New data analysis reveals that private real assets offer compelling potential for institutional investors to enhance risk-adjusted returns as they anticipate more frequent volatility spikes and uncertainty regarding the pace of economic recovery, inflation, and interest rates.

According to the analysis, private investments in relatively illiquid categories of real assets – farmland, timberland, and commercial real estate – have exhibited low or negative correlations to stocks and bonds, diversifying portfolio risk. In the analysis, adding private exposure to any one of those categories increased portfolio returns and reduced risk, resulting in higher Sharpe Ratios.

The analysis was conducted by Gwen Busby, Ph.D., Head of Economic Research and Strategic Development, GreenWood Resources; Skye Macpherson, CAIA, Head of Portfolio Management, Westchester Group Investment Manager; and Abigail Dean, Global Head of Strategic Insights, Nuveen Real Estate.

Four key observations

In addition to the lack of correlation with traditional assets, the authors of the analysis chose farmland, timberland, and commercial real estate, because they are relatively illiquid, infrequently traded, or insulated from commodities speculation, such as options trading. In addition, farmland, timberland, and commercial real estate have at least 25 years of index performance data as a reasonable foundation for analysis.The analysis used traditional mean-variance portfolio optimization (MVO), based on historical performance, standard deviation, and correlations of returns by asset class. In conducting the analysis, four key observations emerged.

Observation #1: Real assets improved the risk-adjusted returns of a portfolio of traditional stocks and bonds.

Institutional investors want to know how private real assets impact the risk and return attributes of a portfolio of stocks and bonds. In the data below (see Fig. 1), efficient frontier charts show the impact of adding farmland, timberland, and real estate individually to a stock/bond portfolio. The table also shows the impact of combining all three categories. In this example, real assets were constrained to 15%, divided evenly at 5% in each.

Results of analysis

- Each category of real assets increased returns, with similar or lower levels of risk, resulting in higher Sharpe Ratios.

- Farmland had the greatest impact on risk-adjusted returns and received the largest allocation in an unconstrained portfolio at 42%. Real estate at 29% had the second biggest impact on returns, followed by timberland at 21%.

- Diversifying a stock/bond portfolio with a 5% allocation to each of the three real assets increased annual returns by 28 basis points and reduced risk by 67 basis points, producing a higher Sharpe Ratio.

Overall, results support the case for diversifying traditional portfolios with multiple categories of real assets even when constrained within realistic limits. The constraints reflect supply limitations, the relative illiquidity of real assets, their relatively high transaction costs, and the limited history contained in the analysis.

Observation#2: Private real assets provided higher returns with lower volatility than publicly traded commodities and real estate stocks.

Private real assets were compared with publicly traded commodity stocks and commercial REITs to assess diversification benefits against the illiquidity of private assets. Since many institutional investors already have exposure to REITs and commodities, such as metals or oil and gas, the impact of combining private real assets with public stocks was also compared. The analysis used fixed allocations and constrained alternatives to 15% of the portfolio, consistent with realistic limits.The data below compares three portfolios consisting of a fixed 85% in stocks and bonds in a 60/40 ratio, and 15% in alternative assets. Portfolio 1 adds three categories of private real assets, divided evenly at 5% each. Portfolio 2 adds three categories of publicly traded commodities and REITs, divided evenly at 5% each. Portfolio 3 combines private and public assets, split evenly at 2.5% each.

Results of analysis

- Private real assets increased portfolio returns and reduced volatility, resulting in a higher Sharpe Ratio, versus publicly traded commodity stocks and REITs. This can be seen by comparing the performance of Portfolio 1 and Portfolio 2 in Fig. 2 (above).

- Private real assets helped to diversify the volatility risk of publicly traded commodities and REITs. This can be seen by comparing the performance of Portfolio 2 and Portfolio 3 in the above charts. The combination of private and public assets in Portfolio 3 increased returns by 22 basis points and reduced volatility by 73 basis points, resulting in a higher Sharpe Ratio, compared to Portfolio 2.

Observation #3: Farmland dominated a portfolio consisting only of private real assets.

The next analysis shows how different asset categories work together in a portfolio consisting only of private real assets by examining how the structure can change based on different investment objectives. An efficient frontier using farmland, timberland, and real estate allowed comparison of three portfolios producing the highest efficiency, lowest risk, and highest return (see Fig. 3).

Results of analysis

- The most risk-efficient portfolio was dominated by farmland at 64%, but also included 19% timberland and 17% real estate, benefitting from low correlations among the categories.

- The lowest-risk portfolio reduced farmland exposure to 39% and increased timberland and real estate to 25% and 36%, respectively, reflecting relatively low or negative correlations between categories.

- The highest-return portfolio consisted of 100% farmland, reflecting higher returns and lower volatility compared to timberland and real estate.

- Overall, the most efficient real asset portfolio generated much higher risk-adjusted returns than the most efficient combination of traditional stocks and bonds. The real asset portfolio produced an additional 377 basis points of return and only increased standard deviation by 163 basis points.

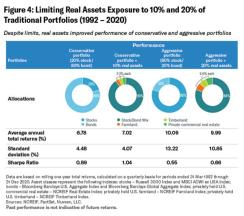

Observation #4: Constraining real assets within practical limits still improved performance.

How much real assets exposure is reasonable for institutional investors? Real assets are expected to continue their recent steady growth, with current portfolio allocations generally estimated at 5% to 10%, and endowments ranging up to about 15%. Overall, real assets represent more than $10 trillion out of $27 trillion of global institutional assets under management in 2019, or nearly a third. Additionally, institutions are increasing their exposure to alternatives in efforts to increase current income and risk-adjusted returns, dampen volatility, and meet specific needs, such as inflation protection.Mean-variance optimization outputs may suggest extreme allocations to individual asset classes based on returns for the time period used as inputs. For most institutions, allocations exceeding 25% to individual real assets categories would be unrealistic. Most portfolios would lack sufficient liquidity to meet near-term spending obligations, and investors would have difficulty accessing enough farmland and timberland. Moreover, questions about the limitations and relatively short history of index data would argue against such large holdings in real assets.

There is no single optimal allocation to real assets, which will differ based on the investor’s specific risk profile. The next analysis considers two model portfolios representing a conservative allocation of 20% stock and 80% bonds and an aggressive allocation of 80% stock and 20% bonds. The combined real asset allocation is limited to 10% (3.3% per category) in the conservative portfolio and 20% (6.6% per category) in the aggressive portfolio.

Results of analysis

- Despite the allocation limits, real assets reduced volatility compared to only stock-bond portfolios – resulting in higher risk-adjusted returns (see Fig. 4, above).

- Overall, results show that, based on historical performance, investors could improve portfolio risk-adjusted returns with allocations that were fractions of the unconstrained allocations, but realistic for institutional investors.

OPINION PIECE: FOR INSTITUTIONAL USE ONLY. NOT FOR PUBLIC DISTRIBUTION.

The statements contained herein are based upon the opinions of Nuveen and its affiliates, and the data available at the time of publication of this report, and there is no assurance that any predicted results will actually occur. Information and opinions discussed in this commentary may be superseded and we do not undertake to update such information. This material is provided for informational or educational purposes only and does not constitute a solicitation in any jurisdiction. Moreover, it neither constitutes an offer to enter into an investment agreement with the recipient of this document nor an invitation to respond to it by making an offer to enter into an investment agreement. This material may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections, forecasts, estimates of yields or returns, and proposed or expected portfolio composition. Moreover, certain historical performance information of other investment vehicles or composite accounts managed by Nuveen has been included in this material and such performance information is presented by way of example only. No representation is made that the performance presented will be achieved by any Nuveen funds, or that every assumption made in achieving, calculating or presenting either the forward-looking information or the historical performance information herein has been considered or stated in preparing this material. Any changes to assumptions that may have been made in preparing this material could have a material impact on the investment returns that are presented herein by way of example. This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The information and opinions contained in this material are derived from proprietary and non-proprietary sources deemed by Nuveen to be reliable, and not necessarily all-inclusive and are not guaranteed as to accuracy. There is no guarantee that any forecasts made will come to pass. Company name is only for explanatory purposes and does not constitute as investment advice and is subject to change. Any investments named within this material may not necessarily be held in any funds/accounts managed by Nuveen. Reliance upon information in this material is at the sole discretion of the reader. They do not necessarily reflect the views of any company in the Nuveen Group or any part thereof and no assurances are made as to their accuracy. Past performance is not a guide to future performance. Investment involves risk, including loss of principal. The value of investments and the income from them can fall as well as rise and is not guaranteed. Changes in the rates of exchange between currencies may cause the value of investments to fluctuate.

This material is presented for informational purposes only and may change in response to changing economic and market conditions. This material is not intended to be a recommendation or investment advice, does not constitute a solicitation to buy or sell securities, and is not provided in a fiduciary capacity. The information provided does not take into account the specific objectives or circumstances of any particular investor, or suggest any specific course of action. Financial professionals should independently evaluate the risks associated with products or services and exercise independent judgment with respect to their clients. Certain products and services may not be available to all entities or persons. Past performance is not indicative of future results.

Economic and market forecasts are subject to uncertainty and may change based on varying market conditions, political and economic developments. As an asset class, real assets are less developed, more illiquid, and less transparent compared to traditional asset classes. Investments will be subject to risks generally associated with the ownership of real estate-related assets and foreign investing, including changes in economic conditions, currency values, environmental risks, the cost of and ability to obtain insurance, and risks related to leasing of properties.

Real Asset investments may be subject to environmental and political risks and currency volatility.

Nuveen provides investment advisory solutions through its investment affiliates.

© 2021 Nuveen, LLC. All rights reserved.