In the aftermath of the Global Financial Crisis (GFC), Collateralized Loan Obligations (CLOs) emerged as a contentious topic and were viewed through a cautious lens. However, as financial markets have evolved, the asset class has been gaining wider prominence as one of the most underutilized areas of opportunity and diversification in the alternatives space. Particularly in a market where interest rates remain high, CLOs have been offering investors compelling coupons, lower volatility, and comparable liquidity to Investment Grade (IG) Corporate bonds. In a bid to protect their portfolios against interest rate erosion, major banks like J.P. Morgan, Bank of America, and Citigroup have been paying attention, buying up top-rated CLOs that carry SOFR-based floating-rate coupons, helping propel credit gains. The question then remains, if CLOs are now a viable complement to traditional fixed income investments, garnering mainstream interest and consistently outperforming lower rated alternatives - then why aren’t more investors taking notice?

To shed light on these opportunities that investors might be overlooking, Institutional Investor spoke with James Guido, Vice President and Wayne Hosang, Managing Director and Portfolio Manager, both with Los Angeles-based global credit investment manager Crescent Capital. Crescent has over 30 years of experience investing in public and private credit markets, as well as extensive experience managing structured products.

Institutional Investor: As interest rates remain elevated and their course uncertain, volatility is top of mind for fixed income investors. How have CLOs performed relative to other traditional fixed income asset classes amidst market volatility, and what is it that makes them stand out amongst peers?

Wayne Hosang: In short, CLO bonds performed exactly as they were supposed to, with low volatility relative to other asset classes in both down-markets and up-markets. For instance, in 2022 CLO IG bonds returned between -2.77% (BBB) and +1.05% (AAA) versus -15.42% for IG Corporate bonds; while in 2023, they returned +8.68% (AAA) to +17.66% (BBB) versus +8.35% (IG Corp).1 The floating-rate feature of CLO bonds insulated them against volatility experienced by their fixed-rate peers. In line with the theme of this article, I think that CLO debt tranches continue to be generally misunderstood allowing them to maintain strong relative attractiveness versus other fixed income products.

James Guido: That’s right - CLOs have low interest rate duration and pay a floating-rate coupon based on 3-Month SOFR. As rates rose in 2022-2023, so did CLO coupons - and this offset some of the short-term price volatility experienced, which was already less pronounced than what we saw in other fixed income markets during the same time. Bottom line, CLOs are an excellent way to diversify away from fixed-rate, single-name credit risk, into an asset class that consistently delivers higher yields and lower defaults versus similar and even lower rated Corporate Bonds and Bank Loans. The CLO market is essentially paying you to trade up in rating quality and get diversified.

Institutional Investor: Why are traditional fixed income investors not as drawn to CLOs, and why should they reconsider?

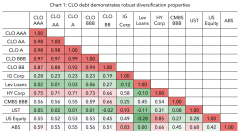

Wayne Hosang: I think because CLO debt tranches are generally viewed by traditional bond investors as an alternative asset, and therefore they are often overlooked. The more likely reason is that CLOs get lumped in together with other structured products that were highlighted as contributing to the great financial crisis in 2008. We now have enough data to demonstrate that CLO structures are resilient, and the message to investors is CLOs fit well in any diversified fixed income portfolio. They provide excellent relative value and display relatively low correlation to fixed-rate products, especially during periods of interest rate uncertainty. It’s a tool available to investors in this highly competitive market that can enhance the performance of their portfolios. Finally, another great aspect of CLOs is that they can be viewed as a diversified play on bank loans without taking on single-name credit risk.

Institutional Investor: CLOs were once thought to be illiquid. What has changed, and what do investors need to know about this market, which just eclipsed $1 trillion in outstanding size?

James Guido: No matter how you look at it, CLO market liquidity has improved leaps and bounds since the market reopened post-GFC 10+ years ago - especially in the past 3-5 years around COVID. The market has approximately doubled in size since 2017, from about $500 billion outstanding to just over $1 trillion today2 —and with that comes more liquidity naturally. The CLO market is a mature, proven asset class at this point, and new investors should not shy away from participating due to misconceived complexities. We are witnessing growing investor participation that spans the globe, deeper bank balance sheet and syndication capabilities, an expanding universe of issuers, a growing list of investment vehicles to access the market, and of course, very active primary and secondary markets which remained open during recent bouts of market turbulence which saw other fixed income markets freeze up.

Wayne Hosang: Up until 4 or 5 years ago, one could argue that CLO tranches were relatively illiquid versus IG and HY corporate bonds. Nowadays, I don’t think you can make that statement. With the market crossing the trillion-dollar mark, we have been able to readily access the market, particularly in the IG tranches. For perspective, we do not think this market is materially less liquid than the underlying BSL or HY markets, both of which are about $1.5 trillion in size.

James Guido: Due to the securitized nature of the product, CLOs are not actively quoted like bonds or loans are, but this should not be mistaken for lack of liquidity. Most lower-rated CLO BB tranches – a relatively thinner market than say CLO AAA – could often see upwards of 10 unique bids from institutional clients and banks when put up for sale on a bid list. It is also telling when you see large institutions (both foreign & domestic) tap the CLO market for liquidity, selling a few hundred million CLO AAA / AA’s with one day notice for next day settlement, for example.

Institutional Investor: There has been much discussion around potential default rates on loans this year given market volatility and interest rate uncertainty. How do CLOs mitigate that risk, if at all?

James Guido: Widely telegraphed projections on loan defaults in recent years have been wrong for the most part (thus far). Although, peak interest rates leave junk-rated HY Bond / Leveraged Loan borrowers under pressure, which could result in more idiosyncratic defaults. With that being said – CLO investors should ultimately feel these defaults less than the HY Bond / Loan investors who own these credits directly. This is thanks to the resilient CLO structure; each CLO, typically $500mm in size, is backed by a pool of 200+ broadly syndicated, senior secured bank loans. The pools are highly diversified and have limits on how much of a certain obligor, industry and rating can be owned – amongst many other things. The underlying loans are liquid – most being actively quoted and traded on a daily basis – which is helpful in determining the ongoing quality of the loans in the pool. For instance, loans will trade up or down in price for a reason, as the market incorporates ever-changing fundamentals into the trading price of the loan. CLO investors have very good look-through into the quality of loans in the pool that back their CLO tranche investment. Last but certainly not least, these pools are actively managed by a third-party collateral manager. These managers are typically seasoned loan investors who oversee many other CLOs and the billions of loans that back them. Bottom line, thanks to the actively managed, highly diversified, liquid nature of the pool of loans that backs our CLOs – the risk can be mitigated, and losses (par burn) in the underlying collateral pool could be offset with gains (par build). CLO investments give you exposure to a pool of 200+ loans – not a single loan.

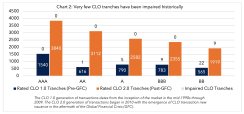

Wayne Hosang: As James alluded to, CLOs are conservatively structured, and default and recovery rates on the underlying assets would have to be severe before CLO debt tranches become impaired. In fact, no CLO debt tranche rated BBB or higher issued in the post-GFC era has ever been impaired.

Institutional Investor: What distinguishes the CLO investment opportunity from other products, and what is something that investors might not be aware of?

James Guido: The CLO asset class has something for everyone, and the ability to rotate throughout different rating classes within the same capital structure to solve for different investment needs stands out. Whether it is Ultra-High Quality, Cash Management needs (CLO AAA), or High Coupon, Below-IG needs (CLO BB / Equity), the CLO market offers compelling, scalable opportunities across the rating spectrum that should be considered. The CLO opportunity set allows investors tremendous flexibility when it comes to fine-tuning a portfolio for ever-changing risk, return and liquidity needs. Investors can pick their spots within the capital structure and take a view on the market, credit, spreads or relative value by mixing and matching their rating exposure.

Wayne Hosang: I totally agree with James. That flexibility cannot be overstated, especially during times of uncertainty. The ability to choose a risk profile to express a view on the market without having to increase or decrease exposure to the underlying assets is often overlooked by investors.

Institutional Investor: Where do the opportunities lie in the asset class?

Wayne Hosang: With a strong macroeconomic backdrop and what appears to be a smooth landing in the coming quarters, the opportunity in CLOs is access to strong performance without having to focus on every utterance from the Fed. Even in a scenario of a few rate cuts in 2024, the income generated will still be historically high, and will exceed similarly rated corporate bonds, and with lower volatility.

James Guido: Short-dated IG CLO Debt in the secondary market is a great way to get dollars in the ground at peak rates quickly. At the same time, with CLO new issuance off to a record start in 2024 – this is a good, scalable opportunity to buy new issue mezzanine BBB / BB tranches constructed with fresh collateral pools and attractive spreads.

Institutional Investor: Would you say that the ability to trade in and out of the different levels of debt is something that differentiates CLOs from other debt instruments?

Wayne Hosang: Yes, for sure when compared to the corporate credit. With CLOs you have the ability to migrate up and down the debt stack and choose to have exposure from the highest credit rating (i.e., AAA) to below-investment grade (i.e., BB). In contrast, in the corporate bond universe it is very difficult to find companies you like where you have the ability to invest across a range of ratings classes while remaining neutral on duration.

James Guido: The ability to trade in and out of different rating tiers swiftly is unique – as is the ability of CLOs to trade in and out of different loans in the collateral pool. The actively managed nature of the collateral pools that back these tranches is a main driver to the CLO markets success.

1 Source: JPM CLOIE Monitor.

2 Source: JP Morgan CLO Research,