia, U.S. Vice President Joe Biden made clear his exasperation with the present state of U.S. infrastructure, calling it “embarrassing.” One dig in particular that made it around the blog circuit: that New York’s LaGuardia Airport feels as if it’s “in some third-world country.” The reality is troubling: The physical infrastructure in many developing countries is far better than in the U.S.

The economic recovery in the U.S. appears to be fairly broad-based and cyclical. Several years after the 2008–’09 financial crisis, various elements of the U.S. economy have kicked into gear. Labor markets have begun to loosen, the housing market is buoyant, and corporate earnings and margins are at historic highs. It’s no wonder that the S&P 500 has recovered nearly 200 percent since its low in March 2009.

But structural problems in the U.S. economy remain. In fact, they have worsened during this recovery. Long-term unemployment remains high, largely because of a skills gap in lower-income segments of the workforce. Wage inequality has also worsened, with 95 percent of economic gains going to the top 1 percent of income earners. And the relentless myopia of the nation’s politicians and market participants means that long-term challenges, such as the redevelopment of infrastructure, remain unaddressed.

Investors need to understand infrastructure needs more deeply for two reasons. First, the state of infrastructure is a shortcoming of the U.S. economy that has and will affect total-factor productivity, industrial development and, ultimately, competitiveness for years to come. Second, the sector could offer major opportunities for investment, that is, if the proper policy framework is put into place.

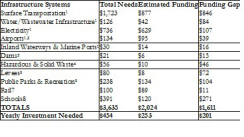

U.S. infrastructure is ripe for rebuilding. The 2013-´14 World Economic Forum Global Competitiveness Report ranks U.S. infrastructure 15th in the world. Countries beating the U.S. in the rankings include emerging markets such as Hong Kong and Singapore, which took the top two spots, respectively, and the United Arab Emirates, which came in at No. 5. The American Society of Civil Engineers recently graded the U.S. infrastructure sector D+, highlighting an approximately $4 trillion infrastructure deficit (see chart 1). That’s larger than the entire U.S. government’s budget.

Source: ASCE, 2013

According to PricewaterhouseCoopers, U.S. pension funds, foreign governments and international organizations have between $300 billion and $400 billion of available capital set aside for U.S. infrastructure projects. Very little of this funding has been tapped, however, despite newfound interest from political and business leaders in addressing these issues. Why? I believe there are three main reasons.

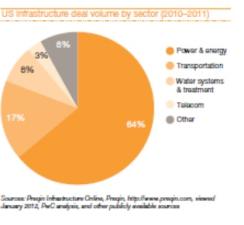

First, there is a conceptual problem in how the U.S. government and its citizens generally think about infrastructure funding. Since the 1930s, most infrastructure spending has taken place through public grants, as opposed to capitalized deals or private financing. As a result, especially in transportation and regulated utilities like water, there is deep skepticism around the role of private entities in U.S. infrastructure. An example that immediately comes to mind is the public’s general disdain for toll roads. Chart 2 shows just how insignificant are public-private relationships in the U.S.

Source: OECD, 2010

Second, there is a coordination problem. The so-called U.S. infrastructure market is in fact composed of hundreds of highly local markets. As a percentage of their total needs, very little financing is done on a state or federal basis. From state to state, regulation varies widely regarding public-private partnerships, tax exemptions and transportation tolling, which has made it very difficult for private money to enter the sector. Only half of the U.S. states, for example, have legal provisions for public-private partnerships.

Source: PwC, 2011

Third, given the surge of U.S. oil production and output from recently tapped oil shale, most private deal flow to infrastructure has been and will continue to be in the energy and utility sectors. Although this is a positive development in terms of overall spending, the U.S. needs a similar level of support for infrastructure projects to boost other sectors such as water and transport.

Source: PwC, 2011

U.S. pension funds would like to increase their allocations to infrastructure, given the inflation hedge/real asset characteristics and long-term/illiquid nature of investment. But a lack of projects open to financing has been a roadblock to pension funds entering the sector. As two experts in U.S. infrastructure financing recently told me, there is a “very short pipeline of potential projects.”

The proposed National Infrastructure Reinvestment Bank offers a sensible solution. First proposed in 2007 by then-U.S. senators Christopher Dodd and Chuck Hagel, the bank would significantly increase and direct allocation of capital toward infrastructure and would prioritize the highest-value projects. Similar arrangements already exist around the world, from the European Investment Bank to development banks in Asia and Latin America.

Structural economic challenges don’t explain daily, weekly or monthly movements in asset prices. As a result, they are often ignored by market participants. But they remain important considerations and can present opportunities for smart investors who look toward a long-term horizon.

Aniket Shah is an investment specialist with the Investec Investment Institute, part of Investec Asset Management.

See Investec's legal disclaimer.

Get more on regulation.