On 19 November, it emerged that Carlos Ghosn – chairman and CEO of the Renault-Nissan-Mitsubishi consortium – had been arrested under suspicion of financial misconduct relating to the under-reporting of his compensation and his personal use of company money. Long perceived as a successful and charismatic business leader – a man instrumental in the turnaround of Renault and Nissan in the 1990s and early 2000s – it came as a huge shock to the business community. “Corporate governance and the dangers of leaving too much power unchecked in too few hands are once again in the spotlight,” says François Millet, Lyxor’s Head of ETF and Index Product Development.

Since the news of his arrest, Ghosn has been ousted as both Chairman of Nissan and Chairman of Mitsubishi Motors. For the moment, he remains Chairman and CEO of Renault pending more clarity. Ghosn denies the charges and nothing has been proven against him as yet. Regardless, shares in Nissan, Renault SA and Mitsubishi Motors have fallen by 3.4%, 4.5% and 3.4% respectively following the news, and have yet to recover their losses.1

These events were unexpected, but not entirely unique given they echo the excesses of the Enron era – so what can you do to try to get a more rigorous grip on governance in your portfolio?

Putting the “G” in ESG

With news of the devastating impact of climate change on our environment filling media outlets on a daily basis, the “E” in ESG tends to be the most closely scrutinised. Yet here’s a great example of how important it is for investors to pay attention to governance as well.

“If you hold a fund with hundreds – if not thousands – of stocks, you’d be forgiven for not having the time or expertise to carry out a thorough due diligence of each and every one of them based on their ESG metrics,” says Millet. “The good news is that there are experts who have that kind of know-how.” When choosing the strategy underlying its broad ESG ETFs, Lyxor chose to partner with index provider and ESG research specialist, MSCI.

MSCI has more than 40 years of experience in collecting, cleaning and standardising data on ESG policies. In building their best-in-class ESG Leaders benchmark series, MSCI’s goal is to include companies with the highest ESG rating in each sector, with a 50% sector representation vs. the broad parent index.

At this level already, neither Nissan nor Mitsubishi Motors make the cut for the ESG Leaders indices. They both have an MSCI ESG Rating of CCC – the worst possible ranking. In Nissan’s case, this mainly has to do with weak governance practices, safety, and emission falsifications. Mitsubishi Motors’ score relates to similar issues around poor business ethics, fraud, and a fuel test manipulation controversy.2

Why it’s worth going the extra mile

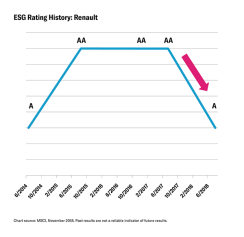

Here’s where things get interesting. Renault, according to MSCI, scores well in areas like safety and clean tech. So, while not securing the top AAA rating, it still fares relatively well with an A – which is enough for it to feature in European MSCI ESG Leaders indices.2

It is possible to take it further however, and adopt MSCI’s ESG Trend Leaders series. Not only do these benchmarks require a high ESG score, they also take that score’s trend into account. “If a company has improved its ESG score over a one-year period, it is more likely to be included in one of these indices but a downward trend reduces that likelihood,” says Millet.

Renault, as noted, has a decent ESG score and was rated AA at one stage, but because of “concerns over potential conflict of interests in the role held by the Chairman, Mr. Carlos Ghosn,” and additional concerns over governance practices linked to its complex ownership structure, MSCI downgraded its rating before news of the scandal actually broke.2

The key single risk factor identified by MSCI’s ESG research was corporate governance. The downward trend reduced Renault’s overall score, meaning it was not present in the MSCI ESG Trend Leaders benchmarks tracked by Lyxor’s World and EMU ESG ETFs. “That’s not to say using Trend is a perfect way to avoid issues of poor governance – and there is always the risk that something could slip through the net,” says Millet. “It could, however, give you a head start.”

Why choose Lyxor for ESG?

The MSCI ESG Trend Leaders benchmarks are designed to identify those companies with a robust ESG profile today, as well as the capacity to improve it. This extra step can help detect and eliminate controversial companies by considering their ESG trend. Those companies committed to improving the world around them are hence more likely to be included. MSCI data shows that rewarding ESG momentum can potentially improve company performance more than excluding or just tilting weightings towards companies with a high ESG rating alone.

Lyxor’s MSCI ESG Trend Leaders range is:

- Far reaching: World, EMU, USA and Emerging Markets exposures available1

- Innovative: one step further by taking into account ESG momentum as well as ESG rating

- Unique: the first and only ETFs in Europe tracking these benchmarks1

Find out how you can stay ahead of the curve with our MSCI ESG Trend Leaders ETFs

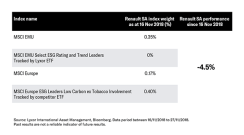

1Source: Lyxor International Asset Management, Bloomberg. Share performance in local currency terms. Data period from 16/11/2018 to 27/11/2018. Past performance is not a reliable indicator of future results.

2Source: Lyxor International Asset Management, MSCI, as at 26 November 2018. Past performance is not a reliable indicator of future results.

This article is for informative purposes only, and should not be taken as investment advice. Lyxor ETF does not in any way endorse or promote the companies mentioned in this article. Capital at risk. Please read our Risk Warning below

Risk Warning

This document is for the exclusive use of investors acting on their own account and categorised either as “Eligible Counterparties” or “Professional Clients” within the meaning of Markets in Financial Instruments Directive 2014/65/EU. These products comply with the UCITS Directive (2009/65/EC). Société Générale and Lyxor International Asset Management (LIAM) recommend that investors read carefully the “investment risks” section of the product’s documentation (prospectus and KIID). The prospectus and KIID are available free of charge on www.lyxoretf.com, and upon request to client-services-etf@lyxor.com.

The products mentioned are the object of market-making contracts, the purpose of which is to ensure the liquidity of the products on the London Stock Exchange, assuming normal market conditions and normally functioning computer systems. Units of a specific UCITS ETF managed by an asset manager and purchased on the secondary market cannot usually be sold directly back to the asset manager itself. Investors must buy and sell units on a secondary market with the assistance of an intermediary (e.g. a stockbroker) and may incur fees for doing so. In addition, investors may pay more than the current net asset value when buying units and may receive less than the current net asset value when selling them. Updated composition of the product’s investment portfolio is available on www.lyxoretf.com. In addition, the indicative net asset value is published on the Reuters and Bloomberg pages of the product, and might also be mentioned on the websites of the stock exchanges where the product is listed.

Prior to investing in the product, investors should seek independent financial, tax, accounting and legal advice. It is each investor’s responsibility to ascertain that it is authorised to subscribe, or invest into this product. This document is of a commercial nature and not of a regulatory nature. This material is of a commercial nature and not a regulatory nature. This document does not constitute an offer, or an invitation to make an offer, from Société Générale, Lyxor Asset Management (together with its affiliates, Lyxor AM) or any of their respective subsidiaries to purchase or sell the product referred to herein.

Lyxor International Asset Management (LIAM), société par actions simplifiée having its registered office at Tours Société Générale, 17 cours Valmy, 92800 Puteaux (France), 418 862 215 RCS Nanterre, is authorized and regulated by the Autorité des Marchés Financiers (AMF) under the UCITS Directive (2009/65/EU) and the AIFM Directive (2011/31/EU). LIAM is represented in the UK by Lyxor Asset Management UK LLP, which is authorized and regulated by the Financial Conduct Authority in the UK under Registration Number 435658. Société Générale is a French credit institution (bank) authorised by the Autorité de contrôle prudentiel et de résolution (the French Prudential Control Authority).

Research disclaimer

Lyxor International Asset Management (“LIAM”) or its employees may have or maintain business relationships with companies covered in its research reports. As a result, investors should be aware that LIAM and its employees may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. Please see appendix at the end of this report for the analyst(s) certification(s), important disclosures and disclaimers. Alternatively, visit our global research disclosure website www.lyxoretf.com/compliance.

Conflicts of interest

This research contains the views, opinions and recommendations of Lyxor International Asset Management (“LIAM”) Cross Asset and ETF research analysts and/or strategists. To the extent that this research contains trade ideas based on macro views of economic market conditions or relative value, it may differ from the fundamental Cross Asset and ETF Research opinions and recommendations contained in Cross Asset and ETF Research sector or company research reports and from the views and opinions of other departments of LIAM and its affiliates. Lyxor Cross Asset and ETF research analysts and/or strategists routinely consult with LIAM sales and portfolio management personnel regarding market information including, but not limited to, pricing, spread levels and trading activity of ETFs tracking equity, fixed income and commodity indices. Trading desks may trade, or have traded, as principal on the basis of the research analyst(s) views and reports. Lyxor has mandatory research policies and procedures that are reasonably designed to (i) ensure that purported facts in research reports are based on reliable information and (ii) to prevent improper selective or tiered dissemination of research reports. In addition, research analysts receive compensation based, in part, on the quality and accuracy of their analysis, client feedback, competitive factors and LIAM’s total revenues including revenues from management fees and investment advisory fees and distribution fees.