Innovations and customization in equity indexing may provide enhanced opportunities.

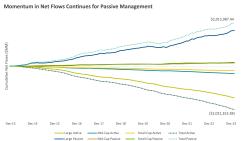

Passive index funds continue to accumulate market share relative to active managers by offering cost-effective market exposure and strong relative performance across many popular market segments, particularly U.S. large cap equities. In fact, this market share has grown exponentially. By the end of 2023, U.S. investors held more than $13.52 trillion in passive funds, surpassing the amount held in active funds by a margin of about $8 billion, according to Morningstar data and Cerulli Associates. One catalyst for this adoption is the perceived simplicity and efficiencies offered to investors, but viewing passive indexing as simple and straightforward ignores other key benefits.

The passive investing landscape has evolved significantly in recent years, with a notable proliferation of indexing options. Today’s passive investing requires active choices, as customization and innovations in index funds have resulted in additional variables to consider, while providing the potential for greater control over investments.

To better understand the evolution and impact of passive investing and index funds, Institutional Investor met with Austin Guy, CFA, Sr. Client Portfolio Manager, Indexing; Jake Weaver, CFA, CPA, Global Head of Equity Index and Christopher Huemmer, CFA, Sr. Client Portfolio Manager, Equity ETFs & Real Assets, all with Northern Trust Asset Management. These experts provided their insights on the potential benefits of index investing strategies, the challenges ahead, and where the most promising opportunities may lie.

Institutional Investor: How has passive investing evolved and what have been the trade-offs in terms of expanding passive coverage?

Jake Weaver: A passive investor is one that uses a rules-based index to get exposure to a specific segment of the market. Typically, passive investors are not making active decisions on the specific securities they buy and sell, and they tend to have a focus on transparency and cost management. One of the biggest evolutions in passive investing has been the expansion of indexing options. New providers have come on the scene and there are more nuanced index exposures now than there were even a decade ago. The evolution has really moved beyond a market cap-weighted benchmark toward a broad variety of index construction options such as factor-based, ESG and thematic indexes. One of the challenges that may not be recognized is that as the options increase, investors must make an active decision when choosing an index for their passive investment. This is an area where asset managers can add value to institutional investors. For example, we often work closely with clients and index providers on opportunities to co-develop indexes and strategies. At the end of the day, the goal is to meet client needs around performance, transparency, tracking error, and overall cost.

Christopher Huemmer: As Jake alluded to, the biggest challenges for institutional investors confronted with more choices are not just about the methodologies, but rather understanding from where returns and risk come and where to get those exposures. I think the key thing investors need to be aware of is to not take labeling and naming conventions at face value, but rather to understand the nuances. One example that comes to mind is listed infrastructure. This asset class has evolved thematically over the last 15 years from what was essentially just “glorified” utilities to the inclusion of all types of infrastructure. The key development is in how index providers have been able to classify the infrastructure companies. Fifteen to twenty years ago, active managers had an informational edge that enabled them to access pockets of the infrastructure complex that passive indexes were not capturing. Today you’re seeing index providers come up with more nuanced, sophisticated ways of developing those classification systems to deliver the exposure that investors are looking for.

Institutional Investor: What has driven the growth in adoption of passive indexing more recently?

Austin Guy: When looking at flows within market segments, passive market share has grown predominately within U.S. large caps, almost directly at the expense of active U.S. large caps. We still see active management in what are generally regarded as less efficient market segments such as small caps, emerging markets, and other more thematic segments like listed infrastructure, as Chris mentioned, although that continues to change. We believe there is a fit for both styles within a portfolio. Another more forward-looking perspective is that given heightened market volatility as one factor, meeting return targets continues to require additional asset classes beyond the traditional 60/40 portfolio, which has increased complexity and often expenses as well, in the form of higher fees to portfolios. One way to look at indexing is to use passive index funds as a tool within a public equity or fixed income portfolio to drive down your costs and optimize your liquidity. As many have increased allocations to less-liquid segments like alternatives, using passive indexes to lower tracking error and expenses is a way to leverage passive funds, and supports the use case for indexing further.

Institutional Investor: How do performance differences expose the nuances in index design?

Jake Weaver: Building on the theme Austin was on, the increasing number of decisions being made by investors doesn’t stop at the strategic or even tactical allocation level, but extends to selecting a benchmark for a passive index fund. Investors should understand that even indexes with similar names or asset class targets can have significant differences in methodology and exposures. If we go back to 2020 at the height of the COVID pandemic, the two most widely used U.S. large-cap indexes, the Russell 1000 and the S&P 500, saw meaningful return differences with the Russell 1000 up about 21% and the S&P 500 up about 18.4%. A handful of technology stocks that were included in the Russell 1000 — but not in the S&P 500 — drove these differences. Another example occurred in the U.S. small cap space in 2021. The S&P 600 Small Cap index returned 26.7% and the Russell 2000 Small Cap index returned only 14.8% — a huge difference and a partial reversal from the prior year. These differences are attributed to differences in methodologies that are impacting which stocks and sectors have higher weights in the different indexes.

Christopher Huemmer: Another simple example is how different index providers define the term “World.” For some providers, that’s going to mean only developed markets, while for others it would include emerging markets as well. So, you’re talking about different return and risk profiles. Also, the naming conventions and nuanced differences between the definitions of value and growth or large cap and small cap come into play. For example, Russell and S&P define value and growth using different metrics, which can lead to meaningfully different outcomes. In 2023, the Russell 1000 Growth index outperformed S&P 500 Growth by 12.6%, which is a massive amount given likely expectations. We think it’s important for investors to understand what is causing those differences.

Natural resources is another example where methodology differences are crucial for investors to understand. Natural resources indexes typically seek exposure to energy, metals and agriculture, but different indexes use different methodologies. One index might deliver an exposure to agriculture where the majority of that weight, maybe 60%, is going to be downstream operations not conventionally thought of as agriculture. For example, it may include cardboard and packaging companies that you wouldn’t find in a traditional commodities index. So, understanding the nuances and differences behind the indexes’ methodologies is really key. I think Northern Trust Asset Management does a really good job of identifying and communicating these differences to help our clients understand the implications and navigate through them to select the indexes they use in their portfolios.

Institutional Investor: Index concentration has increased significantly over the last decade. Is this a positive or negative for index investors and what else has contributed to increasing concentration risk?

Austin Guy: While a benefit of passive indexing is effectively letting winners run and reducing exposure to underperforming companies, concentration risk is often an outcome of market capitalization weighting. A lot of the concentration risk recently has come from the performance of the Magnificent 7 (a group of high-performing tech stocks including Facebook, Apple, Google, and etc.), but it’s not really a new phenomenon despite it receiving a lot of media attention. We've seen other periods of market concentration within U.S. stocks, and currently outside the U.S. as well. Using a few MSCI country indexes for comparison, the ten largest companies in the MSCI USA index make up just shy of 30% of the index, but if you look at the MSCI Japan Index, the ten largest companies make up a similar 27%, or even more concentrated is the MSCI Germany Index where the 10 largest stocks make up almost 60%. Part of the reason why the U.S. is featured heavily within this concentration conversation is because it makes up 60-70% of global and developed international indexes, and by extension, passive equity portfolios.

Institutional Investor: We've seen a lot of interest in customization, be it for index funds or model portfolios. Everyone's interested in customization, so what does this mean for active management?

Austin Guy: It may mean that active management will need to differentiate more by taking more active risk or creating more niche and bespoke strategies, because the cost-effective index solutions that can be customized to take on incrementally more active risk are not only going to become popular, but may be hard to outperform over long time periods when adjusting for fees and risk-adjusted returns. Index funds are now encroaching upon the opportunity set that was once predominately accessible only through active managers. The flip side, of course, is that passively managed funds will continue to be rules-based by design and therefore investors are cosigning on the methodology, which as we discussed previously, is not necessarily a straightforward assessment. Therefore, investors still need to assess index funds as they would active managers.

Christopher Huemmer: From an asset allocation standpoint, I’m seeing more of the active decisions around risk and return exposures being achieved at the portfolio level, and then implemented using passive indexing to get the desired exposures.

From a product design standpoint, we are building strategies that reflect this approach. We’re collaborative with our index providers. When we’re designing new tools for our clients, we come to the table with insights and expertise that aids us in identifying a suitable index partner that pairs well with their skill set to deliver on their objectives. We seek to collaborate with the right partner to leverage their distinctive abilities to design more effective indexes that reflect our clients’ needs.

IMPORTANT INFORMATION

For Use with Institutional Investors and Financial Professionals Only. Not For Retail Use.

Northern Trust Asset Management (NTAM) is composed of Northern Trust Investments, Inc., Northern Trust Global Investments Limited, Northern Trust Fund Managers (Ireland) Limited, Northern Trust Global Investments Japan, K.K, NT Global Advisors, Inc., 50 South Capital Advisors, LLC, Northern Trust Asset Management Australia Pty Ltd, and investment personnel of The Northern Trust Company of Hong Kong Limited and The Northern Trust Company.

Issued in the United Kingdom by Northern Trust Global Investments Limited regulated by the Financial Conduct Authority (Licence Number 191916), issued in the European Economic Area (“EEA”) by Northern Trust Fund Managers (Ireland) Limited regulated by the Central Bank of Ireland (Licence Number C21810) , issued in Australia by Northern Trust Asset Management (Australia) Limited (ACN 648 476 019) which holds an Australian Financial Services Licence (License Number: 529895) and is regulated by the Australian Securities and Investments Commission (ASIC), and issued in Hong Kong by The Northern Trust Company of Hong Kong Limited which is regulated by the Hong Kong Securities and Futures Commission.

This information is directed to institutional, professional and wholesale current or prospective clients or investors only and should not be relied upon by retail clients or investors. The information is not intended for distribution or use by any person in any jurisdiction where such distribution would be contrary to local law or regulation. NTAM may have positions in and may effect transactions in the markets, contracts and related investments different than described in this information. This information is obtained from sources believed to be reliable, its accuracy and completeness are not guaranteed, and is subject to change. Information does not constitute a recommendation of any investment strategy, is not intended as investment advice and does not take into account all the circumstances of each investor.

This report is provided for informational purposes only and is not intended to be, and should not be construed as, an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Recipients should not rely upon this information as a substitute for obtaining specific legal or tax advice from their own professional legal or tax advisors. References to specific securities and their issuers are for illustrative purposes only and are not intended and should not be interpreted as recommendations to purchase or sell such securities. Indices and trademarks are the property of their respective owners. Information is subject to change based on market or other conditions.

Past performance is not a guarantee of future results. Performance returns and the principal value of an investment will fluctuate. Index performance returns do not reflect any management fees, transaction costs or expenses. It is not possible to invest directly in any index.

Forward-looking statements and assumptions are NTAM’s current estimates or expectations of future events or future results based upon proprietary research and should not be construed as an estimate or promise of results that a portfolio may achieve. Actual results could differ materially from the results indicated by this information.

© 2024 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A.