Markets, economies and political dynamics are always in flux. That’s a big reason why understanding what trends have staying power — knowing how the environment of today differs from that of the past — is crucial to intelligent, informed investing.

One undeniable source of divergence from the past is the recently heightened currency volatility. Currency volatility can wipe out gains from investments in other assets and create a sense of uncertainty over returns. Taking a different perspective on the dynamics behind currency volatility can help institutions appropriately hedge the risk in their portfolios and generate alpha.

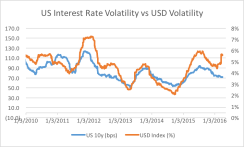

In 2013 currency volatility began to rise as the taper tantrum — the market turbulence that followed the Federal Reserve’s mere intimation that it would wind down its bond buying — took effect. Rising U.S. interest rates forced a sharp move in global rates and led to a substantial pullback in capital from emerging markets.

The more interest rates move, the more the attractiveness of one currency versus another changes. More recently, another dynamic has emerged: Currency volatility and interest rate volatility in the U.S. are diverging (see chart 1).

In the developed world, central banks have increasingly used currencies as a lever to stimulate their domestic economies, because these countries are reaching the end of their debt supercycles and are unable or unwilling to use traditional interest rate channels to support spending. Historically, to spur economic expansion, central banks would cut interest rates to facilitate credit creation. The increase in borrowing would invigorate the economy and push growth above trend. With high debt levels across the developed world and interest rates at their lower bound, however, this maneuver is no longer possible.

Though each developed-market country’s story is slightly different, all suffer from the same problem: a diminishing ability to stimulate economic growth and offset deflation. Japan has been experiencing deflationary stagnation for the past 15 years. The euro zone is dangerously close to the same fate. The next big move for Australia and Canada is likely down, as their household sectors have not yet deleveraged and their commodities sectors have trailed off. All developed markets either need or will soon need economic stimulation, though interest rate policy will likely have very little direct impact.

Currency depreciation works through four channels that are different from those of interest rate–based stimulus — none of which require a pickup in debt. First, a falling currency has the immediate effect of boosting corporate profits through margin expansion. To the extent that a corporation pays costs such as labor and capital expenditures in local currency but earns revenue in a foreign currency, margins immediately expand on the back of currency depreciation. Such a phenomenon contributed to corporate profits in Japan soaring when the yen fell after the introduction of quantitative easing in 2013.

The second channel is the boost to export volumes that occurs when corporations choose either to cut their prices in foreign currency terms or accrue the competitive effects for goods that are priced in local currency terms from the start.

The third channel is the reduction in import volumes as domestic consumers and companies switch their spending away from expensive foreign goods to cheaper domestic ones.

The fourth and final channel is the competitive advantage that arises when domestic corporations shift investment away from foreign countries and when foreign corporations shift investment to markets with a cheaper currency. This factor is the slowest to show an effect but is nonetheless critical to long-term growth.

There is a problem with currency depreciation, however: It is a zero-sum game. Whereas lowering interest rates can be done simultaneously to everyone’s benefit, getting your currency to fall has only one winner. This dynamic fosters a currency war mentality in which each central bank vies for the most favorable position. Market share gains in export markets and global investments, as well as boosts to inflation, all come at the expense of countries that do not depreciate.

This reality has led to conflicts among central bankers — some implicit, others more explicit. The latest iteration of these conflicts came in March when the U.S. Treasury “expressed concern over the [Japanese] authorities’ public statements on the desired direction of the exchange rate.”

In the current low-growth, low-interest-rate environment, practically all developed markets would benefit from a falling exchange rate. It is unlikely that the euro zone can make a full recovery without the euro continuing to decline. The same goes for Japan as the Bank of Japan continues to battle deflation and persuade corporations to invest domestically. Similarly, Australia and Canada would welcome depreciation, as it would boost domestic activity without leading to an expansion of household debt.

Despite the criticism that may come from other countries, we expect central banks to generally act in the best interest of the countries they serve. With interest rates at or below zero, this means using increasingly stronger and stronger tools to support depreciation, such as expanding the quantity and type of assets purchased. Such policy will be a source of continued downside volatility for those currencies.

But that is just one side of the volatility. There is also substantial volatility on the upside because the moves from central bankers get overpriced by the market, creating a temporal mismatch between when the speculators short the particular currency and when the real money flows come in. Such a mismatch happened to the euro several times over the past few months. Despite substantial quantitative easing from the European Central Bank, the euro has been subject to a set of very sharp upside reversals. The reversal of stretched speculative positioning can cause sudden reversals in the euro’s downward trend (see charts 2 and 3). Because volatility is increasing from both sides, it is likely that elevated currency volatility is here to stay.

There are two main implications for institutional investors here. The first is to hedge your foreign equity and debt investments. Because currency volatility is high, it will compose a larger portion of portfolio returns. Unless investors also hold a currency for which the view is the same direction as the asset view, they should insulate themselves from this source of volatility. Moreover, the currency volatility will likely work in the opposite direction as the asset view. Consider that a big driver of returns for stocks and bonds will be easy monetary policy. A primary reason for buying European or Japanese equities is a belief that the ECB and the BoJ will continue to provide stimulus. But that will probably mean the euro and yen will continue to fall. If investors don’t hedge their long exposure to equities in those markets, they stand to lose a good portion of their returns. The very thing being bet on will be detrimental on the forex leg of the position.

This source of volatility can also be wielded to investors’ advantage. Volatility can present an opportunity for alpha, but because currency markets are fairly complicated, institutional investors may consider leaving that to the experts, and there are funds that can take advantage of these opportunities. Capturing currency alpha will be particularly important in a world in which the risk premium on traditional assets, such as stocks and bonds, becomes compressed. At some point, the only possibility for a large move in stocks and bonds will be to the downside. That will not be the case for currencies.

Katina Stefanova is the CEO and CIO of Marto Capital, a New York–based multistrategy asset management firm.

Get more on foreign exchange.