The fixed-income investment landscape today is very different from that seen in the three decades leading up to the financial crisis of the late 2000s. Broadly speaking, from the early 1980s through 2008, interest rates were steadily falling and the world was levering, providing unparalleled dual technical tailwinds of rising prices and ample supply for bond managers.

Today that is no longer the case. We are witnessing a more constrained fixed-income supply, particularly in relation to demand. We are likely to see the very low interest rates in developed markets slowly begin to rise in some regions — the U.S. and the U.K. — while rates remain mired in negative territory in other regions, such as the euro zone and Japan. And that is to say nothing of the broader economic challenges posed by current demographic trends and technological disruptions, which present additional concerns for those seeking to navigate debt markets.

Unconventional monetary policy experimentation by some central banks — and specifically negative rate policies — threaten to produce economic distortions and misallocations of capital that may increase left-tail risks and market stresses, rather than being the panacea policy proponents contend. Indeed, at the end of the first quarter, according to Credit Suisse research, roughly 38 percent of developed-markets bonds overall traded at negative yields. Perhaps unsurprisingly, where negative rate policy is in effect — Denmark, Switzerland, Sweden and Japan and those nations governed by the European Central Bank — the proportion of the bond market trading at negative yields increases to nearly 60 percent. Remarkably, the pool of positively yielding debt in the global fixed-income universe has shrunk by more than $5 trillion in less than two years, which clearly presents a tremendous challenge for investors seeking income and attempting to match assets to liabilities.

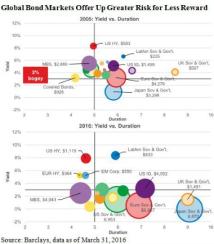

Additionally, the interest rate risk, or duration, embedded in many parts of the global bond market has increased dramatically in recent years, leading investors to have to contend with a landscape in which they are forced to take on greater levels of risk for diminished reward potential (see chart). In 2005 virtually every asset in the Barclays global aggregate bond index and the Barclays global high-yield index yielded 3 percent or more, with the notable exception of Japanese government bonds. Today only relatively small pools of fixed-income assets meet that yield level, and duration has extended in just about every market segment. We at BlackRock find these data to be starkly revealing and think it argues for a strong technical bid in some of the smaller yet higher-yielding asset pools, such as U.S. high-yield and emerging-markets debt. These are some of the only market segments in which the risk-reward profiles appear better today than a decade ago. Given the rising likelihood of defaults in the former sector and the various risks attendant to the latter, however, we think selectivity and flexibility here are vital. Further, both rate volatility and the potential for losses in fixed income will remain elevated for a time.

Responding to this challenging set of circumstances in an opportunistic and flexible manner is critical to investment success. Bond yields in much of the world are likely to remain low for an extended period, and many valuation metrics also suggest that modest returns are in store for equity investors for the foreseeable future. U.S. economic growth is likely to remain decent — if uninspiring — but there are clearly elevated left-tail risks present for the economy and markets. In this environment, we believe that investors are best served by taking a balanced or barbelled approach: combining a set of defensive allocations with some higher-yielding carry assets.

On the defensive side, my colleagues have persuasively argued that realized inflation and breakevens are poised to grind modestly higher, and we think the long end of the inflation curve — and forward markets — holds compelling valuations. We would also argue that investors should consider a modest position of gold in their portfolios, particularly gold denominated in euros, as the significant growth we can expect in the ECB’s balance sheet over the next year should represent a meaningful tailwind to the metal priced in euros. Finally, though market volatility has eased, we would argue that building long-dated volatility positions makes sense when obtained at reasonable prices, since there are myriad risks on the horizon.

For the other segment of the investment barbell, we think carry assets will outperform market beta exposures in the year ahead. The long-end of the U.S. yield curve still looks decent, at least relative to other developed-markets options on offer. That could be combined with more credit-sensitive carry, such as higher-in-the-capital-stack securitized assets. With regard to sovereign rates, we would seek out duration in markets such as Australia, New Zealand and South Korea, where the central bank policy is likely to be easy but is not punishing investors with negative rates.

To be clear, we think fixed-income investment success in the years ahead will require maintaining both flexible and highly diversified portfolios that can avoid the pitfalls of negative rates and potential policy mistakes and can source assets with sound carry, defensive characteristics and even, in some cases, upside potential.

Rick Rieder is chief investment officer of global fixed income for BlackRock in New York.

Get more on fixed income.